GOLD: Gold Rallies On Fed Easing Expectations But December Not Yet A Given

Gold continued to rally into the reopening of the US government on expectations that the release of the delayed data will show a weaker economy allowing the Fed to cut rates again on 10 December. This may be a bit optimistic as some Fed speakers on Wednesday suggested that with inflation above target there is a high bar to further easing for them. Also market pricing for December has come down with around 15bp priced in.

- The US House of Reps vote on the bill to reopen the government is to be held around 1900 EST/0000 GMT. Our US analysts believe that the post-shutdown data schedule should be published next week. See their FAQ here. The White House also indicated that October CPI and jobs data may not be published.

- Gold rose 1.7% to $4195.39 on Wednesday, close to the intraday high of $4211.79 and above initial resistance at $4161.4, 22 October high opening the bull trigger at $4381.5. It has started Thursday around $4199.5. Bullion is now 4.8% higher this month signalling that the correction is done. The US dollar was flat yesterday but the 2-year yield slightly lower.

- Silver rallied 4% to $53.260 to be 9.4% higher in November and is currently around $53.30. It reached $53.671 yesterday, above initial resistance at $52.374 and opening the bull trigger at $54.480. The bull cycle remains intact.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: UK BRC SEP BY VALUE SHOP SALES LFL +2.0% Y/Y, TOTAL +2.3% Y/Y

- MNI: UK BRC SEP BY VALUE SHOP SALES LFL +2.0% Y/Y, TOTAL +2.3% Y/Y

UK DATA: Retail Sales Slow Amid Budget Caution, Still Boosted By Food Inflation

BRC Retail Sales data for September posted a 2.3% Y/Y increase, a slowdown from the 3.1% of August, and marginally above the 12-month average of 2.1%. However, it is important to note that the monitor is a value measure and a large proportion of the increase is likely due to inflation.

- Food sales (the largest contributor) slowed slightly versus August, growing 4.3% Y/Y (vs 4.7% Aug), though the press release notes that "growth in food sales was largely inflationary rather than volume growth".

- Non-food sales weakened, increasing 0.7% Y/Y (vs 1.8% Aug), below the 12-month average of 0.9%. The figure was propped up by strong electrical sales, from the release of the new iPhone and Apple Watch, and strong furniture sales.

- Planning spending around high inflation and a "potentially taxing Budget" ahead of the Christmas period is highlighted as a notable downward driver by the BRC.

- Note that ONS's retail sales volume index sees the September data released on 24 October, following a 0.5% M/M rise in August. The in the BRC report covers the same 5 weeks as the ONS report (from 31 August - 5 October 2025).

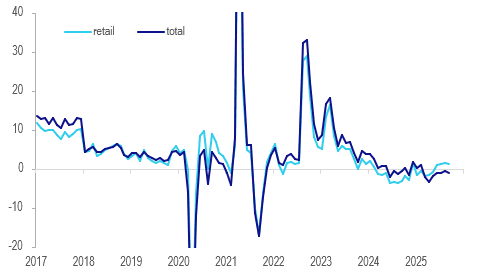

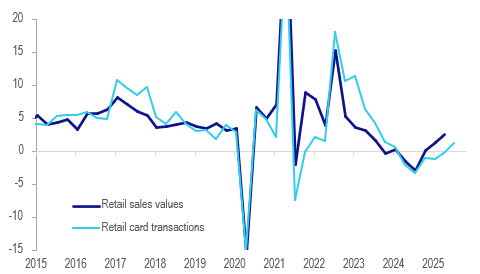

NEW ZEALAND: Q3 Retail Spend Up On Quarter But Still Soft Consistent With Easing

September retail card transactions fell 0.5% m/m after rising 0.6%, the first negative after three consecutive increases. Annual growth slowed to an anaemic 1.2% y/y signalling that while consumption is off its lows the recovery remains weak making additional RBNZ rate cuts more likely. The extent of further easing including in early 2026 remains highly data dependent though.

NZ retail spending y/y%

Source: MNI - Market News/LSEG

- Despite the soft end to Q3, the quarter saw a 0.6% q/q increase in nominal retail spending driven by consumables (+1.0%), hospitality (+1.4%) and motor vehicles (+2.7%). Q3 retail sales volumes are released 27 November. They rose 0.5% q/q & 2.3% y/y in Q2.

- Total expenditure was down 0.4% m/m in September after rising 0.4% to still be down 1% y/y. The total was up 0.7% q/q in Q3.

- Core retail spending fell 0.4% m/m in September but rose 0.7% q/q in Q3. The September decline was broad based with all the major categories falling except hospitality (+1.5% m/m). Motor vehicles sank 2.6% but consumables were down 0.5%, durables -0.8% and apparel -1.4%.

- Services fell 1% m/m while non-retail spending ex services was flat (includes healthcare but also travel).

NZ card expenditure y/y%