PRECIOUS METALS: Gold & Silver Range Trade Despite Lower USD & Weak ADP

Gold and silver range traded on Wednesday and finished little changed. They found support from disappointing US ADP jobs data but then trended lower following the services ISM print. Silver finished steady at $58.500/oz but is up 3.5% this week, while gold was down 0.1% to $4203.08/oz and is 0.9% lower this week.

- Precious metals found little support from the weaker US dollar (BBDXY -0.4%) and lower 2-year yield. December Fed rate cut pricing was slightly softer but still has 23bp.

- Silver reached $58.989, a new record, and then traded around $58.40. It fell to $57.558 late in APAC trading. It is has started Thursday around $58.51. A bullish price sequence of higher highs and higher lows continues.

- Gold rose to $4241.50 following the ADP employment data which showed a 32k decline in November after rising 47k. It then trended lower breaking below $4200 a number of times but not holding the moves. It is currently around $4206.9. Bullion remains in a bullish trend with initial resistance at $4264.7. Initial support is at $4125.2, 20-day EMA.

- Members of Italy’s PM Meloni’s party want to add to the upcoming budget legislation a clause that the country’s gold reserves “belong to the Italian people” but are managed by the central bank. The ECB has requested that the government reconsider this proposal as it could lead to sales.

- Equities were generally higher with the S&P up 0.3% and Euro stoxx +0.2% but FTSE down 0.1%. The S&P e-mini is currently slightly higher. Oil prices were up with Brent +0.6% to $62.80/bbl. Copper jumped 2.8%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (Z5) Returns Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.640 @ 16:08 GMT Nov 3

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures slipped lower Wednesday on the back of hotter-than-expected Australian inflation. This returned prices lower despite nascent signs of a technical recovery as recently as last week. The sustainability of the pullback will be dependent on prices holding above key short-term support at 95.510, the Sep 3 low. Near-term resistance remains 95.780, the Sep 12 high. A clear break of this level signals scope for a continuation higher and opens 95.960, the 76.4% retracement level for the Sep’24 - Nov’24 downleg.

AUSSIE 3-YEAR TECHS: (Z5) Struck by Strong CPI

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 96.345 @ 16:07 GMT Nov 3

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Having bounced well on the back of the mild US CPI print, Aussie 3-yr futures reversed course Wednesday on strong domestic inflation data containing RBA cut pricing through 2026. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 96.280 as the next major support.

AUSSIE BONDS: Slightly Cheaper Ahead Of RBA Policy Decision

ACGBs (YM x-1.5 & XM -1.5) are weaker after cash US tsys finish moderately weaker.

- Today is RBA Policy Decision day, with the Board likely to remain highly data-dependent and cautious given inflation's renewed shift higher and the emerging domestic recovery, but easing labour market conditions. (see MNI RBA Preview here)

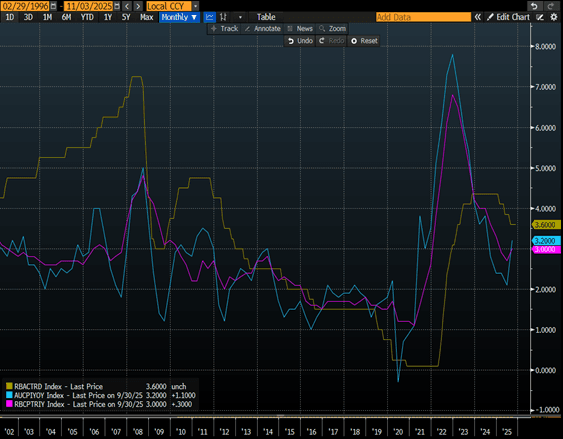

- Paul Bloxham (HSBC) argues that Australia’s labour market still appears tight, as inflation is rising even with unemployment at 4.3%. He questions whether the RBA may have already eased policy too much. Consequently, he does not expect further rate cuts and believes the next move in interest rates is more likely to be an increase. – AFR via BBG

- These thoughts appear consistent with the attached chart, which highlights that rising annual inflation tends to end easing cycles.

- Cash ACGBs are 1bp cheaper.

- The bills strip is flat to -2 across contracts.

- RBA-dated OIS pricing implies almost no chance of an easing, with just a 3% probability assigned. As it currently stands, the OIS market has only an 80% chance of a 25bp cut by mid-2026.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Wednesday and A$800mn of the 3.00% 21 November 2033 bond on Friday.

Bloomberg Finance LP