EMISSIONS: Global CO2 Emissions Set to Peak Around 2026 Before Gradual Decline

Oct-31 13:18

Global CO2 emissions are expected to peak around 2026 before beginning a gradual decline, according to Rystad Energy.

- The subsequent decline will likely be driven by rapid renewable deployment in power generation and EV adoption in transport.

- Current NDCs remain insufficient to limit warming to 1.5 degrees, with full implementation still falling short of the reductions required under the Paris Agreement.

- It expects the trajectory to be at 1.9 degree by 2035, citing the need for stronger policy signals and faster deployment to close the emissions gap.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US PREVIEW: ISM Manufacturing: Marginal Improvement Seen Continuing

Oct-01 13:17

Today's ISM Manufacturing survey (1000ET) is expected to see another rise in the headline index in September, to 49.0 from 48.7 prior for a 2nd successive improvement in activity albeit below the 50 mark for a 7th consecutive month.

- Recall: August's ISM Manufacturing report was weaker than expected on the headline figure, with some sub-components telling a slightly more mixed story, and price pressures unexpectedly diminished. Overall the ISM survey continues to portray a manufacturing sector that is failing to convincingly regain traction after the summer's tariff-related policy uncertainty. Indeed, tariffs were mentioned extensively in the sector-by-sector anecdotes in the report, and not in a positive light.

- September's flash US PMIs brought a 2-month low for Manufacturing at 52.0 (52.2 consensus, 53.0 prior). That report noted: "Higher output was reported in the manufacturing sector for a fourth consecutive month, but the expansion was much weaker than the strong gain (a 39-month high) seen in August. New order inflows in the goods-producing sector also weakened to only a marginal pace, in part due to an increased rate of loss of exports due to tariffs." The report also reported "lower job gains" in manufacturing in the month, with the sector seeing "more of a focus on job losses due to cost cutting."

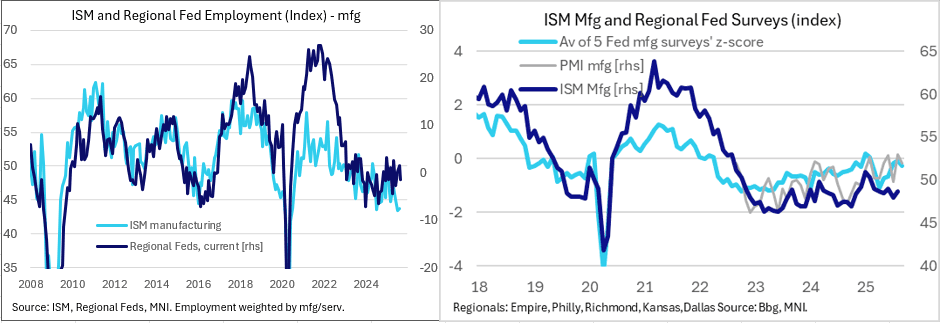

- September saw a very mixed round of regional Fed manufacturing surveys: The Dallas, NY, and Richmond Feds saw sizeable pullbacks in current activity vs August, while Philadelphia and KC saw big improvements.

- ISM New Orders are seen slowing to 50.0 (51.4 prior) with Employment up to 44.3 (43.8 prior). For Employment, regional Fed data has held up a little better than the national ISM series (see chart).

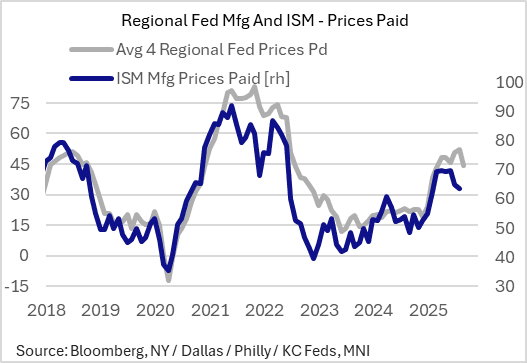

- Meanwhile, the ISM Manufacturing Prices Paid gauge is expected to tick down to 62.7 from 63.7 prior. This would mark a second consecutive monthly dip but still keep the prices gauge around the highest levels since late 2022. The expectation for a slight downtick in roughly accords with the proxy indicators we have seen.

- September's flash S&P Global PMI report noted "Manufacturing input price inflation remained elevated at one of the highest rates since the pandemic, albeit dipping slightly since August." Regional Fed manufacturing surveys showed pullbacks in NY, Philadelphia, Kansas City, and Dallas (Richmond, which reports % Y/Y changes, was steady).

MNI EXCLUSIVE: Former SOMA Desk Trader On Long End Rates

Oct-01 13:15

Former New York Fed trader Joseph Wang discusses how the central bank will deal with elevated long end rates -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

SOFR OPTIONS: BLOCK: Dec'25 SOFR Call Spd

Oct-01 13:14

- 5,000 SFRZ5 96.56/96.68 call spds, 1.25 ref 96.355 at 0910:53ET