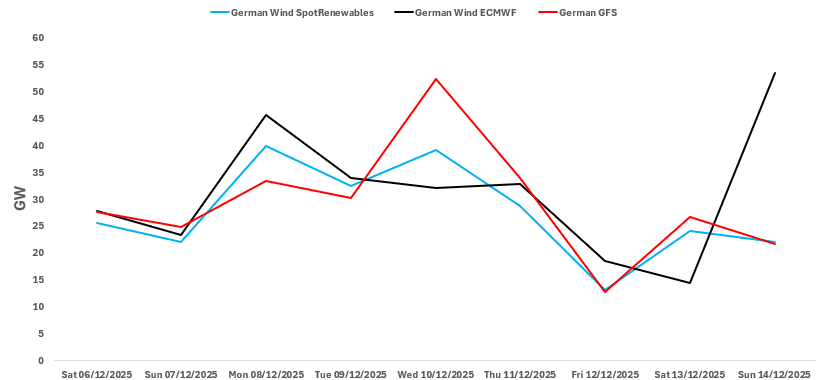

RENEWABLES: German Wind Output Forecast Comparison

See the latest German wind output forecast for base-load hours from SpotRenewables vs Bloomberg’s ECMWF and GFS models for the next seven days as of Friday afternoon.

- SpotRenewables and the German GFS model forecast similar wind generation levels on 12 December and 14 December. Meanwhile, SpotRenewables and the ECMWF models are comparable but deviations for all days are above 1GW.

- The largest deviation is noted when comparing the ECMWF model and SpotRenewables on 14 December at 31.4GW, with large deviations between GFS and SpotRenewables on 10 December at 13.2GW.

Despite these differences, all three models forecast wind output to be relatively volatile throughout the forecast period – which could lead to price swings on the German spot market.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Adding to the Large Outright Call

ERU6 98.50c, bought for 3.25 in 17.5k total.

US: Speaker Johnson Downplays Election Results

Speaker of the House of Representatives Mike Johnson (R-LA) has downplayed the significance of the results from elections across the country on 4 November. After a slew of Democrat wins, Johnson said, “What happened last night was blue states and blue cities voted blue. We all saw that coming, and no one should read too much into last night's election results. Off-year elections are not indicative of what's to come. That's what history teaches us.”

- For more analysis of the elections, see MNI's latest US Daily Brief: MNI POLITICAL RISK - 'Blue Wave' Fuels Democratic Optimism

STIR: Hawkish Extension In Fed Prices After ISM

The combination of a firmer-than-expected headline ISM services reading and prices paid sub-component (70.0) makes for an extension of the hawkish move in the USD front end.

- Note that the employment component remained in contractionary territory but wasn’t quite as soft as expected.

- Market now prices 16bp of easing for next month i.e. over 60% odds of a cut taking place, with a cumulative 24bp of easing showing through January, 31.5bp through March and 51.5bp through June.

- That compares to 17bp, 26bp, 35bp and 55bp ahead of the data.

- SOFR-implied terminal rate pricing moves to 3.13% vs. 3.09% seen ahead of the ADP employment release.