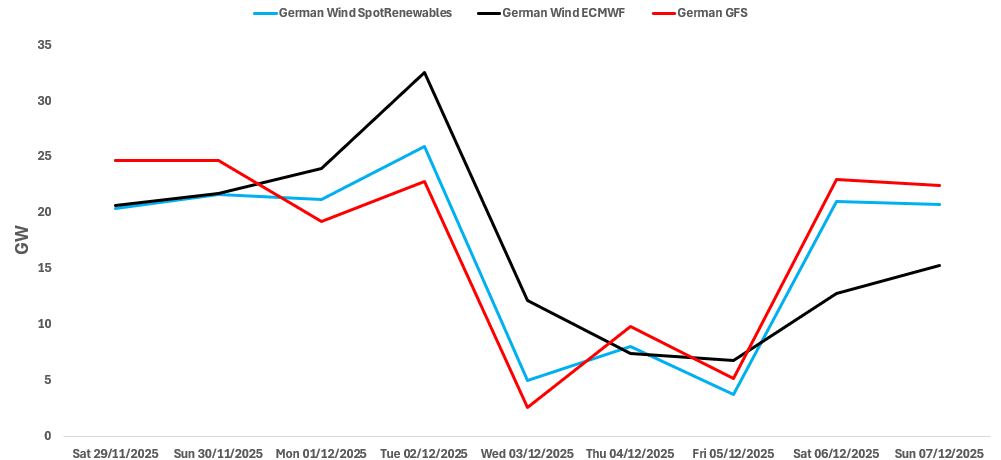

RENEWABLES: German Wind Output Forecast Comparison

See the latest German wind output forecast for base-load hours from SpotRenewables vs Bloomberg’s ECMWF and GFS models for the next seven days as of Friday afternoon.

- All three models suggest German wind generation to rise on 2 December, before easing back. Output is then forecast to increase again over 6-7 December.

- Bloomberg’s ECMWF sees the highest wind output on 2 December at 32.5GW, well above levels in the other two models.

- Bloomberg’s GFS model and the SpotRenewables model forecast wind output to rise above 20GW on 6-7 December, while the ECMWF model forecasts wind output between 12.8-15.3GW.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURGBP TECHS: Resumes Its Uptrend

- RES 4: 0.8865 1.764 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 3: 0.8848 1.618 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 2: 0.8835 High May 3 2023

- RES 1: 0.8818 Intraday high

- PRICE: 0.8812 @ 14:43 GMT Oct 29

- SUP 1: 0.8751 High Sep 25

- SUP 2: 0.8710 20-day EMA

- SUP 3: 0.8688 50-day EMA

- SUP 4: 0.8656 Low Oct 8 and a key support

A bull trend in EURGBP remains intact. Tuesday’s strong gains resulted in a clear break of resistance 0.8769, the Jul 28 high and a bull trigger. This, together with today’s extension, confirms a resumption of the uptrend and maintains the bullish price sequence of higher highs and higher lows. The 0.8800 handle has been cleared, sights are on 0.8835, the May 3 2023 high. Initial support lies at 0.8751, the Sep 25 high.

US TSY OPTIONS: US 5yr Put buyer

FVZ5 108.75p, bought for '04 in 2k.

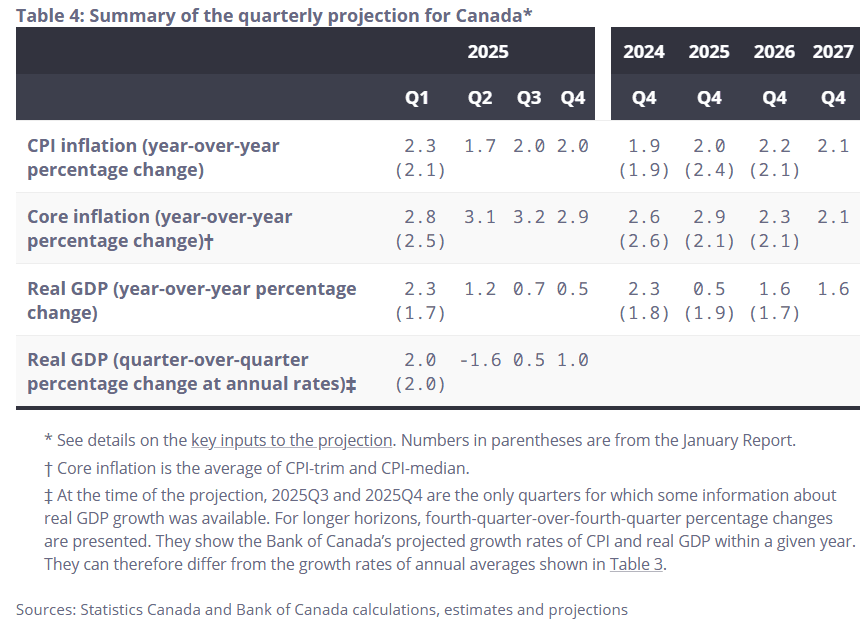

BOC: Monetary Policy Report Returns To Base-Case Forecast

As expected, the BOC's quarterly Monetary Policy Report (MPR) returns to a base-case forecast, after the scenario-based April and July reports. Even so as we cautioned in our meeting preview, we wouldn't put much stock in the new central projections because it was unlikely that the BOC itself would have a high degree of confidence in them (and indeed, the rate decision statement notes of the MPR: "Because US trade policy remains unpredictable and uncertainty is still higher than normal, this projection is subject to a wider-than-usual range of risks.")

- October's forecasts are presented relative to January's, so obviously a lot has changed.

- Versus that report, 2025 GDP is seen slower (1.2% vs 1.8%) as is 2026's (1.1% vs 1.8%), but compared with July's base-case tariff projections the GDP downgrades are minimal (was 1.3% 2025/1.1% 2026 in July). Potential output is seen as substantially lower vs January (2026 between 0.4-1.4%, vs 0.9-2.2% then).

- Inflation forecasts vs July's current tariff scenario are also a little higher, now 2.0% for 2025 (vs 2.3% Jan projection, 1.9% Jul) with 2026 2.1% (2.1% Jan, 2.0% Jul)

- Real GDP is seen picking up from -1.6% Q/Q SAAR in Q2, to +0.5% in Q3 and 1.0% in Q4, the Q3 figure being weaker than in July's current tariff scenario (1.0%), while core inflation is seen steadying out - from 3.1% Y/Y in Q2, to 3.2% in Q3 and 2.9% in Q4 (falling to 2.3% in Q4 2026), a slightly higher profile than seen in July's projections (3.1% in both Q2 and Q3, falling to 2.4% by Q4 2026).

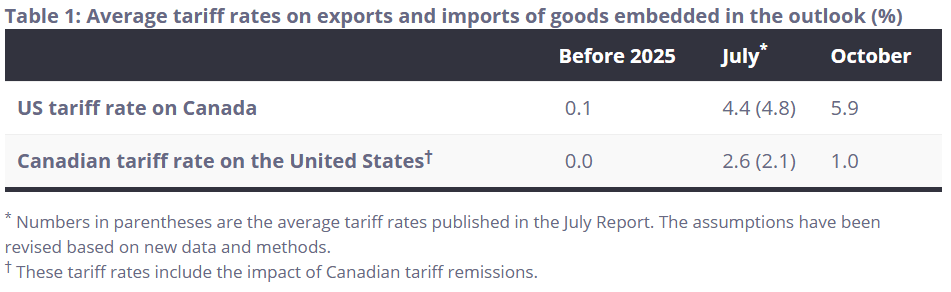

- Among other findings - the average tariff rates overall have obviously risen since pre-2025 amid the US-Canada trade conflict, but "only slightly since the July Report" with Canadian counter-tariffs on the US having been lowered since the July report. - see table. Echoing other estimates we've seen, "If steel, aluminum, motor vehicles and energy are excluded, then 94% of the value of goods entered the United States tariff-free."