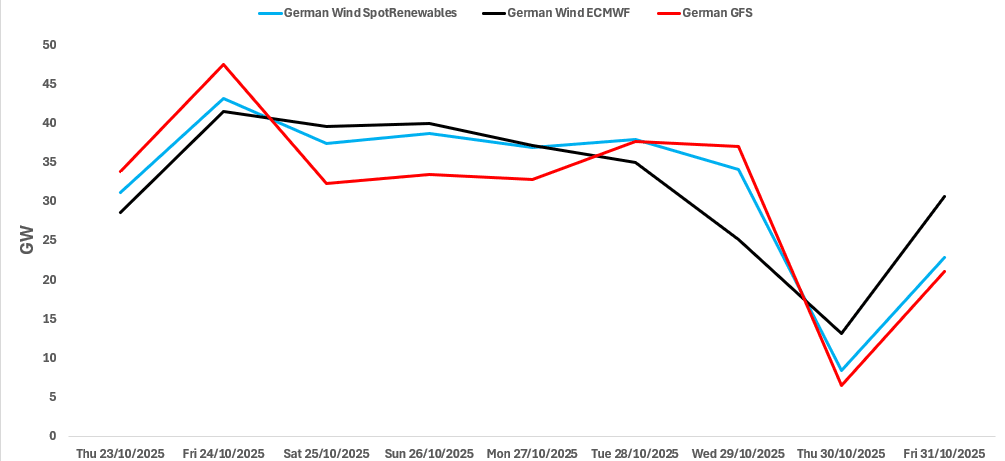

RENEWABLES: German Wind Output Forecast Comparison

Oct-22 15:19

See the latest German wind output forecast for base-load hours from SpotRenewables vs Bloomberg’s ECMWF and GFS models for the next seven days as of Wednesday afternoon.

- SpotRenewables and the German GFS model forecast similar wind generation levels on 27 October. Meanwhile, SpotRenewables and the ECMWF models have similar wind forecasts on 28 October.

- The largest deviation is noted when comparing ECMWF and SpotRenewables on 29 October, with the biggest difference between the GFS model and SpotRenewbales on 26 October.

Despite these differences, all three models still forecast wind output to be on a general downward trend from 25 October.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

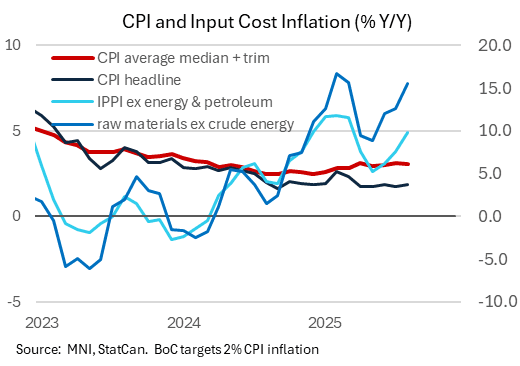

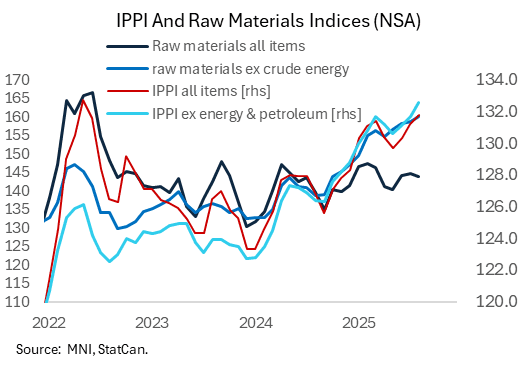

CANADA DATA: Industrial Price Pressures Remain Elevated

Sep-22 15:15

Industrial product and raw materials prices came in stronger than expected in August, with "core" measures showing some signs of acceleration. The implications for CPI aren't straightforward but there doesn't appear to be much price relief in the pipeline for or from Canadian producers.

- The Industrial Product Price Index (IPPI), which measures the prices of products manufactured in Canada, rose 0.5% M/M (NSA) vs consensus 0.1% (0.7% prior was unrevised). The ex-energy/petroleum index advanced 0.7% after 0.5%, with energy/petroleum products -1.3% after +2.7%.

- With these being non-seasonally adjusted figures, the Y/Y comparison is more apt for trend analysis: ex-energy/petroleum IPPI accelerated for the 4th consecutive month on a Y/Y basis, to 4.9% (3.8% prior, trough of 2.6% in May) for a 5-month high.

- The prices of raw materials purchased by manufacturers operating in Canada fell 0.6% M/M (NSA) in Aug, but ex-energy/petroleum rose 0.9%, per the Raw Materials Price Index (RMPI). The latter measure was up 15.5% Y/Y, vs 12.6% prior, for a 5-month high.

- The consumer price inflation implications aren't straightforward. IPPI has been distorted to the upside by a jump in precious / semi-precious metals prices (+36.3%), which as Statistics Canada points out "were supported by strong safe-haven investment demand over the 12 months ending in August" with the latest M/M uptick supported by expectations for a Fed cut in September.

- That said, there were pressures in food categories including fresh and frozen beef and veal (+28.9% Y/Y) and fresh and frozen poultry (+18.4%). Likewise, the raw materials increase Y/Y owes heavily to gold/silver/platinum group metal ores and concentrates up +37.0% Y/Y), though also very strong was cattle (+19.9%).

- Capital/durable goods inflation has been steadying out across various categories in IPPI albeit at elevated levels amid the US-Canada trade conflict. However food prices have already been on the relatively elevated side in CPI (3.4% Y/Y in August, double the rate of core goods at 1.7%), so this could be an area of more direct concern for the outlook.

FED: US TSY 26W AUCTION: NON-COMP BIDS $1.423 BLN FROM $73.000 BLN TOTAL

Sep-22 15:15

- US TSY 26W AUCTION: NON-COMP BIDS $1.423 BLN FROM $73.000 BLN TOTAL

FED: US TSY 13W AUCTION: NON-COMP BIDS $1.905 BLN FROM $82.000 BLN TOTAL

Sep-22 15:15

- US TSY 13W AUCTION: NON-COMP BIDS $1.905 BLN FROM $82.000 BLN TOTAL