EUROPEAN INFLATION: German HICP Confirms Flash, Broad-based Goods Pullback

Jan-16 07:52

- German HICP confirmed flash estimates at 2.0% Y/Y in December, down from 2.6% in November. As noted after the flash release, some caution is warranted when interpreting the Y/Y figure, which looks to be heavily influenced by a base effect after a seasonally strong 0.7% M/M rise in December 2024.

- Goods inflation was soft in December. Clothing and footwear eased to -0.7% Y/Y (vs 0.5% prior), while furnishings and household equipment was -0.5% Y/Y (vs 0.2% prior). Vehicle inflation and several recreation and culture categories also decelerated.

- Services was stickier, with rents at 2.2% Y/Y (vs 2.1% prior), insurance rising to 5.4% Y/Y (vs 4.8% prior) and accommodation services at 3.5% Y/Y (vs 3.0% prior). Meanwhile, recreation and culture services eased to 3.3% Y/Y (vs 3.8% prior), and transport services pulled back to 7.1% Y/Y (vs 7.6% prior, driven by the rail fares component). The volatile package holidays category pulled back to 4.1% (vs 6.7% in Nov, 3.6% in Oct).

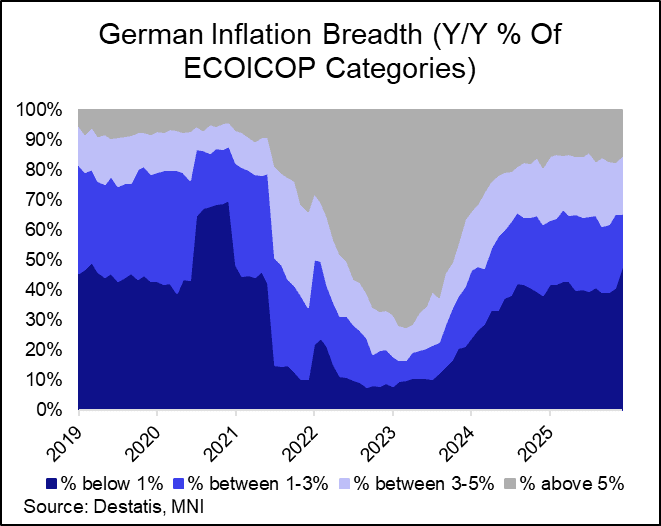

- The proportion of HICP ECOICOP categories with annual inflation rates below 1% Y/Y increased to 47.8% in December, the most since 2020. Meanwhile, the proportion of components with high inflation rates above 5% Y/Y eased to 15.6% (vs 17.4% prior).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Sharp Dovish BoE Repricing On Soft UK CPI, Market Leans Towards 3 Cuts

Dec-17 07:51

Soft UK CPI data drives a fresh dovish leg of repricing in GBP STIRs, although market implied terminal rates continue to struggle to push meaningfully below 3.30%, as has been the case during instances of dovish repricing seen recent weeks.

- BoE-dated OIS 1.5-9.5bp more dovish across liquid contracts. 23.5bp of easing is priced for tomorrow’s decision vs. ~22bp late yesterday, while the strip is now pricing ~69bp of easing through end of ’26 vs. ~60bp late yesterday.

- SONIA futures are 2.0-9.0 higher, SFIZ6 prints an incremental year-to-date high (96.720) SFIZ5/Z6 registers a fresh cycle low at -44.0.

- A reminder that the CPI data looks pretty soft across the board.

- With a cut for tomorrow effectively cemented, one question now is will there be enough in the data to convince any additional "hawkish" member, in addition to Governor Bailey, to support a cut. The market is very much looking for a 5-4 split on the MPC, so a 6-3 vote tomorrow would be a surprise (5-4 remains our base case).

EGB OPTIONS: Schatz Call Condor

Dec-17 07:37

DUG6 106.90/107.00/107.10/107.20c condor, bought for 1.5 in 2k.

UK DATA: Broad-based downside surprises

Dec-17 07:29

Downside surprises from services, core goods and food inflation all behind the UK CPI miss,.

- Core goods the big downside driver here - so it may be an early Black Friday sales driver helping here. Clothing as well as furniture and household goods look soft at first

- Within services, accommodation looks soft at -0.95%Y/Y (+0.82%Y/Y in Oct) as well as cultural services.

- This looks like a pretty soft print across the board and seems to very much reinforce the expectation that we will see a cut tomorrow.

- One question now is will there be enough in this data to convince any additional "hawkish" member in addition to Bailey to support a cut here. The market is very much looking for 5-4 so a 6-3 vote tomorrow would be a surprise (5-4 remains our base case, however).