BUNDS: German 30yr Yield breaks above the highlighted level

* Bund is now through 125.31 Yesterday's low, not seen as a support with the area of interest comi...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

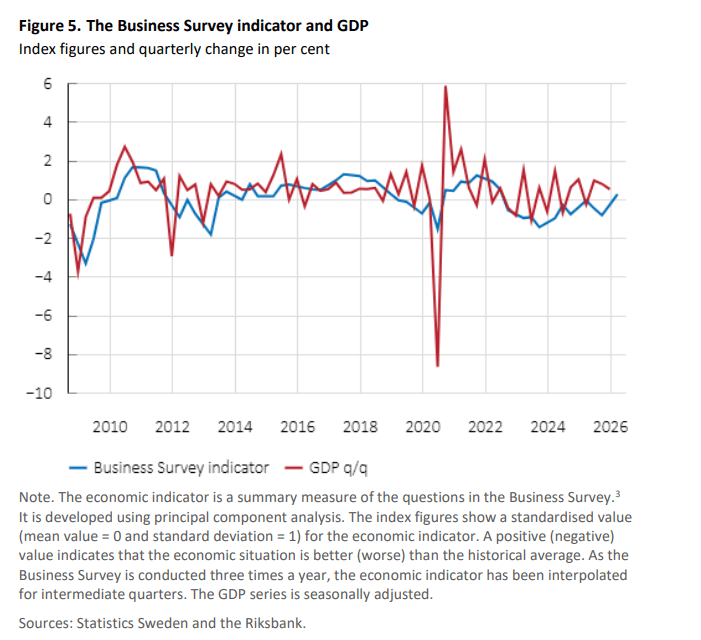

SWEDEN: Mixed Signals From Business Survey, Strengthens Case For Steady Rates

The key caveat with the Riksbank’s February Business Survey is that interviews were mainly carried out between Jan 29 – Feb 9. As such, it doesn’t capture any direct impact of the Middle East War.

With that in mind, the results are mixed, with a few dovish signals but otherwise confirmation that a tentative economic recovery is underway. Overall, we continue to think that the Riksbank will once again signal plans to hold rates at 1.75% "for some time" at next week's decision, but stress a wider range of potential outcomes than before.

- Respondents suggested that a geopolitical shock would increase consumer’s marginal propensity to save, and many companies note that consumer behaviours is limiting the ability to raise prices above inflation.

- However, there were no comments around whether a rise in energy prices (as has been seen in the current environment) would force companies to raise prices even if it meant sacrificing demand.

- The Business Survey indicator did strengthen relative to last quarter, and is now above the historical average: “It is primarily companies' hopes that demand will strengthen that are contributing to the rise in the indicator”

Some highlights from the report:

- “Large Swedish companies are experiencing some improvement in economic activity, but the recovery is both slow and hesitant. “

- “Companies that sell goods and services to households describe the situation in somewhat brighter terms compared with last autumn. Households’ willingness to consume has strengthened “…. “companies see a risk that global events may cause households to tighten their purse strings again.”

- “Among manufacturing companies, the view of the economy is more divided than usual. The uncertain geopolitical situation reinforces the disparity between sectors.”… “The appreciation of the krona is having a negative impact on the earnings of export companies, but it is above all the fluctuations in the exchange rate that are perceived as challenging.”

- “Non-durable goods retailers plan to reduce their selling prices when VAT on food is temporarily reduced. Other retailers and companies selling services to households instead plan to increase selling prices in line with inflation. They emphasise that households' price consciousness is dampening pricing plans.”

- “Almost all companies use AI in their operations. But they mainly use AI to increase productivity with existing staff, not to reduce headcount.”

GILTS: Bear Flattening, Futures Through First Support

Gilts sell off with oil bid through early London trade, while hawkish comments from an ECB Governing Council member provide spillover pressure from Bunds.

- Futures trade as low as 90.51, breaching initial support located at the March 9 high/gap support (90.54). Bears look to the March 6 low (89.43) next.

- Conversely, bulls need to break the 20-day EMA (91.68) to turn focus higher.

- Yields 7-10bp higher, curve flattens. Pre-existing week-to-date yield highs remain untested across benchmarks.

- Flattening driven by reduction in pricing of BoE rate cuts.

- Short end last discounting 5bp of easing through July, with contracts as much as 14bp less dovish for late ’26 meetings.

- BoE’s Breeden will speak in front of the House of Lords Financial Services Regulation Committee this morning, but will cover Stablecoins, so don’t expect much on monetary policy.

- That will leave geopolitical matters and related oil volatility at the fore.

FRANCE DATA: Bank of France See Q1 GDP At 0.2-0.3% Q/Q, Now With Downside Risk

Released yesterday: "GDP could grow between 0.2% and 0.3% in the first quarter", from the Banque de France's monthly business survey for March (unchanged from Feb), though they now note downside risk due to the Middle East conflict. While the conflict is yet to show in hard economic data, we are seeing the first signs of concern over downside risks that could stem from the conflict.

- "However, this technical forecast is subject to downside risk, given the uncertainties related to the conflict in the Middle East and its impact on supply chains and energy prices, which could weigh on activity at the end of the quarter."

- The growth estimate is unchanged from the February survey, and is also in line with Bloomberg consensus at 0.2% Q/Q. This would also be unchanged from 0.2% Q/Q realised growth in Q4 2025. Further ahead, growth is seen staying in the 0.2-0.3% Q/Q range for the remainder of the year (Bloomberg consensus).

- Data were collected between 25 Feb - 4 Mar 2026, covering around 8500 businesses: "about one-third of the responses were collected before [events in the Middle East] and two-thirds after. For February, according to the business leaders surveyed, economic activity continued to grow at a pace consistent with expectations."

- "For March, businesses anticipated continued strong activity in industry and services, and more limited activity in construction. However, while uncertainty continued to decline in the initial responses prior to February 28, it rebounded sharply in subsequent responses, with businesses citing risks of rising energy prices and logistical disruptions."

- We note that French hard output data has been more mixed recently: IP rebounded in Jan at 0.5% M/M (0.4% cons, -0.5% prior, revised up 0.2ppt), but entirely due to a strong rebound in transport equipment (all other manufacturing categories saw flat/negative growth M/M).

- Elsewhere in the survey, it's noted that "price increases remain moderate ... Overall, 11% of industrial companies reported increasing their selling prices in February, while 5% reduced them. Price decreases were mainly seen in the automotive (-12%), pharmaceutical (-10%), and food processing (-10%) sectors. Price increases were more concentrated in pharmaceuticals (+28%), computer, electronic, and optical products (+17%), and electrical equipment (+15%)."