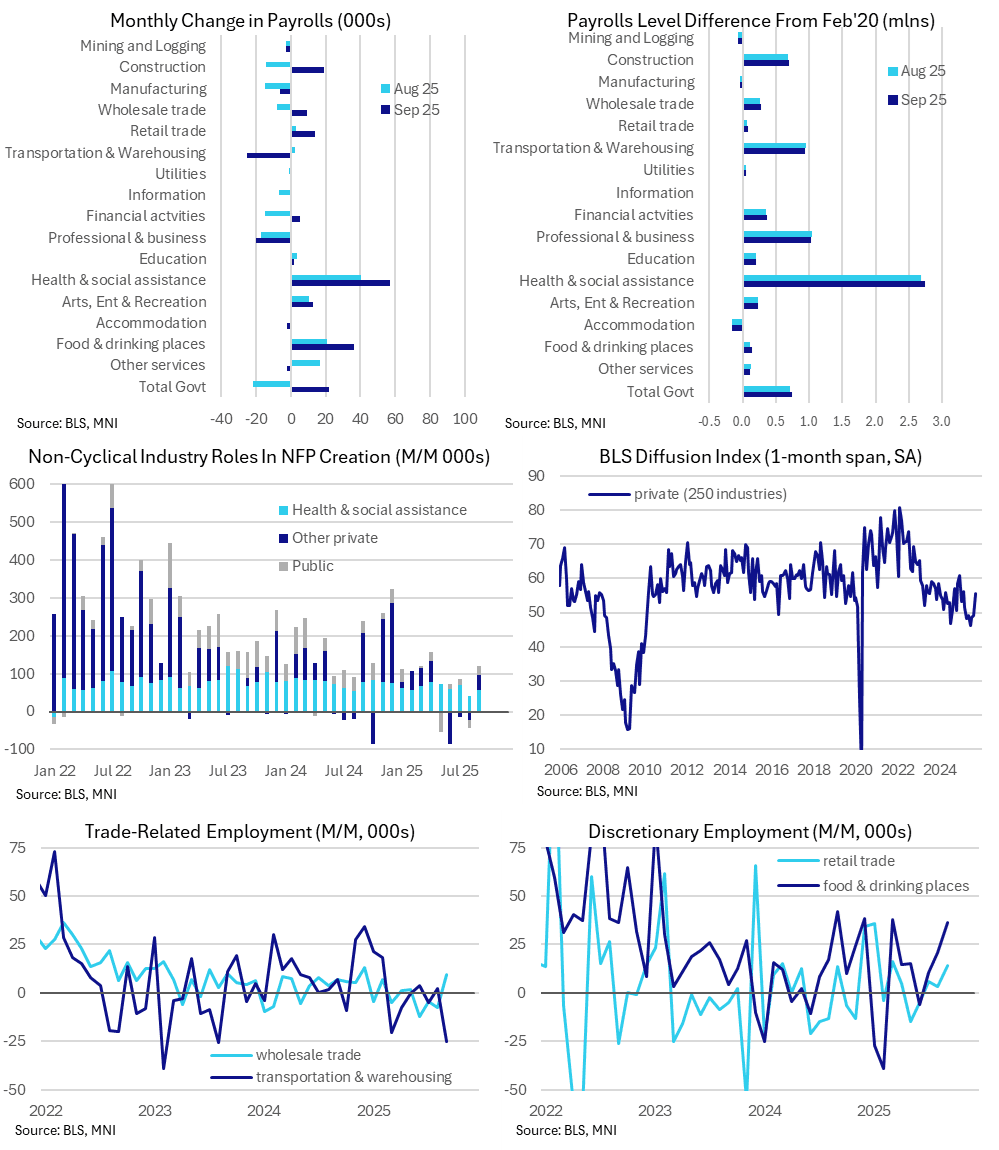

US DATA: Genuine Improvement On Payrolls Side Of September Jobs Report

Separate to the weaker household survey with its push higher in the u/e rate, the payrolls data in the establishment survey were stronger than expected in September. Trend growth rates are at the lower end of the range of breakeven estimates rather than pushing more materially below. Further, September alone saw the first net job creation for private industries outside of health & social assistance since April, albeit after some heavy cumulative declines since then.

- September’s report put nonfarm payrolls growth at a stronger than expected 119k in September (cons 51k), following a downward revised August to -4k (22k initially) after 72k in July (from 79k) and -13k in June.

- Private payrolls were weaker on net though, increasing 97k (cons 65k) in a surprise that was offset by a two-month revision of -41k (spread over both August and July).

- Looking through monthly volatility, three- and six-month averages for both nonfarm and private sector payroll growth stand close to 60k per month in the latest vintage of data.

- That’s at the low end of recent estimates for breakeven payrolls growth rather than pushing more clearly below them.

- Within the details, a 57k increase in the cyclically insensitive health & social assistance sector after 40k in August takes a little of the gloss off the latest private sector strength.

- Still, it’s notable that private sector job creation ex health & social assistance increased 40k, its first increase since April having lost -126k through May-Aug.

- Other main positive drivers were food & drinking places (37k after 21k), construction (19k after -14k), retail trade (14k after 3k for its highest since March) and arts, entertainment & recreation (13k after 10k).

- The main drags came from transportation & warehousing (-25k after 3k for its weakest since Aug 23), professional & business services (-20k after -17k) and manufacturing (-6k after -15k).

- The 97k private payrolls growth is in firm contrast with the -29k in the September ADP report, which subsequently improved to 42k in October. Large discrepancies in September come from leisure & hospitality employment (+47k for payrolls vs -16k for ADP) and construction (+19k for payrolls vs -4k for ADP), along with the education & health category (59k vs 25k) which has seen large gaps over the past year.

- Supporting a rosier September, the 1-month diffusion index increase to 55.6, its highest since February after five months below 50 (with <50 indicating more than half of the 250 industries monitored declined on the month).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Late Morning Equities Roundup: Early Whipsaw Trade, Back Higher

- Stocks are trading mixed early Tuesday, whipsawing off early session highs - apparently after Pres Trump social media post warning retribution "if Hamas continues to act badly, in violation of their agreement with us."

- While Treasury futures extended early highs (10Y yield fell to 3.9455%), equities managed to recover off lows by midmorning. A noticeable exception: mining stocks underperformed after Gold fell sharply (appr -240.0 at 1050ET to 4115.0, appr -6.3% from session highs).

- Currently, the DJIA trades up 389.05 points (0.83%) at 47,095.25, S&P E-Minis up 10.5 points (0.16%) at 6,784.5, Nasdaq down 32.2 points (-0.1%) at 22,959.71.

- In addition to Materials and Utility Services sector share underperformed: Philip Morris Int -9.54%, Newmont -9.52%, Vistra Corp -3.58%, Albemarle Corp -3.51%, Quanta Services -3.49% and NRG Energy -3.38%.

- On the positive side, Consumer Discretionary and Industrials sector shares outperformed in the first half, General Motors surged +14.76% after reporting better than expected Q3 earnings, CarMax +3.97%, Ford Motor +3.96%, Lululemon Athletica +3.27% and Expedia Group +2.94%.

- Supporting the Industrials sector: RTX +8.39%, 3M Co +4.66%, PACCAR +2.78% and Stanley Black & Decker +2.78%

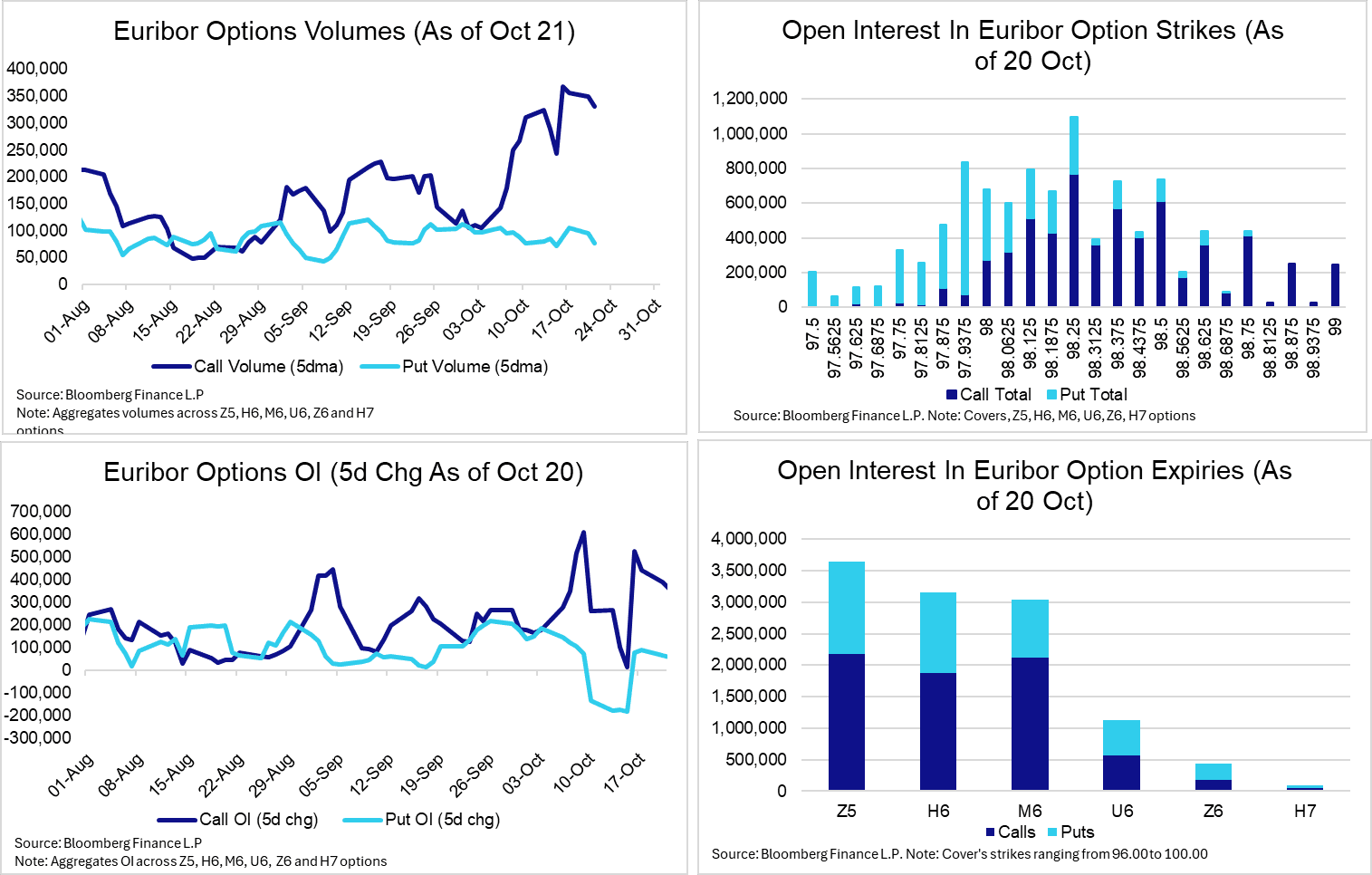

EURIBOR OPTIONS: More Moderate Activity Still Favours Calls; Flash PMIs In Focus

Euribor options activity has moderated a little compared to the previous two weeks, but remains healthy. Participants continue to eye Friday’s October flash PMIs for the next update on Eurozone growth momentum. A weak set of figures would work in favour of recent upside interest, and potentially spur a fresh round of positions looking for an additional ECB rate cut this cycle.

- Call volumes and OI changes continue to outstrip puts. Note that while this has encompassed familiar upside structures expiring in the first half of next year, we’ve also seen examples of paper selling call spreads in the last few sessions.

- Front-end vol has rebounded modestly this month, which alongside rallies in outright futures has benefitted dovish option structures bought in recent weeks. We’ve previously noted significant interest in M6 options, with participants likely viewing the June 2026 expiry as providing sufficient flexibility around the potential timing of an additional ECB rate cut.

- The price of a 98.75 M6 call bought for 1.25 ticks on October 10 has now crept up to 1.75 ticks (data according to Bloomberg).

- Open interest in M6 options currently totals just over 3 million contracts, skewed towards calls. This is only slightly below total H6 option OI (data as of yesterday).

- The 98.25 strike continues to command the largest OI across the next 18 months’ worth of options expiries.

BELGIUM AUCTION PREVIEW: On offer next week

Belgium has announced it will be looking to sell the following at its auction next Monday, October 27:

- the 2.60% Oct-30 OLO (ISIN: BE0000365743)

- the 1.25% Apr-33 Green OLO (ISIN: BE0000346552)

- the 3.10% Jun-35 OLO (ISIN: BE0000363722)

A reminder that Belgium just cancelled their November 24 OLO auction, making next Monday's offering the last one of the year. The size announcement for the auction will follow this Friday.