US DATA: GDP Revision Shows Domestic Demand On Weaker Footing Than Seen Earlier

Jun-26 13:05

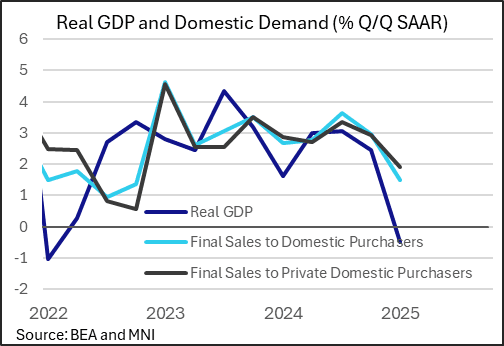

The main takeaway from the final revision to Q1 GDP is that not only was growth overall weaker than previously estimated, but that it was domestic demand rather than idiosyncratic factors in the quarter that largely drove the lower revision. Overall the data shows consumer demand on a weaker footing than previously seen going into a volatile Q2.

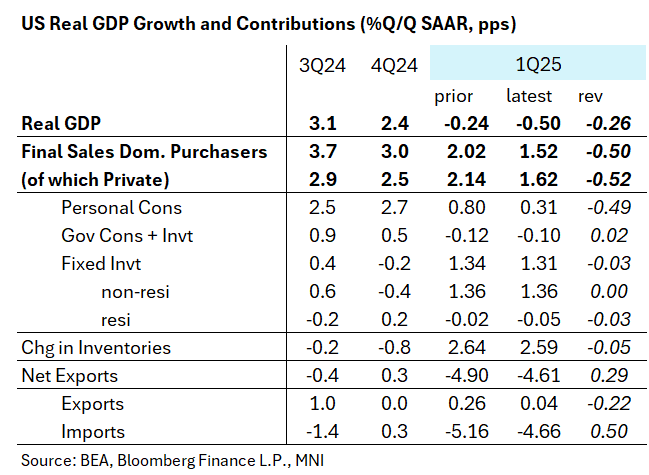

- Real GDP growth is now estimated at -0.50% Q/Q SAAR, down from the prior -0.24% estimate.

- While final sales to private domestic purchasers (PDFP) - the Fed's key guide to underlying demand - continued to drive growth, it was significantly weaker than in the prior estimate, contributing 1.6pp to GDP, vs 2.1pp. That in turn was due to a sharp downward revision in personal consumption expenditures, which are now seen to have contributed just 0.3pp to GDP vs 0.8pp previously seen.

- To put this into perspective, the initial read for PDFP was 3.0%, revised down to 2.5%, but now to 1.9%, which is the weakest since Q4 2022. Private consumption is now seen as having grown just 0.5%, vs 1.8% in the initial read and 1.2% in the second. That is the weakest since Q2 2011 (excluding the sharp Q2 2020 drop due to pandemic).

- Net exports dragged on headline GDP less than expected too: -4.6pp (previously est -4.9pp), due largely to less of a subtraction from the inventories column.

- Investment, government spending, and inventories were all relatively steady vs the previous estimates.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US Q1 FHFA HPI Q/Q SA +0.7% V +4.0% Q1 2024

May-27 13:00

- MNI: US Q1 FHFA HPI Q/Q SA +0.7% V +4.0% Q1 2024

MNI:US MAR FHFA HPI SA -0.1% V +0.0% FEB; +3.7% Y/Y

May-27 13:00

- MNI:US MAR FHFA HPI SA -0.1% V +0.0% FEB; +3.7% Y/Y

SOFR: Put Ladder seller

May-27 12:56

SFRU5 95.87/95.75/95.68p ladder, sold at 5 in 2.5k.