MALAYSIA: GDP Preview

- Following the first rate cut in five years today's GDP has the potential to be weaker than expected.

- The BNM cut rates in what was seen as an attempt to preserve growth.

- Q1 growth saw an uptick in Government spending offset a modest decline in private spending and a sizeable decline in investment

- Export and Import growth had moderated in Q1.

- Following a Q1 result of +4.4% the market forecasts a +4.2%.

- Given what (for some) was a surprise move by the BNM, today's print has the potential for being weaker than expected.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LNG: European Gas Higher As Vulnerable To Middle East Disruptions

European natural gas rose 3.4% to EUR 39.21 after a high of EUR 39.74 driven by growing concerns of an escalation in the Iran-Israel conflict resulting in a disruption to LNG shipments. Prices are now up 14.6% in June.

- Energy markets reacted to prospects of the US assisting Israel in its attacks on Iran after President Trump left the G7 early. He has demanded that Iran surrender but said that they won’t assassinate the Ayatollah “for now” but his patience with Iran is “wearing thin”.

- An escalation of the conflict especially if the US gets involved could prompt Iran to disrupt tankers through the Strait of Hormuz which carries 20% of global LNG exports. This scenario would drive gas prices sharply higher and add to Europe’s challenge of refilling storage ahead of winter, which is making the market very sensitive to disruption risks.

- Qatar, the world’s third largest LNG exporter in 2024, has asked tankers to wait outside the Strait until they can be loaded, according to Bloomberg. Also, some companies are not taking new bookings and the conflict has resulted in the jamming of navigational equipment, which resulted in two tankers colliding and catching fire off the coast of the UAE.

- The EU presented plans to end pipeline and LNG gas imports from Russia, which account for around 13% of total imports. It will be gradual but more reliant members are reluctant as they fear higher prices, reported by Bloomberg.

- US gas rose 3.2% to $3.87 to be up 12.2% in June as cooling demand is expected to rise towards month end. It is up another 1.1% to $3.89 today as Middle East tensions could drive demand for US LNG higher.

- PM Carney said that Canada could become a “LNG superpower”.

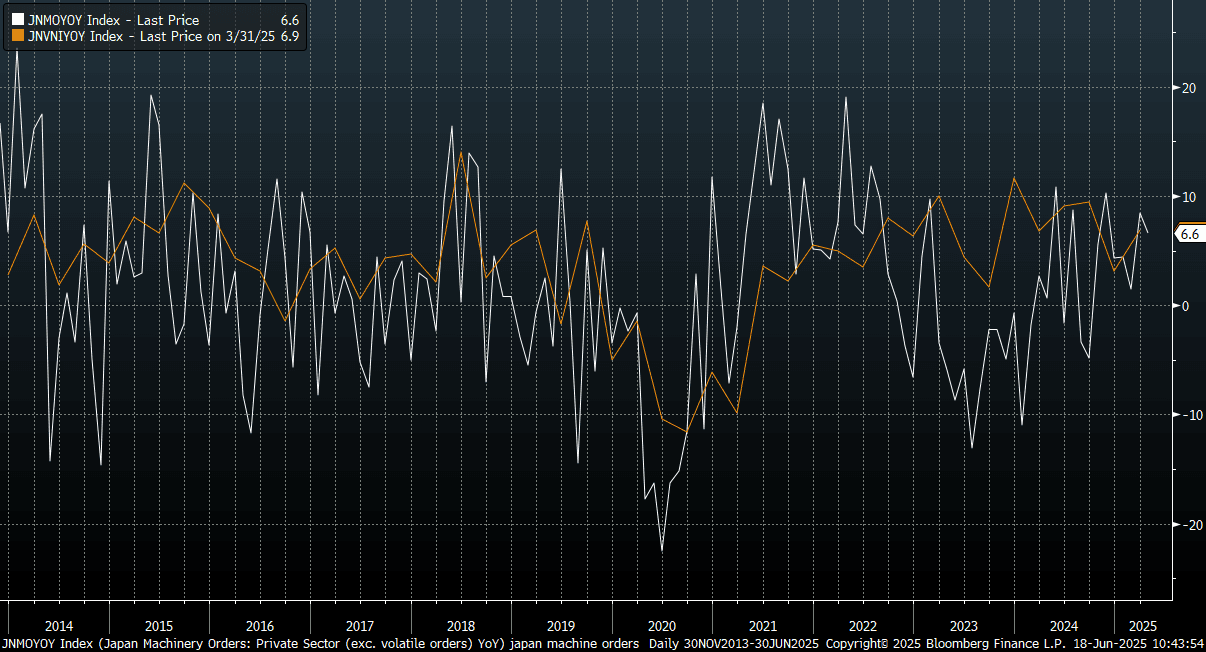

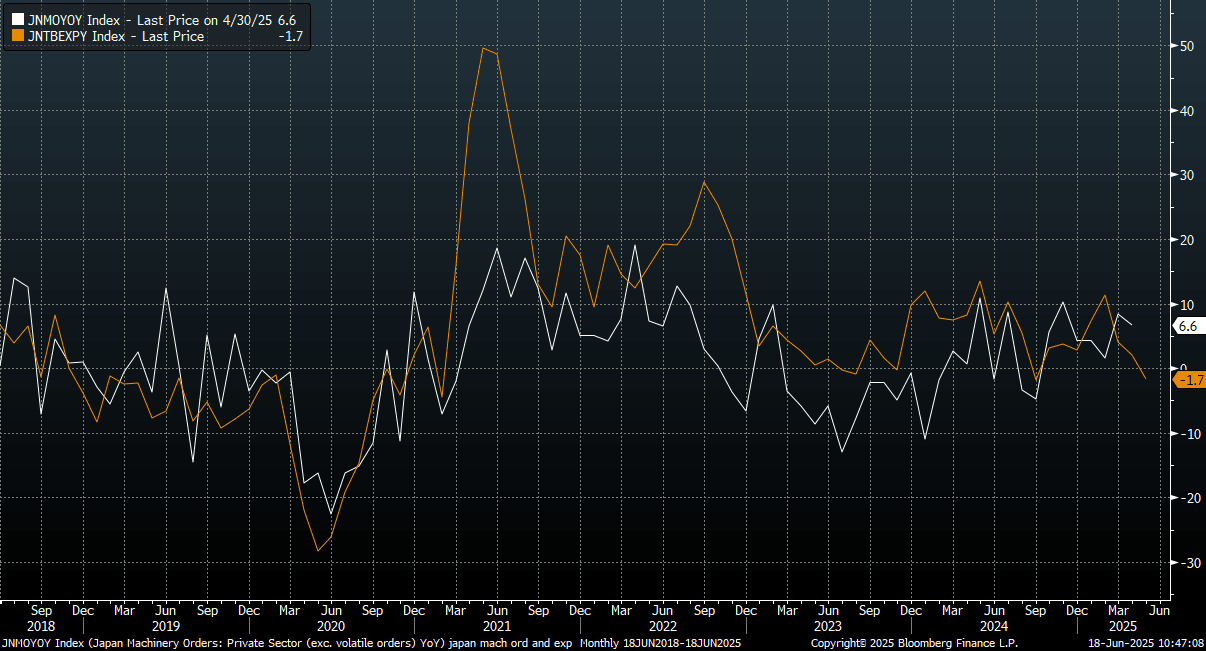

JAPAN DATA: Core Machine Orders Dip In April, Weaker Exports May Weigh

Japan April core machine orders fell sharply, but in line with market projections. We were down -9.1%m/m (-9.5% forecast and following a 13.0% gain in March). In y/y terms, we were slightly better than forecasts at +6.6% (+4.2% was projected, while 8.4% was the March outcome).

- The chart below plots core machine orders y/y (the white line on the chart) against a Japan Capex (ex software), which is also in y/y terms. It's still painting a fairly resilient backdrop in the earlier stages of Q2.

- Still, this comes ahead of trade headlines, with earlier data showing faltering export growth. The second chart below plots the machine orders against export growth (y/y), which is the orange line on the chart.

Fig 1: Japan Core Machine Orders & Capex (Y/Y)

Source: Bloomberg Finance L.P./MNI

Fig 2: Japan Core Machine Orders & Exports (Y/Y)

Source: Bloomberg Finance L.P./MNI

NEW ZEALAND: Q1 GDP Forecast To Print Higher Than RBNZ Expected

Q1 GDP prints on Thursday June 19 and is Bloomberg consensus is forecasting the production-based measure to rise 0.7% q/q again bringing the annual rate to -0.8%, higher than forecast by the RBNZ in May. The central bank is expecting a rise of 0.4% q/q. Activity at the start of 2025 was likely boosted by the agricultural and manufacturing sectors with exports supporting expenditure-based growth. With rates now in the “neutral zone” and RBNZ Governor Hawkesby saying the MPC doesn’t have a bias, and especially if GDP prints stronger than it expects, the RBNZ may be on hold on July 9.

- Forecasts range from 0.4% to 0.8% q/q but the major local banks are all in line with consensus projecting a 0.7% q/q rise.

- This data is dated as it covers the period before key US tariffs were announced and includes frontloading of exports to the US to beat any duties. The resultant heightened uncertainty makes the outlook very clouded and export growth is vulnerable.

- On a positive note, there are signs that NZ’s construction sector has begun to recover helped by 225bp of easing.