FED: GDP-Labor Market Disconnect Comes To Fore In Data "Fog" (2/2)

Having pushed back against the idea that the Fed was on autopilot going into end-year, one of the key questions was how the Fed would make its next rate decision in the absence of “official” government data during the ongoing federal shutdown. Powell didn’t quite endorse but likewise didn’t push back against the notion that the Fed could skip a December cut in light of the data “fog”: “what do you do if you are driving in the fog? You slow down…I don't know how that will play into things. We may get the data -- the data may come back, but there is a possibility it would make sense to be more cautious about moving. Again, I am not committing to that, but I am saying it is certainly a possibility that you would say, we really can't see, so let's slow down.”

- That appeared to raise the bar to what was already going to be a data-dependent cut in December: it may be that without tangible evidence of further labor market weakness and given apparent underlying strength in the economy, the FOMC’s default position may not be to ease again in December, but rather to wait to gather more information.

- Asked if today's cut was a close call, Powell said that aside from the two dissents in opposing directions there was a "strong, solid vote in favor of this cut". But the "strongly differing views" at this meeting were "really about the future". "And I think people are saying, they're noticing stronger economic activity....In the meantime, we see a labor market that's kind of, I don't want to say stable, but it's not clearly declining quickly. In any case, it may be just continuing to gradually cool again.”

- Overall Powell sounded a lot like Gov Waller who in an inter-meeting speech highlighted that there was a disconnect between apparently strong economic growth and nascent weakness in the labor market. Powell: “I think for some part of the Committee, it's time to maybe take a step back and see whether there really are downside risks to the labor market, or see whether, in fact, the stronger growth that we're seeing is real. Ordinarily, the labor market is a better indicator of the momentum of the economy than the spending data. In this case that gives a more downbeat read.”

- Waller of course this month had sounded a slightly more cautious note than he previously did on cuts beyond October, arguing that the ultimate path of monetary policy would depend on how the employment-GDP disconnect resolved - a sentiment that appears to have carried over into Powell’s messaging.

- It wasn’t all hawkish: Powell sounded dovish on inflation, saying that the September CPI report "was a little softer than expected", and that "inflation away from tariffs is actually not so far from our 2% goal” while inflation expectations remained well-behaved.

- But Powell was clearly seeking to convey that the FOMC saw more optionality in making its next decision, and on that front he was successful.

- As noted, rate markets are now pricing in closer to a 65% implied probability of a December cut, vs closer to 90% before the meeting.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: VP Vance: Think We're Headed To A Government Shutdown

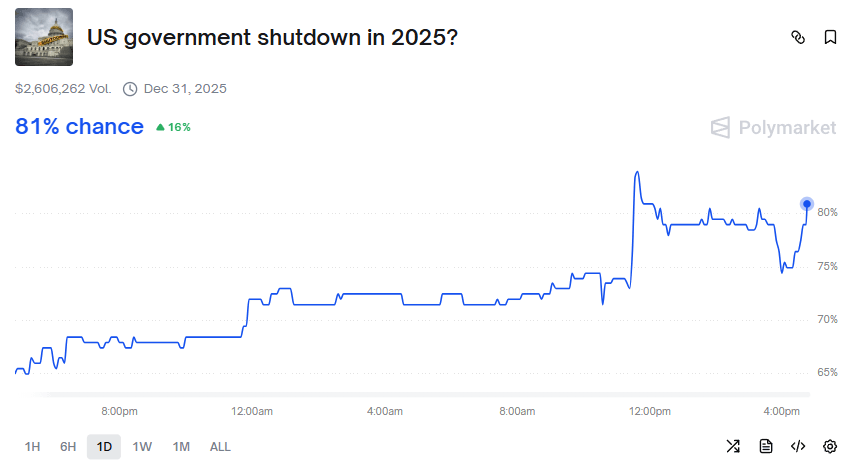

The Democratic congressional leadership's meeting with the White House has concluded, some headlines that suggest only limited if any progress has been made toward avoiding a federal government shutdown on Oct 1. Limited financial market reaction (equity futures dip slightly) but prediction markets' implied probabilities of a shutdown are beginning to pick up (Polymarket back over 80%). Some selected Bloomberg headlines:

- "*SCHUMER: WE MET WITH TRUMP, WE HAVE LARGE DIFFERENCES"

- "*VANCE: I THINK WE'RE HEADED TO A GOVERNMENT SHUTDOWN"

- "*JOHNSON: IF DEMOCRATS DECIDE TO SHUT DOWN GOV, IMPACT'S ON THEM"

FED: Deputy SOMA Manager Eyes Signals Of Reserve Regime Shift

Deputy SOMA Manager Remache of the NY Fed commented today at an annual meeting with primary dealers that system reserves appear to be "still abundant".

- "Our indicators currently suggest that reserves are still abundant. But we have observed some firming of repo rates recently, in part due to the increase in bill supply after the debt ceiling resolution, and continued pressures are likely over time given ongoing Fed balance sheet reduction. We have also started to see some movement in the distribution of federal funds transactions in response to higher repo rates—which is a healthy sign of market linkages, and exactly what we would expect. Most recently, this has translated to a one-basis-point increase in the EFFR relative to IORB."

- The Standing Repo Facility has been effective so far: "The SRF has been much less extensively used than the ON RRP to date, since reserves have been abundant over recent years. But as reserve levels fall this is shifting somewhat, with the SRF used at the recent June quarter end and at the mid-September tax date. On those occasions it worked consistent with its design, providing funds into the market when market rates rose above the SRF minimum bid rate. By doing so, the SRF can stem incipient rate pressure that, if left unaddressed, could threaten rate control."

- However: "Observing a more substantial shift in the EFFR relative to IORB, and changes in our set of reserve ampleness indicators, would be consistent with transitioning from abundant toward a more ample level of reserves. The Committee has indicated that it will consider stopping balance sheet runoff when we reach that point...When market conditions suggest reserves are ample, we will provide those liabilities by beginning to grow our balance sheet once again. At that point, the Committee would direct the Desk to resume purchases of Treasuries for the SOMA portfolio to maintain an ample level of reserves."

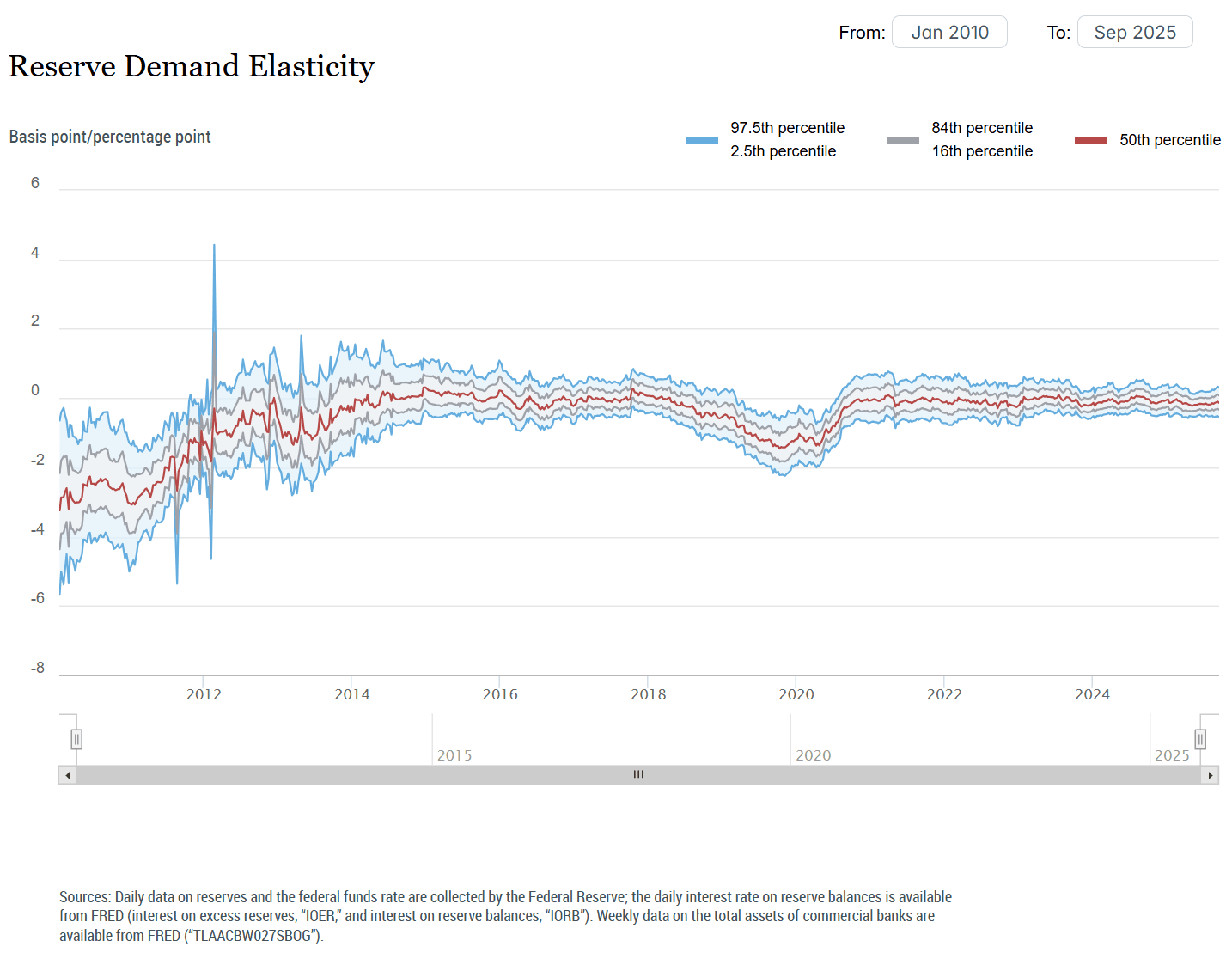

- The NY Fed's latest Reserve Demand Elasticity (RDE) indicator only goes through September 19 but suggests limited pressure through that period (the September update: "The elasticity of the federal funds rate to reserve changes is very small and statistically indistinguishable from zero. The estimate suggests that reserves remain abundant."

USDCAD TECHS: Northbound

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3968 High May 20

- RES 1: 1.3959 High Sep 26

- PRICE: 1.3920 @ 16:19 BST Sep 29

- SUP 1: 1.3885/3805 Low Sep 25 / 50-day EMA

- SUP 2: 1.3727 Low Aug 29 and a bear trigger

- SUP 3: 1.3689 Low Jul 28

- SUP 4: 1.3637 Low Jul 25

Last week’s rally in USDCAD cancels a recent bearish theme and instead strengthens a bullish outlook. The pair has breached a key resistance at 1.3925, the May 20 high and bull trigger. The breach confirms a resumption of the bull cycle that started Jun 16. This paves the way for a climb towards 1.4019, a Fibonacci retracement point. On the downside, first key support lies at 1.3805, the 50-day EMA.