SPAIN DATA: GDP Growth Driven By Strong Supply Side Amid Mixed Annual Revisions

Sep-26 15:21

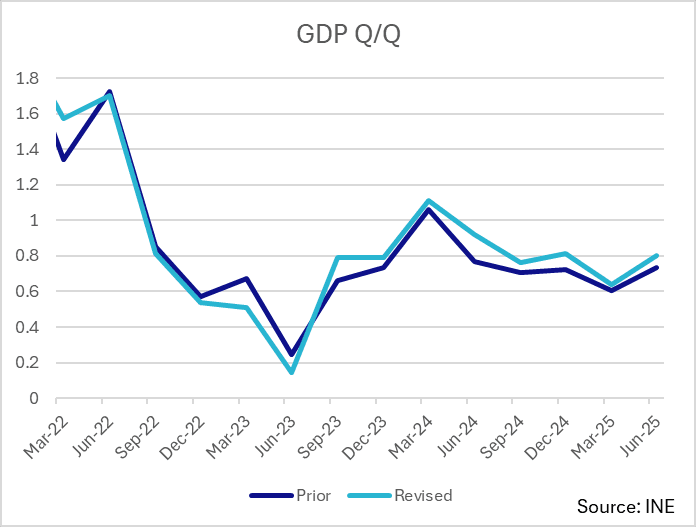

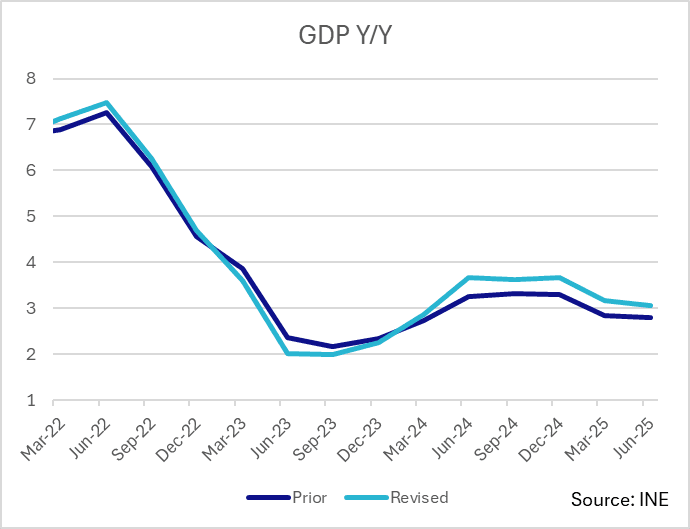

Today's Q2 GDP release came with upward revisions from the flash release (0.8% vs 0.7% flash Q/Q, 3.1% vs 2.8% flash Y/Y). There were also notable upward revisions to Y/Y figures going back to Q124 - attributable to the standard annual revision process to previous years' data.

- The INE implemented the annual revisions (that were released last week) and updated its quarterly path for these, as well as the usual revisions to more current data. As a reminder, last week's release confirmed that 2024 annual GDP growth was revised up 0.3ppt to 3.5%, 2023 revised down 0.2ppt to 2.5% and 2022 revised up 0.2ppt to 6.4%.

- The large upward Y/Y revisions in the Q225 release are driven mainly by base effects from these revisions.

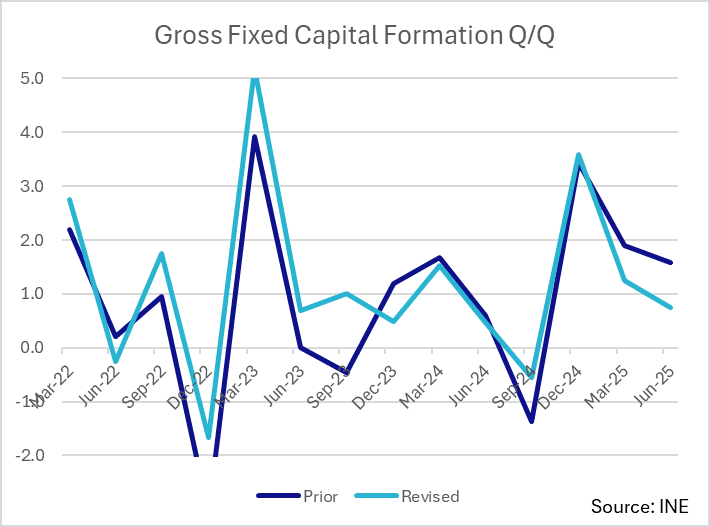

- The 2023 annual series revisions included downward revisions to final consumption expenditure (revised down by 0.2ppt to 2.5%, mainly due to central government expenditure), exports, and imports. There were upward revisions to gross capital formation, while household consumption was unrevised (+1.8% for the year).

- For 2024's annual data, final consumption expenditure was revised down to 3.0% from 3.2% (again, mainly from central government), alongside a huge upward revision to gross capital formation to 4.7% from 1.9%.

- In Q225, contributing to the upward revision from the flash release, construction rose 2.3% Q/Q (vs 1.5% flash) and, within services, finance and insurance activities +2.1% Q/Q (vs 1.6% flash). Interestingly, both construction and services saw upward revisions to their 2024 annual data (most notably in construction, revised up to 4.8% from 2.1%), suggesting an even stronger rate of growth.

- Partly offsetting these positive contributions, investment was revised down from the flash release across the board (gross capital formation +1.8% Q/Q vs +2.1% flash, gross fixed capital formation +0.8% vs +1.6% flash, tangible fixed assets +0.8% Q/Q vs 1.8% flash, dwellings and buildings +0.6% Q/Q vs +1.6% flash, machinery/equipment/weapon systems +1.2% Q/Q vs +2.1% flash).

- Relative to the above, imports and exports were not hugely revised from flash: exports revised up 0.2ppt to 1.3% Q/Q and imports revised down 0.1ppt to 1.6% Q/Q.

- As noted, large revisions to back data were seen in investment. Gross fixed capital formation saw notable upward revisions of around 2-3ppt on a Y/Y basis through Q422 to Q423, though these didn't have a huge impact on more recent figures aside from contributing to the headline GDP's base effect. Though these revisions are less extreme on a Q/Q basis, Q225 still saw a notable downward revision to 0.8% Q/Q from 1.6% flash.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

Aug-27 15:20

- EUR/USD: Aug29 $1.1600(E1.4bln), $1.1625(E4.0bln), $1.1700(E1.1bln), $1.1725(E1.1bln)

- USD/JPY: Aug29 Y145.00($1.7bln), Y146.50($1.1bln)

- EUR/GBP: Aug29 Gbp0.8563-80(E2.1bln)

- AUD/USD: Aug29 $0.6500-15(A$1.4bln)

FED: US TSY 1Y-11M FRN AUCTION: NON-COMP BIDS $19 MLN FROM $28.000 BLN TOTAL

Aug-27 15:15

- US TSY 1Y-11M FRN AUCTION: NON-COMP BIDS $19 MLN FROM $28.000 BLN TOTAL

FED: US TSY 17W AUCTION: NON-COMP BIDS $530 MLN FROM $65.000 BLN TOTAL

Aug-27 15:15

- US TSY 17W AUCTION: NON-COMP BIDS $530 MLN FROM $65.000 BLN TOTAL