EURGBP: GBP Strength Builds, But Could Reach Limit Alongside Z6 Rates

Oct-16 14:15

- Quietly, GBP strength continues to build. Only SEK & NOK have outperformed GBP in spot returns this week and while GBPUSD is close to erasing the early October move lower, it's EURGBP that seems to be more at risk of moving lower.

- The cross off daily lows, but is still trading either side of the 50-dma (a level that has helped anchor prices over the past fortnight). Price has found very little support from the survival of France's cabinet across two confidence votes today, despite the tightening of the French-German yield spread this week.

- A break lower for EURGBP would run counter to the consensus view. The street sees EURGBP rising to 0.88 in the coming three months, with many sell-side analysts seeing the cross as a more effective channel for GBP shorts relative to GBPUSD, which remains overly exposed to uncertain US politics.

- In addition, BoE speakers this week have seemed insensitive to this week's softer-than-expected wages data (Mann: Restriction needed, Bailey: have to balance labour softening against above-target inflation, Greene: concerned disinflation slowing, with only Taylor providing the counter: wage-led inflation won't rekindle upward spiral), suggesting that even as 10bps of BoE easing are priced into year-end, there remains the option for no change to policy rates out to Q1 next year.

- That said, we see the market having more room to reprice a dovish BoE outlook than a dovish ECB outlook, which points to the risk of further downside in the SFIZ6/ERZ6 spread. EURGBP's correlation to 12m forward rates rather than near-term CB expectations is clear - and with more scope for BoE repricing across the course of 2026 relative to the ECB, this could contain protracted downside in spot.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

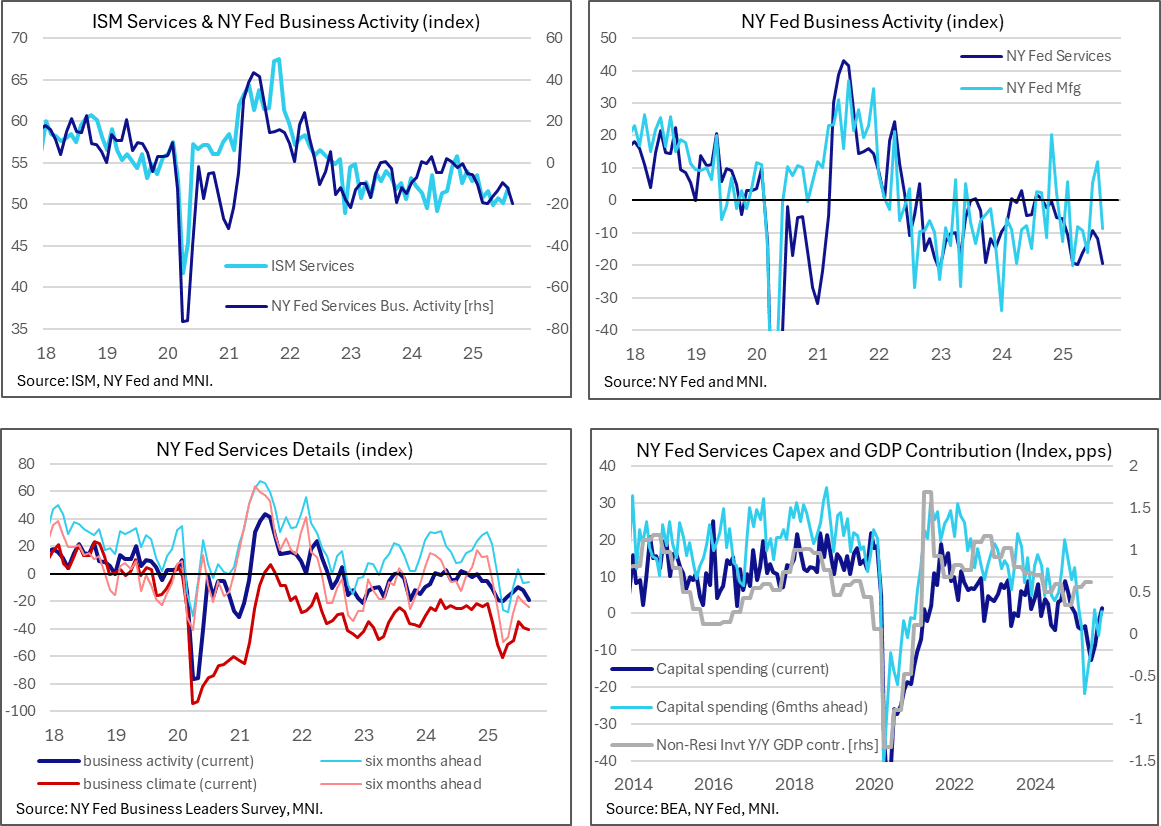

US DATA: NY State Service Firms Echo Manufacturing Weakness In Early September

Sep-16 14:14

Service firms in New York State got off to a similarly weak start to September as their manufacturing counterparts saw yesterday. These are the first September readings for the regional Fed surveys.

- The general activity index surprisingly fell to -19.4 (cons -5.8) in September after -11.7 in Aug to come close to the -19.8 low in April, having last been lower in Jan 2023.

- The six-month ahead measure isn’t as pessimistic though, at -5.8 in Sept after -6.8 in Aug vs a recent low of -28.1 in May.

- In one upside to the report even if not strong, the capital spending index pushed up to 1.4 for its first positive reading since Dec 2024 having recently bottomed at -12.6 in June.

- Other details from the press release: “Employment edged lower, and wage growth remained modest. Supply availability continued to worsen.”

- “Input and selling price increases remained elevated but were little changed from last month. Firms remained pessimistic about the outlook.”

- As with the manufacturing report, the survey was collected through Sep 2-9.

EQUITY TECHS: E-MINI S&P: (Z5) Bullish Extension

Sep-16 14:14

- RES 4: 6750.50 2.000 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6748.50 1.236 proj of the Aug 1 - 15 - 20 price swing

- RES 2: 6712.33 1.764 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6700.00 Round number resistance

- PRICE: 6671.25 @ 15:03 BST Sep 16

- SUP 1: 6559.62 20-day EMA

- SUP 2: 6506.50 Low Sep 5

- SUP 3: 6452.53 50-day EMA

- SUP 4: 6417.25 Low Aug 12

A bull cycle in S&P E-Minis remains intact and the contract has started this week on a bullish note. Fresh cycle highs reinforce current bullish conditions. The move higher confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on the 6700.00 handle next and 6712.33, a Fibonacci projection. On the downside, initial support to watch is 6559.62, the 20-day EMA.

MNI: US JUL BUSINESS INVENTORIES +0.2%; SALES +1.0%

Sep-16 14:00

- MNI: US JUL BUSINESS INVENTORIES +0.2%; SALES +1.0%

- US JUL RETAIL INVENTORIES +0.2%