FOREX: GBP Budget Bounce Could Prove Short-lived as Relief Rally Fades

Nov-27 08:57

- GBPUSD fades from 1.3266 this morning as markets digest yesterday's UK budget, which on balance was roughly in line with expectations. While Chancellor Reeves was able to avoid breaking the Labour manifesto pledges while creating enough fiscal headroom to calm down gilt markets, some questions on further downside risks to the OBR's growth forecasts as well as back-loaded savings remain. This may explain some of the current retrace as yesterday's upside may have been more of a relief from a worst-case scenario and associated unwind of short sterling positioning then genuine optimism.

- The fiscal measures announced should be marginally disinflationary on net, keeping Bank of England easing expectations supported yesterday. Odds for a December cut stand at above 90% with key voter Bailey likely reassured as some inflation upside risks driven by budget uncertainty should have subsided now. Through the April decision, a cumulative 50bp of easing is more or less fully priced.

- Comments from BoE’s Greene (who voted to leave rates unchanged earlier this month) are due at 16:30 London. We don’t expect Greene to indicate support for a cut at the December meeting (the topic of her address is “balancing risks”). BoE's Dhingra is scheduled speak on Monday, and should keep her dovish stance. The UK data calendar meanwhile remains light until monthly GDP on December 12.

- From a technical perspective, the trend theme in GBPUSD is bearish and short-term gains are for now, considered corrective. However, the pair has breached the 20-day EMA and pierced the 50-day EMA, at 1.3261. A clear break of the 50-day average would highlight a stronger bull theme. Moving average studies are in a bear-mode condition, highlighting a dominant downtrend. 1.3010, the Nov 4 / 5 low, is the trigger for a resumption of the bear leg.

- Analysts are not unanimous in the path ahead: MUFG think "While the initial relief rally for the pound is understandable in light of positioning, we are not convinced that the bullish momentum will last long. The lack of any material negative policy surprises in the budget does not provide justification for a sustained reversal higher for the pound" while HSBC say "GBP’s direction will depend on several factors. In the very near-term, it will take cues from the UK Gilts market and BoE rate cut expectations and their response to the Budget over the coming days [...] Overall, we are expecting a further relief rally for GBP in the coming weeks."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUNDS: Block trade

Oct-28 08:55

Bund block trade, suggest buyer:

- RXZ5 2k at 129.71.

GBP: Surge in Volumes Triggers Spell of Weakness in GBP

Oct-28 08:54

Downdraft in GBP in early trade puts GBPUSD through yesterday’s lows of 1.3311 on decent volumes: GBP futures have now printed volumes of 20% above average for this time of day after a sharp uptick in activity at 0839GMT – suggesting a flow-driven move rather than a headline or news trigger spell of weakness.

- The fiscal picture remains the key driver more broadly, particularly given the increasing signs that the Chancellor will have to raise income tax at this month’s budget to fill a widening fiscal hole (as detailed above).

- This has pressured BoE rate pricing across year-end meetings as well as through 2026, however the market is yet to fully factor in 2 x 25bps rate cuts until April.

- The GBPUSD bear trigger remains 1.3249, the October 14 low – which leaves the Fed decision tomorrow evening as the next key news driver.

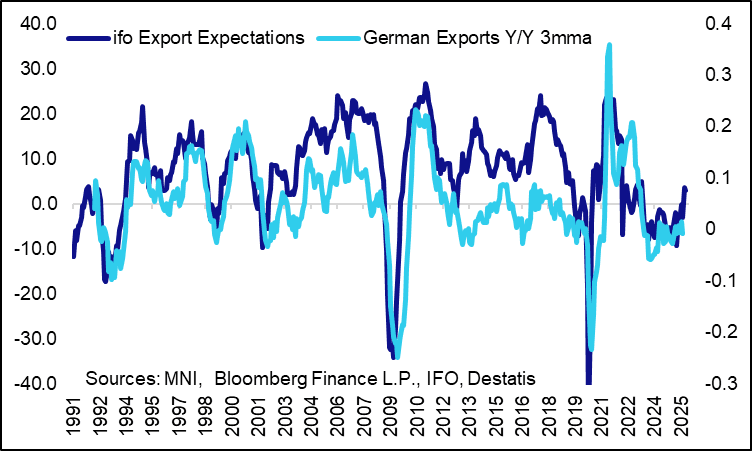

GERMAN DATA: IFO Export Expectations Decline In October

Oct-28 08:47

The German IFO Export Expectations index fell by 0.6 points to 2.8 in October. While the index is off its cycle lows, IFO continues to remain on the pessimistic side regarding German export prospects, commenting "there is no real recovery in sight."

- IFO commentary in September already suggested improvement last month may have been a one-off at least to some extent.

- Across sectors: "The metal industry is feeling the pressure from abroad particularly acutely, with companies expecting exports to decline. The chemical and paper industries anticipate a decline in exports. Although expectations in mechanical engineering and the food industry are better than in the previous month, actual export growth has yet to materialize. In contrast, the automotive industry continues to be very optimistic about international business, with export expectations rising once again. Manufacturers of electrical equipment also expect to increase their exports."

- As a % of nominal GDP on a 12-month rolling basis, the trade surplus extended its current downtrend, at 4.7% as of August, 1.2pp below levels seen around a year ago. That compares with a 2015 high of 8.0% and 2022 low of 2.1%.