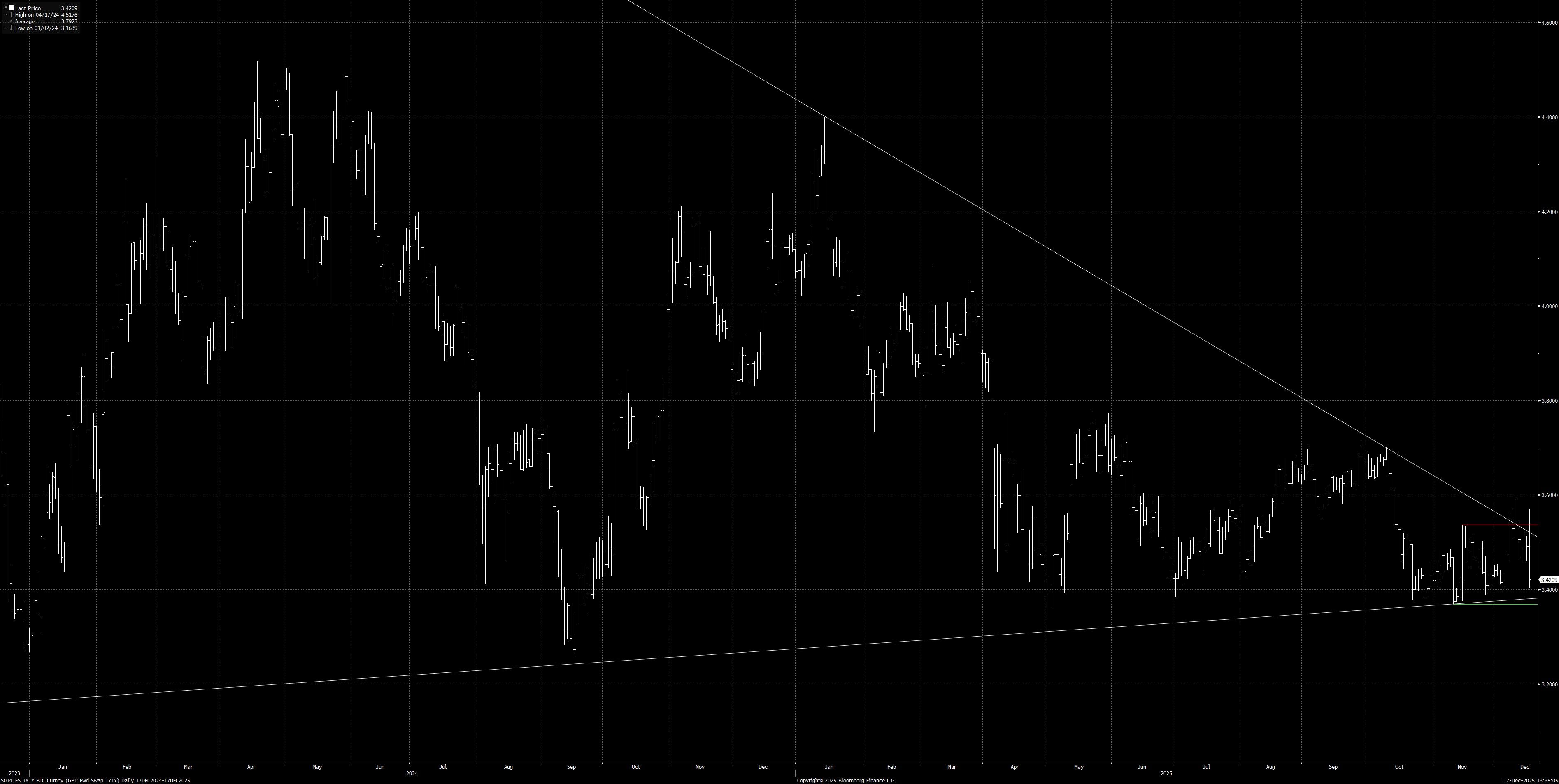

STIR: GBP 1y1y Retraces Back Within Wedge Pattern

Dec-17 13:51

The dovish repricing that followed this morning’s soft UK CPI data has pulled GBP 1y1y swaps further away from the upper boundary of the wedge structure that has formed (see chart below).

- The recent round of hawkish BoE repricing generated a false break above the upper boundary of the wedge early last week.

- Looking forwards, the pricing of a deeper BoE easing cycle is the most likely driver of any extension beyond the base of the wedge.

- Terminal rate pricing of 3.30% has provided a bit of a limitation for terminal rate pricing in recent weeks, but the soft CPI data does increase odds of a potential dovish departure from the market expectation of a 5-4 vote split to deliver a rate cut at tomorrow’s BoE decision.

- This morning’s CPI release may also make the rhetoric that accompanies the decision sound a little more dovish than it otherwise would have been.

Fig. 1: GBP 1y1y (%)

Source: MNI - Market News/Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

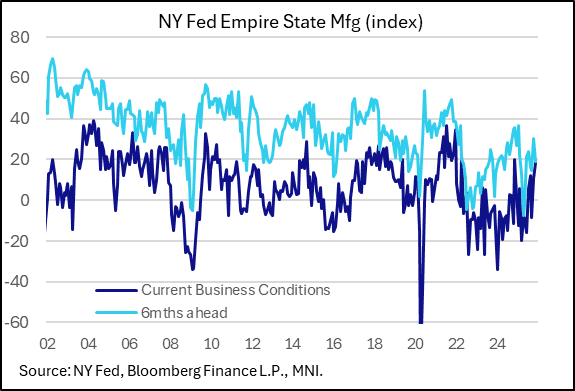

US DATA: Empire Manufacturing Solidifies For 2nd Consecutive Month

Nov-17 13:49

The NY Fed's Empire State Manufacturing Survey impressed in November, with the current General Business Conditions index rising 8 points to a 1-year high 18.7 (well above the 5.8 expected). As such it's the 2nd highest reading since April 2022, with solidly-above-long-term average-readings now for 2 consecutive months, the first time we've seen that since 2021 for this notoriously volatile survey.

- The 6-month outlook pulled back 19.1 from to 30.3 prior, which had been the highest optimism since January.

- Activity indices were strong. New orders jumped to 15.9 from 3.7, setting a 12-month high just 2 months after setting a 17-month low; shipments rose 2 points to 16.8 while inventories turned positive after 3 consecutive negative months.

- The employment gauge edged up to 6.6 from 6.2, for a fresh 4-month high, while the average workweek rose to a multiyear high.

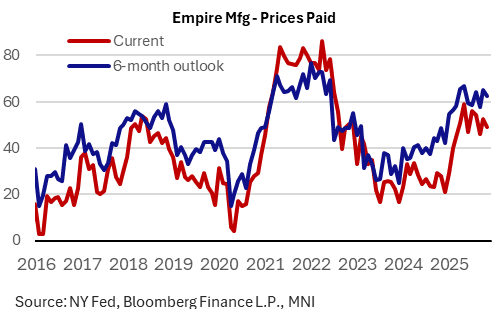

- Inflation remained stubbornly high but didn't show signs of worsening. Current prices paid fell to 49.0 after 52.4, with expected prices paid 6-months ahead down to 62.5 from 65.0. Both are elevated but suggest some moderation after October's sharp M/M rise that suggested inflation was picking up alongside with activity.

- In short, a solid start to the month's regional Fed manufacturing surveys.

GLOBAL POLITICAL RISK: Week Ahead 17-23 November

Nov-17 13:47

Download Full Report Here

Monday 17 November:

- Ukraine-France: French President Emmanuel Macron is hosting his Ukrainian counterpart, Volodymyr Zelenskyy, in Paris. During their meeting at Villacoublay air base near Paris, the two signed a letter of intent for Ukraine to purchase up to 100 Rafale fighter jets, as well as other French-made military equipment, in its efforts to repel Russia’s invasion. The purchases are due to be realised over a period of around 10 years, although questions remain on the ability of Kyiv to fund these purchases, having signed a separate letter of intent to purchase 100-150 Gripen jets from Sweden.

US TSY FUTURES: BLOCK: Dec'25 5Y Buy

Nov-17 13:45

- +5,000 FVZ5 109-04.5, post time offer at 0836:59ET, DV01 $213,500.

- The 5Y contract trades 109-05.25 last (+1.25)