NATGAS: Gas Summary At European Close: TTF Rises

TTF front month has risen to its highest since late-November, unwinding December losses amid a cooler temperature forecast for early-January and above-normal net withdrawals from storage.

- TTF FEB 26 up 2.9% at 28.98€/MWh

- Gas import volumes to Ukraine in 2025 reached 6.47 bcm, nine times higher than in 2024, according to ExPro.

- Temperatures in NW Europe are forecast to fall below normal in the coming days, before rising back towards normal levels in mid-January.

- NW European sendout was estimated at 237.6 mcm/d on Jan. 1, slightly lower than the December average of 249.8 mcm/d.

- Norwegian pipeline supplies to Europe are at 345.3 mcm/d, completing a recovery from a dip to 305.9 mcm/d on Dec. 30 back towards levels seen through most of December. Gassco shows limited unplanned capacity reductions through January.

- European gas storage was 62.24% full on Dec. 31, according to GIE data, compared to the previous five-year seasonal average of 73.98%, with net withdrawals above normal.

- Asian spot LNG prices started the year steady, as muted regional demand and ample supply kept the market flat following a 34% slump in 2025, according to Reuters.

- Global LNG freight rates continue to fall at the start of the new year, according to Spark Commodities.

- The Shell-led 14 mtpa LNG Canada plant in Kitimat, British Columbia, resumed LNG exports following a shutdown earlier this month, with a cargo departing from the terminal late on Dec. 30, according to vessel tracking from Kpler

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

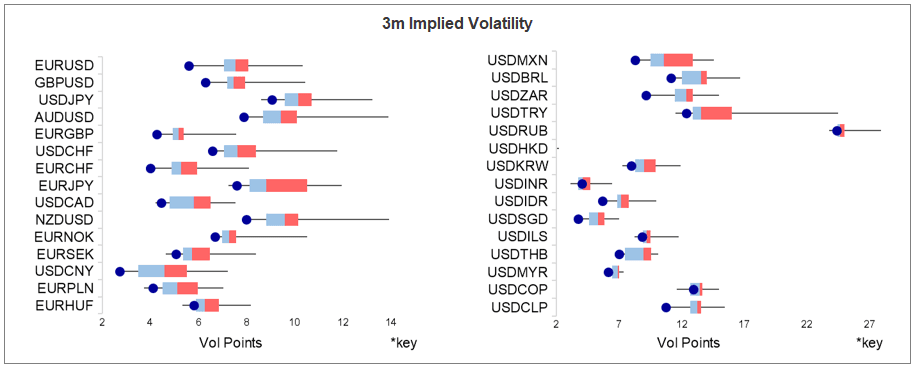

FOREX: Spiralling Vols Leave Year-End Options Cost Among Lowest of the Century

FX vol markets remain heavily pressured, particularly in the front-end of the curve and even when excluding December seasonality. Low outright vol (and vol-of-vol) coincides with solid pricing for the various rate decisions due between now and year-end (~90% for Fed & BoE cut, 80% for BoJ hike, ~100% for ECB, RBA & SNB hold), leaving minimal odds for event-driven vol.

- As a result, 3m implied vols across both G10 and EM FX heads through early December at comfortably the lowest levels of the past 12 months - as shown in this histogram:

- More notably, however, even on a 25-year look back, vols look historically extremely cheap: GBP, EUR, NZD, CAD, SEK vols are at their second lowest level for December 3rd in 25 years, NOK the third lowest and AUD the fifth lowest.

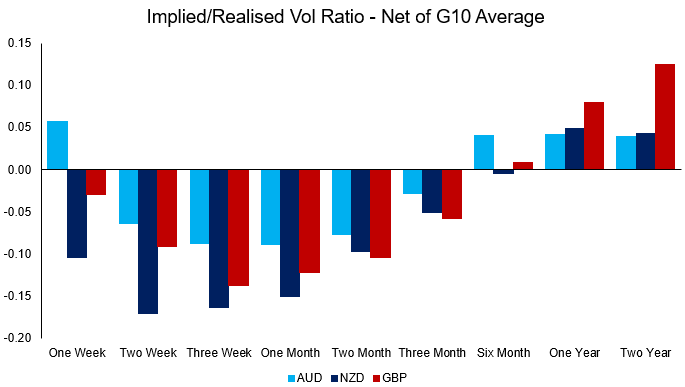

- Hotspots of vol are declining as we approach year-end (we identified JPY as one of the last currencies in focus and the implied/realised vol ratio across currencies suggests further subdued gamma demand in the likes of NZD, GBP and AUD (see bar chart below).

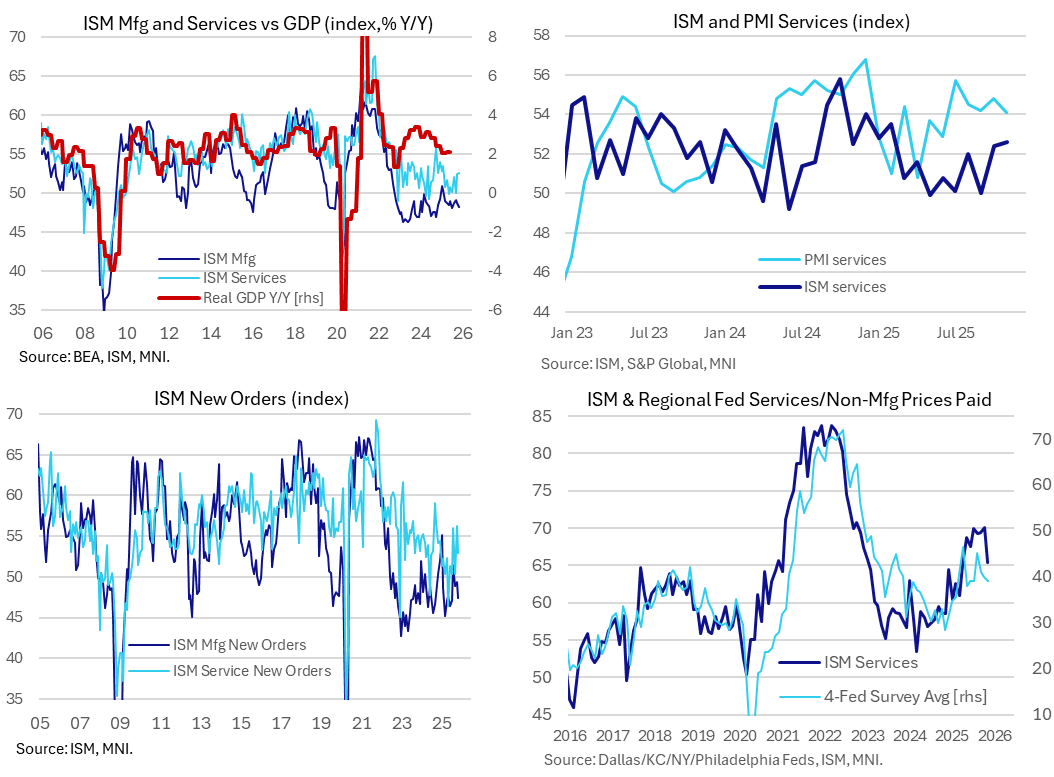

US DATA: ISM Services Beat Countered By Declines In Some Key Components

The ISM services report was stronger than expected in November although saw some conflicting developments in the main components, with new orders and prices paid slipping but employment increasing to a six-month high (albeit still in contractionary territory).

- The ISM services index was stronger than expected in November as it inched higher to 52.6 (cons 52.0) after 52.4 in October, marking its highest since February.

- The S&P Global US services PMI continues to offer a more optimistic assessment of current activity despite being revised down in its final November release to 54.1. That said, the 1.5pt outperformance is the smallest gap since the ISM survey briefly overshot it in April.

- Twelve industries reported growth last month, led by retail trade, entertainment and recreation, and accommodation and food services. Five contracted, including construction.

- New orders fell 3.3pts to 52.9 after a twelve-month high of 56.2 in October, but it’s hard to take a signal from here after some particularly volatile months where it’s swung between 50 to 56 handles in each month since July.

- Orders are a clear area when the PMI report is more optimistic, noting "Activity was supported by the firmest rise in new work of 2025 so far, whilst confidence in the outlook strengthened following the end of the government shutdown and expectations of improved economic growth in the year ahead."

- Prices paid saw a more notable 4.6pt decline to 65.4 after the 70.0 in October poked above 69.9 in July for the highest since Oct 2022. It’s the lowest since April but is still elevated historically, for instance following 58.7 in 2024 and 57.5 in 2019 for longer-term context).

- As noted beforehand, regional Fed service surveys pointed to downside risk for prices paid, as has been the case through 2H25, but the services PMI saw a sharp uptick in input cost inflation, even after a downward revision in the final S&P Global release just before the ISM release.

- The employment index meanwhile logged a fourth consecutive monthly increase to 48.9 (+0.7pts), still in contractionary territory but a six-month high.

GILT AUCTION PREVIEW: On offer next week

The DMO has announced it will be looking to sell GBP4.5bln of the 4.75% Oct-35 Gilt (ISIN: GB00BTXS1K06) at its auction next Wednesday, December 10.