LNG: Gas Continues To Be Highly Sensitive To Weather Outlook

Wintery weather drove natural gas higher on Wednesday. Europe reached EUR 29.175 but finished at EUR...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

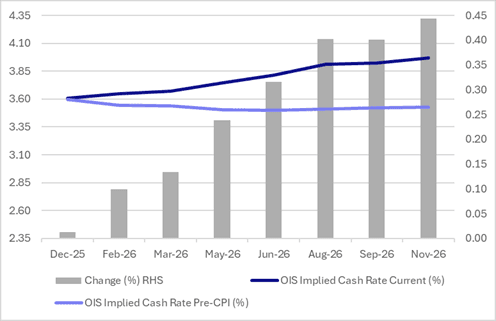

STIR: 39bps Of Tightening Now Priced For Dec 2026 Ahead Of RBA Decision

RBA-dated OIS pricing is modestly firmer today for meetings beyond May 2026, ahead of the RBA’s policy decision.

- The RBA is unanimously expected to leave the Cash Rate at 3.6% when it announces its decision at 1430 AEDT (see MNI RBA Preview), followed by Governor Bullock’s press conference at 1530 AEDT.

- The market continues to price tightening across all meetings, with the implied probability of a 25bp hike rising from 3% today to 123% by August and 157% by December 2026.

- Given this pricing backdrop, there is scope for a modest relief softening if the Board signals that it needs more information before adjusting its rhetoric—particularly as the October CPI was the first release under the new monthly methodology.

- Key upcoming data include Q4 CPI on 28 January, November consumption figures, and the November and December labour-market reports.

- Following today’s moves, OIS pricing is now 10–45bps firmer across the curve beyond December 2025 relative to levels before the Monthly CPI release on 26 November, led by December 2026.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI Monthly

Source: Bloomberg Finance LP / MNI

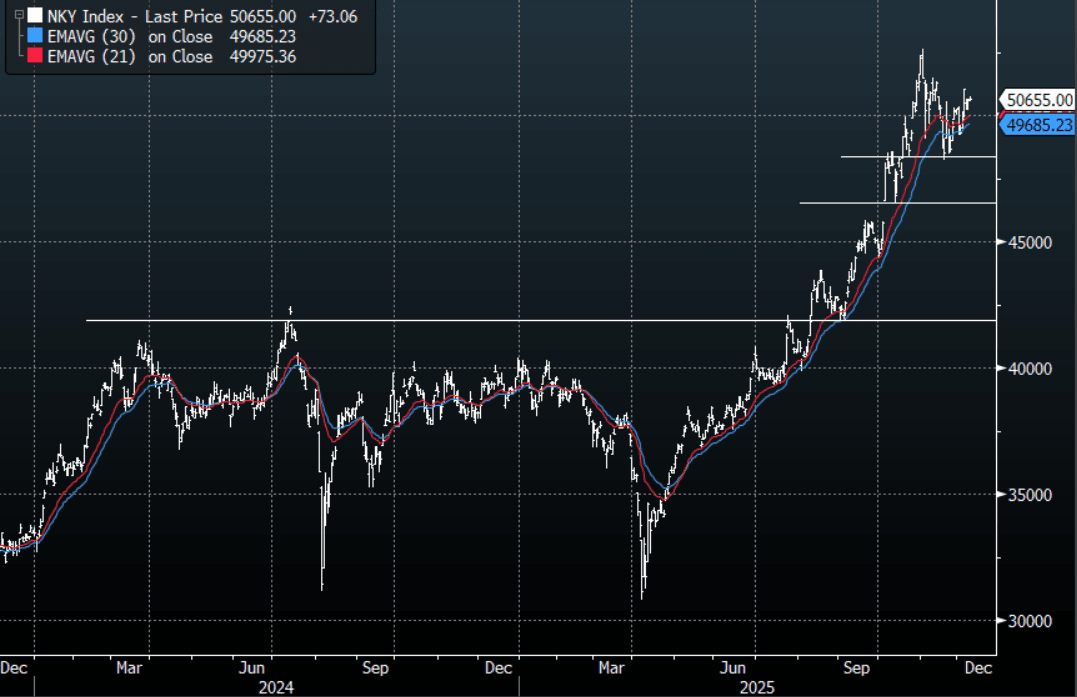

JAPAN: Nikkei(NHH6)-Bounces With Risk, Watch 50800-51000 Area To Cap Initially

The Nikkei(NHH6) contract overnight range was 50220 - 50705, Asia is currently trading 50750, +0.75%. The (NHH6) contract has opened much stronger this morning as risk takes a leg higher on news Trump is allowing Nvidia to sell H200 chips to China. Is this news enough to turn around a market that potentially looked to be retracing with worries about higher global bond yields.The Nikkei 225 technically remains in an uptrend while the support toward 48000 holds, albeit a very steep one. In the Asian session price will watch to see if this strong open is able to break above the 50800-51000 area, above here and the focus will turn toward the 51500-51700 resistance. Failure to push above here and we could see a pullback, first support is back toward the 49600-900 area.

- MNI POLICY: BOJ Unshaken By JGB Volatility. Bank of Japan officials see no need to intervene in the JGB market, even though they expect volatility to persist, and attribute the recent rise in yields to market assessments of the economic and inflation outlook as well as future policy moves, MNI understands.

- The Nikkei 225 Index Average True Range(ATR) for the last 10 Trading days: 691 Points

Fig 1: Nikkei 225 Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

RBA: Tone To Be Scrutinised At Today’s Decision, May Wait For Q4 CPI Though

The RBA is unanimously expected to leave rates at 3.6% when it announces its decision today at 1430 AEDT (see MNI RBA Preview). It will be followed by Governor Bullock’s press conference at 1530 AEDT. With the outcome widely forecast, the statement and her tone will be scrutinised for any changes in stance and balanced view around the outlook. The Board may want to see more information before it makes any major changes, especially as the October CPI was the first read on the new monthly series. Q4 CPI on 28 January, November consumption and November & December jobs will important releases.

- NAB expects the RBA to sound more hawkish given that inflation rose further above the top of the band in October and “signs of momentum in private demand”. It is forecasting no rate changes in H1 2026 but that could change depending on inflation, activity and labour data.

- ANZ notes that a hike in December would surprise them less than a cut. It also expects a hawkish shift with the RBA noting “uncomfortably high inflation pressures” and as a result has removed its H1 2026 cut and is forecasting unchanged rates through 2026. It can see scenarios for both easing and tightening though.

- CBA observes that since the November RBA decision there has been further evidence of tighter capacity and upside inflation risks and so it expects the Board to “acknowledge the increased risk of higher inflation and the shift in the balance of risks around monetary policy”. CBA doesn’t believe that there will be “major changes” to the RBA’s tone this month but it will maintain its flexibility while waiting for Q4 CPI.

- Westpac is projecting that softer supply capacity will drive inflation lower in 2026 and as a result create “scope for rate cuts in May and August next year”.