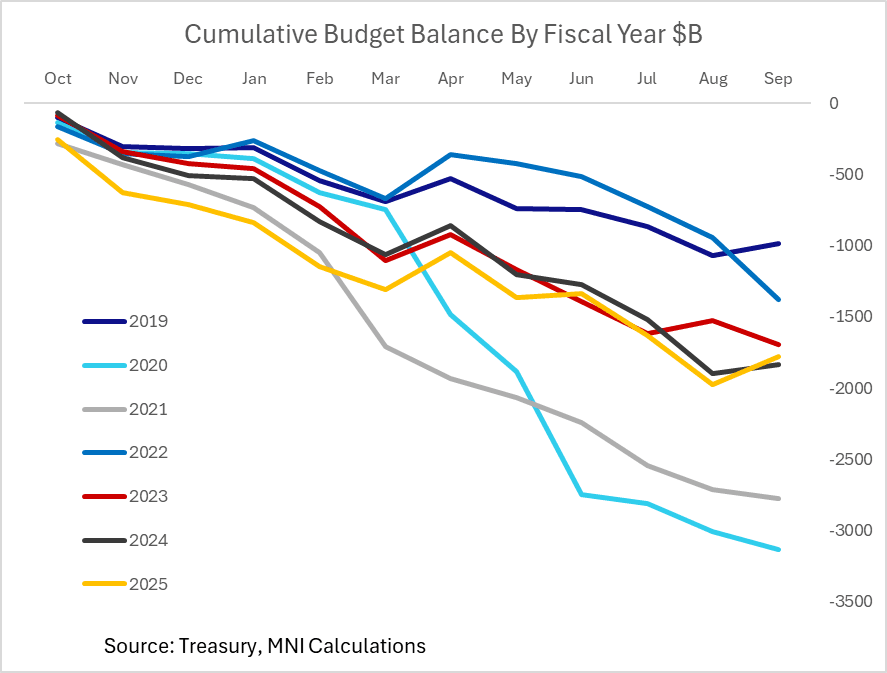

US FISCAL: FY2025 Deficit Pared To 5.9% Of GDP, Tariffs Offset Net Interest

Treasury announced a $1.775T deficit for the 2024 fiscal year, down from $1.817T prior.

- The September surplus of $198B was substantially above the Congressional Budget Office's $160B estimate, with the report noting that "Outlays for military active duty and retirement, veterans benefits, Supplemental Security Income, and Medicare payments to health maintenance organizations and prescription drug plans accelerated into August, because September 1, 2025, the normal payment date, fell on a non-business day."

- Total outlays for the year totaled $7.01T ($6.73T prior), with receipts rising to $5.23T ($4.92T prior).

- Some key line items: customs duties came in at $195B, up from $77B the year prior, helping offset a rise in net interest to $970B from $881B.

- In total, the deficit to GDP dropped to 5.9%, vs 6.3% in the prior fiscal year, in line with MNI's estimate based on the raw figures provided by the CBO earlier this month. That's progress but still well above the 4.6% in 2019 pre-pandemic, and the 3% target Tsy Sec Bessent is ultimately aiming for.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Traders Through Resistance

- RES 4: 1.3789 High Jul 1 and key resistance

- RES 3: 1.3753 High Jul 2

- RES 2: 1.3681 High Jul 4

- RES 1: 1.3672 High Sep 16

- PRICE: 1.3657 @ 20:24 BST Sep 16

- SUP 1: 1.3510 20-day EMA

- SUP 2: 1.3480/3430 50-day EMA / Low Sep 5

- SUP 3: 1.1.3333 Low Sep 3

- SUP 4: 1.3142 Low Aug 1 and a key support

A bullish theme in GBPUSD remains intact and price is trading higher this week. The pair has traded through resistance at 1.3595, the Aug 14 high and a bull trigger. The break strengthens bullish conditions and opens 1.3681 next, the Jul 4 high. Initial firm support to watch is 1.3480, the 50-day EMA. A clear breach of the EMA would highlight a potential reversal and signal scope for a deeper retracement.

OPTIONS: US Options Roundup: Sep 16 2025

Tuesday's US rates/bond options flow included:

- SFRV5 95.75/95.87/96.00c fly, traded flat in 5k (on block)

- SFRV5 95.87c, traded for 47.5 in 2k

- SFRX5 96.62/96.75cs, bought for 1 in 10k total

- SFRZ5 96.00 puts 23K given at 1.0 over several clips

- SFRZ5 96.37/96.50/96.56/96.68c condor, traded 2.25 in 2.5k

- SFRZ5 96.50/96.37/96.25p ladder, traded 2.25 in 2.5k

- 0QH6 97.00/96.75ps vs 3QH6 96.75/96.50ps, traded flat in 1.5k

- 0QH6 96.87/96.75/96.37/96.25p condor, bought for 3.5 in 1.5k

- 0QZ5 97.00/98.00 call spread sold at 21 in 7.25k

FED: September Dot Plot: Longer-Run Seen Stable, Analysts Split On 2025 (2/2)

- 2026: The end-2026 dot is likely to fall a quarter-point to 3.4% from 3.6% prior. June’s projections had 4 members at the median, with 6 above and 9 below, so it would take just one of those at 3.6% to shift lower at this meeting to bring the median down a notch. That said, vs 10 seeing rates remaining above 3.50% back in June, we expect their number will shift down only slightly to 7-8. There is something of a lower bound here set by the longer-run dot of 3.0%, with 3.1% representing the median outer-year view, and we’re not sure there will be much appetite for most of the Committee to project a move any lower than 3.4%.

- 2027-28: As noted, the outer years are likely to see a settling-in at 3.1%, just above the longer-run rate. We get 2028 projections for the first time at this meeting.

- Longer-Run: The median is finely poised with 3 members at 3.00%, 8 above and 8 below, meaning there’s always a risk that the median will shift up from 3.00% (it has been drifting higher since 2022). However, this is not our base case for this meeting.

- The next increase would bring the longer-run rate back above 3.00% for the first time since March 2016, and would be up from the trough of 2.40% in 2022.

Analyst consensus: Analysts see a slightly lower “dot” profile in the Fed funds medians vs the last edition in June. For 2025 the median is narrowly in favor of a 3.9% (unchanged) end-year median, though many see 3.6%. For 2026 most see 3.4% (down from 3.6% in June), moving to 3.1% by end 2027 (down from 3.4% in June). No analyst sees the longer-run rate changing (3.0%).

- Sorted in order of highest to lowest 2025 end-year "Dot":