EUR: FX Exchange traded Option

FX Exchange traded Weekly Wednesday Option:

- EURUSD (7th Jan) 1.2150c, bought for 0.00035 and 0.00040 in 1k.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

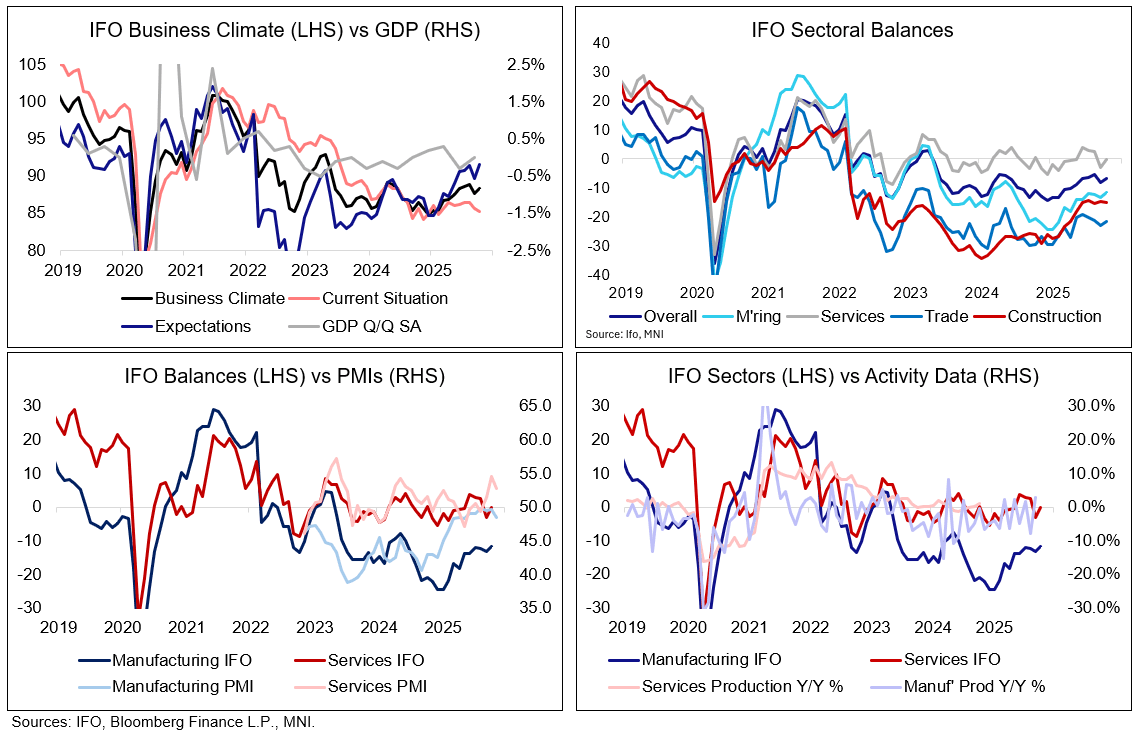

GERMAN DATA: IFO To Show If Current Conditions Start Catching Up To Expectations

The German IFO business climate index is scheduled for release at 09:00 GMT / 10:00 CET, with consensus for a broadly unchanged reading at 88.5 (88.4 prior). We continue to watch when current conditions (85.5 cons vs 85.3 prior) will start to catch up to expectations (91.6 cons vs 91.6 prior) which have improved in recent months but not filtered through yet. A further deterioration in current conditions may weigh on Q4 GDP in the country (see top left chart).

- "Due to weakness in the Sentix survey, ZEW and German PMIs there are probably downside risks to consensus" RBC think.

- As a reminder, the German composite PMI printed below consensus on Friday at 52.1 (vs 53.5 cons, 53.9 prior), with both services and manufacturing lower-than-expected. We don't read into the services miss too much though - it's still the third consecutive month of expansion and the bar set by consensus was probably too high after a very strong October. Manufacturing trends meanwhile remain sluggish, with poor export order performance weighing.

- Final Q3 German GDP is scheduled for tomorrow, which will provide an expenditure split to the 0.0% Q/Q flash print after Destatis commented "gross fixed capital formation in machinery and equipment developed positively [...] exports, by contrast, were down compared with the previous quarter."

GILTS: Friday's High In Futures Holds On First Test As Budget Week Gets Underway

Gilts firm at the open, mimicking moves in core global FI peers.

- Friday’s high in futures (92.43) holds on the first test before a fade back to 92.35.

- A break higher would expose the November 18 high (92.60), which protects the 20-day EMA (92.70).

- Meanwhile, support comes in at 91.51.

- Bears remain in technical control at this stage

- Yields ~1.5bp lower across the curve.

- Recent headlines reaffirm the idea that the OBR is set to downgrade growth across its forecast horizon.

- Elsewhere, we have highlighted the likely reduction in headline and services CPI surrounding the reported freeze of rail fares (-0.02ppt & 0.04-0.05ppt respectively in March ’26).

- Wider weekend reporting generally reaffirmed known focal areas and ideas as we move towards Wednesday’s Budget.

- Some buy-side names have outlined what they want to see in the Budget via the FT: https://www.ft.com/content/e01f51d9-11d5-45d8-a865-62446eeda545

- Note that the BoE will come to market with GBP750mln of medium-term paper from its APF this afternoon.

MONTH-END EXTENSIONS: Bond Extensions

Given the shorter Week can't rule out some small front running. Overall though, Extensions are below average and the impact should be limited.

Bloomberg Bonds:

- US Tsys: +0.11yr (average).

- EU Govies: +0.05yr (small).

- UK Govies: -0.03yr (non event).

MS Bonds:

- US Tsys: +0.08yr (average).

- EU Govies: +0.05yr (small).

- UK Govies: -0.03yr (non event).