JGBS: Futures Stronger Overnight With US Tsys As Risk-Off Grips Markets

In post-Tokyo trade, JGB futures closed sharply higher, +45 compared to settlement levels, after US ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.870 @ 15:51 GMT Jan 13

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again on Thursday last week, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

AUSSIE BONDS: Slightly Mixed, Light Data Day, Oct-36 Supply

ACGBs (YM +0.5 & XM -1.5) are slightly mixed after cash US tsys finished little changed, well off the morning's knee-jerk post-CPI data bests. Markets continue to digest multiple anomalies in the data set stemming from a reversal of November holiday sale discounting for goods products, along with sampling issues from the use of bimonthly metro area surveys (with no October data for comparison due to no survey that month).

- Today’s US data includes PPI, Retail Sales and Existing Home Sales data.

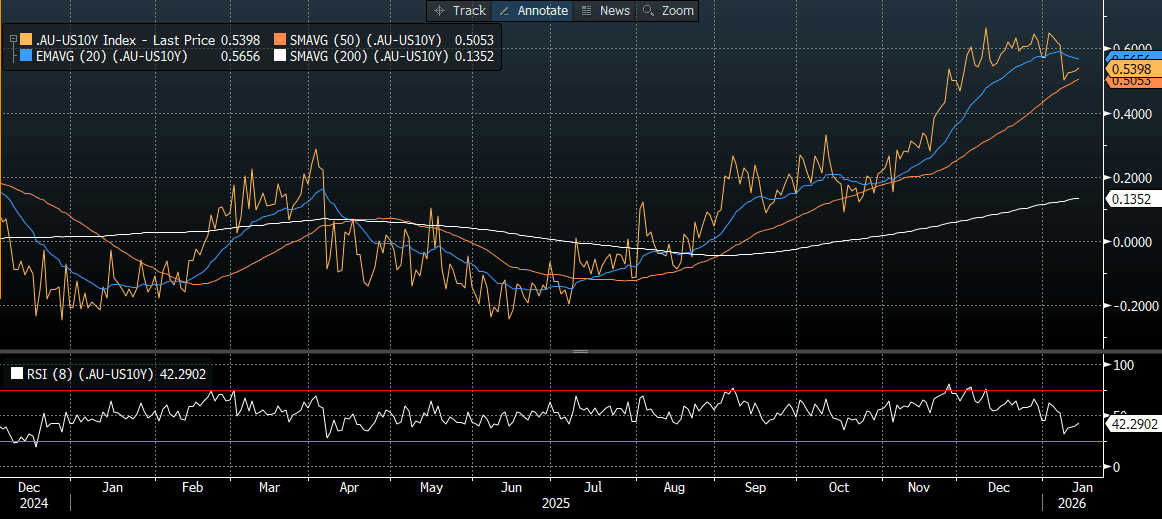

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +54bps. A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month (1Y3M) swap spread over the past two years suggests the current spread sits close to its regression-implied fair value.

- The bills strip is slightly stronger, with pricing +1 to +2 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 31% for February to 91% by June and 136% by December 2026.

- Today, the local calendar will see Job Vacancies.

- The AOFM plans to sell A$1bn 4.25% 2036 bond today and A$700mn 3.25% 2029 bond on Friday.

Bloomberg Finance LP

NEW ZEALAND: Filled Jobs Best M/M Rise Since Late 2023, But Still Down Y/Y

New Zealand filled jobs rose 0.3%m/m in Nov last year after a revised -0.1% outcome for Oct (originally reported as flat). Nov's rise was the best m/m gain since Oct 2023. This signifies some progress in better jobs growth momentum, although it follows a long period of softer momentum through much of 2024 and 2025. In y/y terns, jobs filled were still down 0.4%. The data, along with a rise in building permits, should add to the sense of improved economic momentum for NZ in 2026, suggesting an early wait and see approach for the RBNZ. Note we get Q4 2025 inflation next week on Friday.

- By industry, Stats NZ noted the following outcomes in y/y terms - "construction – down 3.6 percent, health care and social assistance – up 1.8 percent, professional, scientific, and technical services – down 2.2 percent, manufacturing – down 1.6 percent, public administration and safety – up 2.1 percent."

- Hence a lot of the job creation is in the services side rather than goods producing/manufacturing.

- Earlier, Westpac noted: "Employment confidence rose by 3.9 points to 93.8 in the December quarter. Jobs are still seen as hard to come by, but current readings are consistent with a peak in the unemployment rate."

- Other data showed a 2.8%m/m in building permits for Nov. This comes after a revised 0.7%m/m fall for Oct. We up 7% in y/y terms, but in levels terms we are still comfortably under 2022 highs.