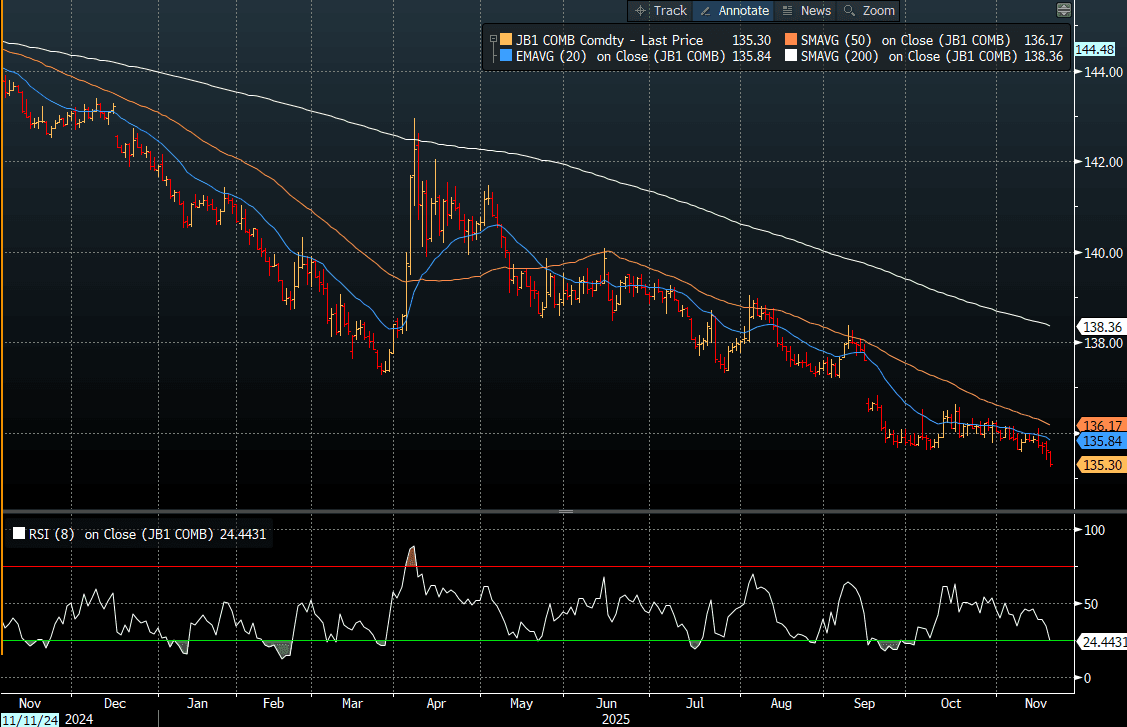

JGBS: Futures Pushed To fresh Cycle Low Overnight

In post-Tokyo trade, JGB futures closed sharply weaker, -31 compared to settlement levels, after cash US tsys finished 2-3bps cheaper following the release of the October Meeting FOMC Minutes.

- JGB 10-year futures (JB1) continuous contract pushed to a fresh cycle low overnight. (see chart)

- Wall Street rebounded ahead of Nvidia's earnings but finished below its early highs. After the close, U.S. equity futures moved higher following Nvidia's results, which topped expectations.

- The improvement in risk appetite weighed on US tsys, as did expectations that the FOMC will hold off on a December rate cut.

- While opinions "differed strongly", the minutes suggest that it may only be a minority of the Committee that is pushing for a follow-up cut.

- MNI POLICY: BOJ To Phase Out Underlying CPI Gradually. The Bank of Japan has begun a gradual phase-out its in-house underlying inflation gauge as the primary guide for policy decisions and will instead rely on headline and core CPI to steer monetary policy, in a move aimed at improving communication with markets, MNI understands.

- Today, the local calendar will feature the Weekly International Investment Flow and Tokyo Condominiums for Sale data, alongside a speech in Niigata by BOJ Board Member Koeda.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: AUCTION PREVIEW: ACGB Jun-54 Supply Due

The Australian Office of Financial Management (AOFM) will today sell A$300mn of the 4.75% 21 June 2054 Treasury Bond. The line was last sold on 23 September 2025 for A$300mn. The sale drew an average yield of 5.0141%, at a high yield of 5.0175% and was covered 3.3500x. There were 54 bidders, 16 of which were successful and 10 were allocated in full. The amount allotted at the highest yield as a percentage of the bid at that yield was 91.7%.

- This week's ACGB supply is near the top of the recent weekly issuance range of $1500-2200mn, with A$900mn of the 2.75% 21 June 2035 bond on Wednesday and A$800mn of the 2.75% 21 November 2029 bond on Friday.

- During the first half of 2025-26, the AOFM plans to: issue a new October 2036 Treasury Bond (by syndication and subject to market conditions); conduct 2 Treasury Bond tenders most weeks; hold 1-2 Treasury Indexed Bond tenders each month.

- Issuance of Treasury Bonds (including Green Treasury Bonds) in 2025-26 is expected to be around $150 billion. Issuance of Treasury Indexed Bonds in 2025-26 is expected to be between $2 billion and $3 billion.

- Results are due at 0200 BST / 1100 AEST.

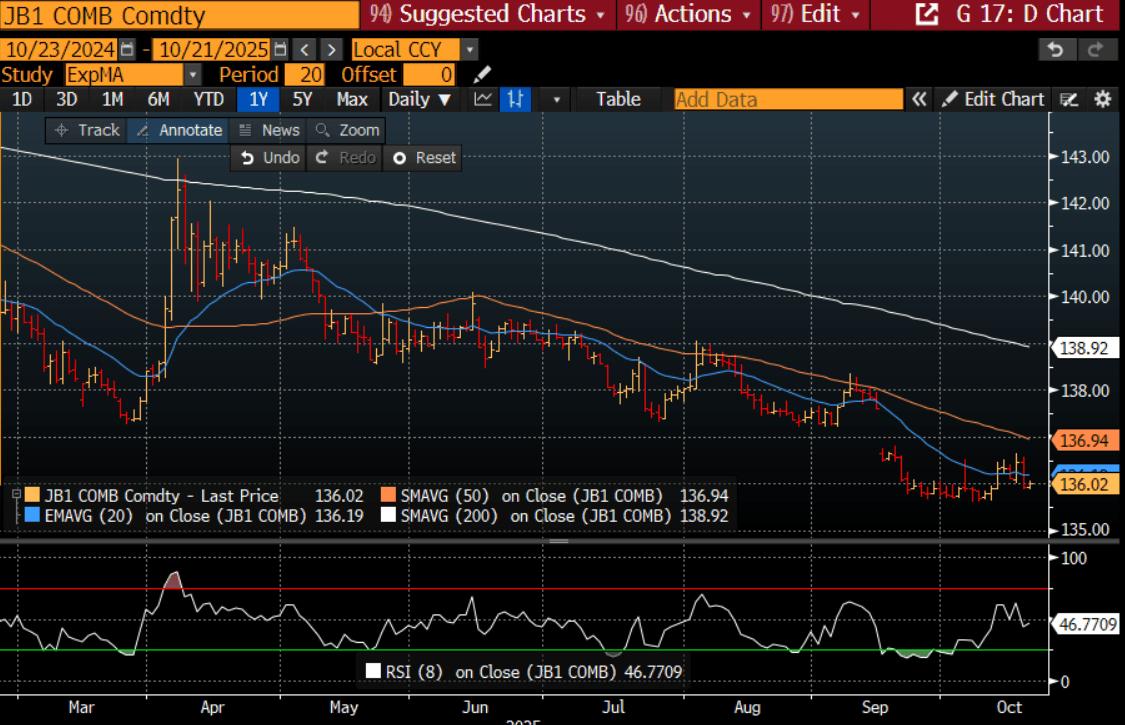

JGBS: Futures Higher Overnight But Trend Is Down

In post-Tokyo trade, JGB futures closed higher, +9 compared to settlement levels, after US tsys finished with a modest bull-flattener as the US Gov entered shutdown day 19, no data & the Federal Reserve is in policy blackout through October 30.

- Looking ahead, UK fiscal data will be published ahead of Canada CPI on Tuesday, while markets will remain focused on Friday’s US inflation data. An early look at analyst unrounded core CPI estimates for Friday’s delayed September release sees a median estimate of 0.30% M/M, with a reasonably wide range of 0.25-0.36% M/M.

- MNI Tech: Key short-term resistance for JB1 has been defined at 137.30, the Sep 8 high. The latest sell-off, however, resulted in a break of support at 136.19, the Sep 4 low and a bear trigger. Clearance of this level confirms a resumption of the downtrend and opens 135.39 next, a Fibonacci projection.

- Focus will be on Takaichi's policy agenda, particularly cost-of-living relief and what that means for the fiscal outlook. Takaichi's and her advisors' viewpoints on BoJ hikes will be watched, although market pricing doesn't have a full 25bps hike priced in until March next year.

- Today, the local calendar will see Tokyo Condominiums for Sale and Machine Tool Orders data alongside 10-year CT supply.

Bloomberg Finance LP

JGB TECHS: (Z5) Bounce Fades

- RES 3: 140.08 High Jun 13

- RES 2: 139.05 High Aug 4

- RES 1: 137.30 - High Sep 8 and key short-term resistance

- PRICE: 136.04 @ 17:08 BST Oct 20

- SUP 1: 135.61 - Low Oct 08

- SUP 2: 135.39 - 1.618 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

- SUP 3: 134.69 - 2.000 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

Prices surged last week, in sympathy with global bond markets, helping the price rally toward last week’s high. This rally proved short-lived, however, as domestic fiscal concerns continue to weigh on prices. This affirms the firm downtrend that’s dominated prices since mid-September, and prices will need to challenge resistance before signaling any broader reversal. Key short-term resistance has been defined at 137.30, the Sep 8 high. The latest sell-off, however, resulted in a break of support at 136.19, the Sep 4 low and a bear trigger. Clearance of this level confirms a resumption of the downtrend and opens 135.39 next, a Fibonacci projection.