JGBS: Futures Higher Overnight With US Tsys Ahead Of Earnings & HH Spend Data

In post-Tokyo trade, JGB futures closed stronger, +13 compared to settlement levels, after US tsys f...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NEW ZEALAND: Ongoing Labour Market Recovery Modest, Wages Contained

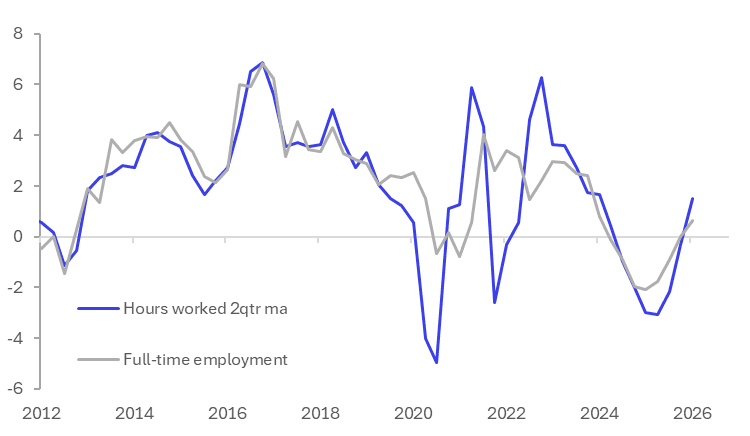

The labour market continued its modest recovery in Q1. The unemployment rate was lower, there was job growth in both full-time (FT) and part-time (PT) sectors and hours worked were higher. While the unemployment rate dip to 5.3% was in line with the RBNZ’s February forecast, employment growth was softer. Wage growth also remained contained, thus labour market conditions argue for the RBNZ to remain on hold but the onset of the Iran War has complicated decision making. The next announcement is 27 May.

- Employment rose 0.2% q/q to be up only 0.4% y/y after 0.5% q/q & 0.2% y/y. The RBNZ projected in February an increase of 0.4% & 0.7%. The majority of job growth was in part-time positions suggesting employer caution. PT rose 0.5% q/q with FT up 0.1% q/q.

NZ employment y/y%

Source: MNI - Market News/LSEG

- The unemployment rate eased 0.1pp to 5.3% as the participation rate fell 0.1pp to 70.4%. Also the number of unemployed was down 1.2% q/q, the largest quarterly decline since Q4 2021. However, youth not in employment or education/training rose 1.1pp to 14.4% in Q1, which as a lead indicator signals ongoing labour market weakness.

- Hours worked increased 0.8% q/q to be up 2.2% y/y. The underutilization rate remains high though at 12.9%.

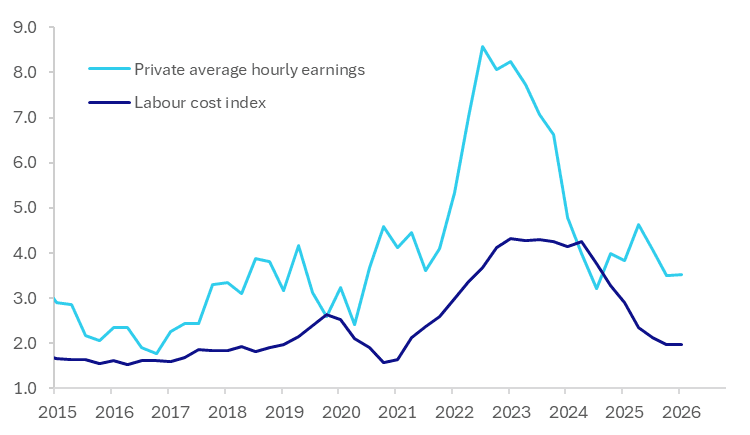

- Private wages including overtime rose 0.4% q/q, as expected, but excluding overtime were stronger at 0.5% q/q but only 2.0% y/y unchanged from Q4. Wage growth is currently not a problem for the inflation outlook and with labour demand still moderate, high pay outcomes are unlikely.

- Private average hourly earnings were also moderate up 0.2% q/q and 3.6% y/y. Total labour costs rose 0.5% q/q & 2.0% y/y.

NZ wages y/y%

Source: MNI - Market News/LSEG

CROSS ASSET: Risk Sentiment Aided Post Trump Post On Pausing Project Freedom

"*TRUMP: PAUSED PROJECT FREEDOM ON REQUEST OF PAKISTAN

*TRUMP POSTS ABOUT PROJECT FREEDOM ON TRUTH SOCIAL

*TRUMP:GREAT PROGRESS HAS BEEN MADE ON FINAL AGREEMENT WITH IRAN" - BBG

"TRUMP: IRAN, U.S. HAVE MUTUALLY AGREED THAT, WHILE BLOCKADE WILL REMAIN IN FULL FORCE AND EFFECT, PROJECT FREEDOM ( MOVEMENT OF SHIPS THROUGH STRAIT OF HORMUZ) WILL BE PAUSED FOR A SHORT PERIOD OF TIME TO SEE WHETHER OR NOT AGREEMENT CAN BE FINALIZED AND - [RTRS]

Risk sentiment getting a boost as Trump posts on Truth Social re pausing of the Project Freedom, while noting progress in getting an agreement in place with Iran.

US equity futures higher, oil futures lower. USD softer. Eminis are up close to 0.40%, to 7315, WTI is back near $100/bbl, the USD BBDXY is down a little over 0.10%.

BONDS: NZGBS: Little Changed, Q1 Employment Rate Mixed

NZGBs are little changed after the release of the Q1 Employment Report.

- The Q1 unemployment rate eased 0.1pp to 5.3%, better than expected and in line with the RBNZ’s February forecast. However, employment growth was weaker up 0.2% q/q and 0.4% y/y. Private wages with overtime rose 0.4% q/q, as expected, but excluding overtime were stronger at 0.5% q/q.

- Overnight, US tsys finished modestly richer after ISM Services prices paid comes out lower than expected, as did New Orders. Meanwhile, March JOLTS job openings vs. Feb declined less than expected while Quits and Layoffs levels surge higher.

- (Bloomberg) “New Zealand’s financial system is resilient and well positioned to support households and businesses even if economic conditions soften, RBNZ Governor Anna Breman says in a statement Wednesday alongside the Financial Stability Report.”

- (Bloomberg) “New Zealand finance companies are attracting a surge of new money as the nation’s new deposit insurance levels the playing field with banks, according to the Reserve Bank.”

- Swap rates are little changed.

- RBNZ-dated OIS pricing is little changed across meetings. 9ps of tightening is priced for May, while February 2027 assigns 105bps.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 1.50% May-31 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 5.00% May-54 bond.