US TSYS: Further Risk-Off Gains Trimmed, A Thin Docket Ahead

Oct-17 10:49

- Treasuries are off earlier fresh highs as equity futures have stabilized but on net have extended yesterday’s US regional bank driven gains, which sparked the largest curve-wide DV01 shift seen for several months.

- Regional bank earnings are likely in near-term focus at the start of the session.

- Cash yields are 0.5-3bp lower on the day, with declines led by the front end.

- The bull steepening sees 2s10s at 57bp for back close to yesterday’s 58bp, whilst 5s30s have seen highs of 106.5bp for their highest in nearly a month.

- After seeing solid support at the 4% handle for 10Y yields earlier this week, they now trade comfortably through this at 3.961% (-1.4bp). 10Y yields were last lower in early April on reciprocal tariff deliberations.

- TYZ5 trades at 113-28+ (+04+) on elevated cumulative volumes of 600k, off an overnight high of 114-02.

- It has seen clearance of key resistance at 113-29 (Sep 11 high and bull trigger), confirming a resumption of the medium-term uptrend and opening 114-10 (Apr 7 high continuation). Support is seen at 113-24 (the low with the Asia open).

- Data: We believe the mid-month estimate for Manheim used vehicle prices will be the sole data release today. Housing starts, import prices, IP and TIC flows should all be delayed by the government shutdown.

- Fedspeak: Musalem (1215ET) – see STIR bullet

- Politics: Trump in bilateral lunch with Zelensky (1315ET), Trump departs White House for Florida (1500ET)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EU-BOND AUCTION PREVIEW: EU to confirm non-competitive round to start next week?

Sep-17 10:48

- The EU will announce the details of its bond auction of Monday 22 September at midday BST / 7:00ET / 13:00CET.

- Provisionally this has been announced as the first auction at which the EU will hold a second non-competitive round (at which a further 20% would be available the following day).

- We assume that we will receive confirmation and further details of this today, alongside the bonds that will be on offer.

- We are unsure at this stage whether the non-competitive round will bring any change in sizes in the first round (we assume not) and we still expect triple line EU-bond auctions to be held for the considerable future.

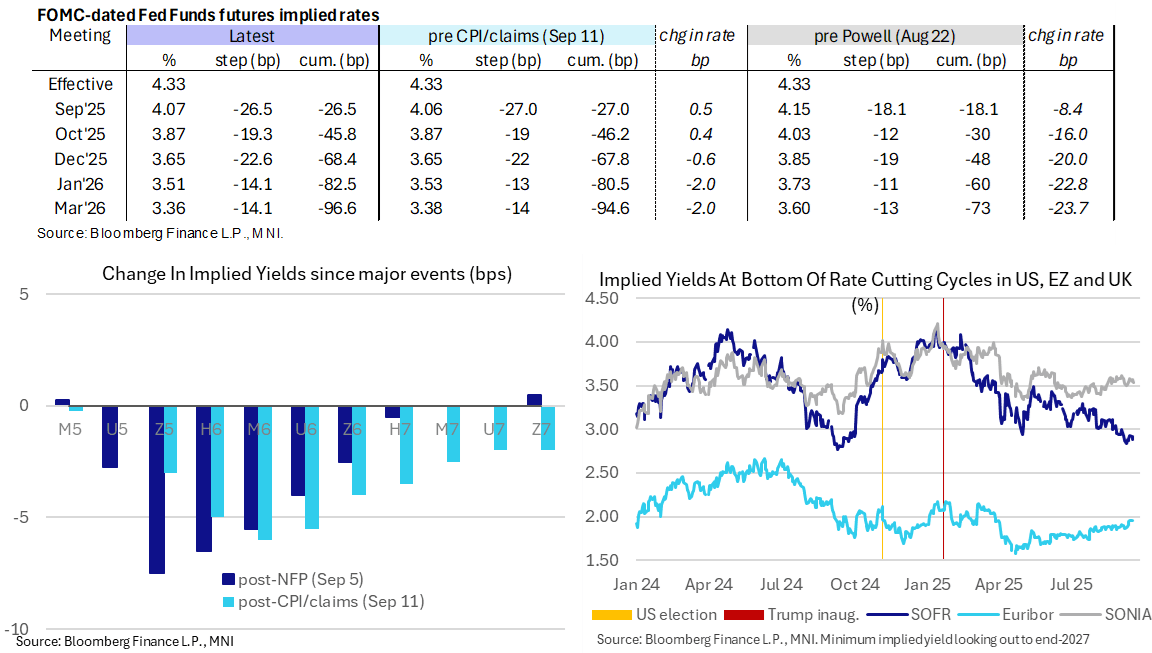

STIR: Fed Cut Pricing For Today Inches Higher But Still <10% Odds Of 50bp Cut

Sep-17 10:37

- Fed Funds implied rates have dipped 0.5bp for today’s decision in response to aforementioned flow (Ongoing trade in FFV5 with paper paying 95.945 on 7K, taken bid over), but it still points to less than 10% odds of a 50bp cut.

- It holds the broad paring in 50bp cut expectations having increased to ~20% after payrolls earlier in the month.

- Cumulative cuts from 4.33% effective: 26.5bp for today, 46bp Oct, 68.5bp Dec, 82.5bp Jan and 96.5bp Mar.

- SOFR futures are essentially unchanged on the day.

- That includes the implied terminal yield of 2.88% (SFRH7), eyeing 145bp of cuts ahead including fully priced cut. It’s within ranges for the past two weeks, including dovish extremes of ~150bp of cuts after payrolls.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Sep2025_With_Analysts_c3eababfe1.pdf

BUNDS: Looking to close the Gap

Sep-17 10:37

- The German curves are tilted to the flatter side in early trade, but the Schatz edges through the very tight intraday high with 5k lifted.

- This is underpinning Bund, albeit still just short of the earlier printed high.

- Initial area of interest in Bund, not a Tech level, is the 129.13 gap.

Trending Top

Jan-30 21:43

Jan-30 21:11