HKD: Further Phase of Spot Strength; HKD Forward Discount Narrows Again

Aug-14 13:31

- A further phase HKD spot strength has USD/HKD pressed through earlier lows (the 7.8358 print was the lowest spot rate since late May) as the front-end of the swaps curve continues to improve: one-week swap rates are now touching 1.00% to more than double today's opening levels of 0.44%.

- As was the case earlier today, no specific headline or newsflow to trigger the move, and the price action is not consistent with HKMA intervention, particularly as the price hasn't tested the weak side of the band today.

- That said, HKMA were active in buying HKD earlier this week - and once those purchases settle, the aggregate balance should drop to ~H$53bln. This, in tandem with the move in the FX swap rate should support the HIBOR fix in the short-term, although this is still well short of the correction needed to put rates on a par with levels earlier this year, or to narrow the SOFR-HIBOR spread.

- This leaves a local liquidity squeeze as the most likely driver here - on which pressure has been building over the past month or so as liquidity is withdrawn by the HKMA. We have noted the lagged effect between a declining aggregate balance and HIBOR, FX swap rates - so today's price action may be a case of catching up.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Restaurant Prices, Energy Services Boost Headline CPI

Jul-15 13:18

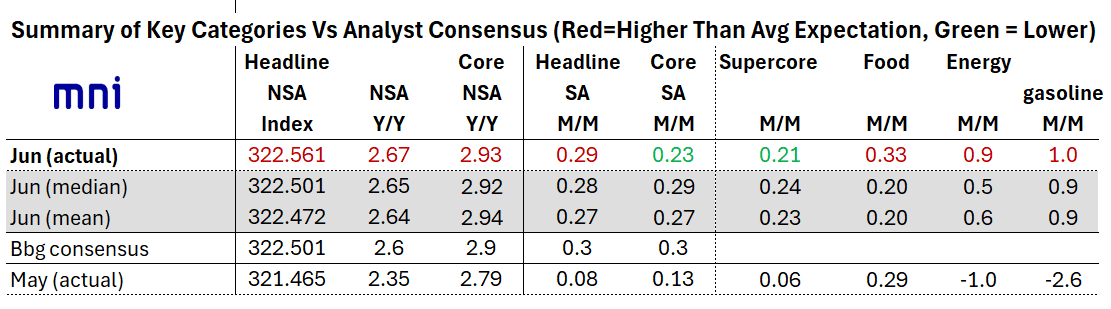

In contrast to core CPI, headline inflation was stronger in June than expected, rising 0.29% M/M (0.28% MNI median, 0.08% prior), for a 2.93% Y/Y rate (2.92% MNI median, 2.79% prior). Both food and energy came in above-expected.

- Energy had been expected to re-accelerate from -1.0% M/M in May, and duly delivered with a rise to a 5-month high 0.9% (0.946% unrounded, very close to a 1.0% unrounded figure) vs 0.5% MNI median. Gasoline was largely in-line with a 1.0% rise (0.9% MNI median, -2.6% prior), with the overall energy "beat" appearing to stem from energy services which rose 0.9% after 0.4%: gas service prices were up 0.5% after -1.0%, with electricity ticking up to 1.0% from 0.9%.

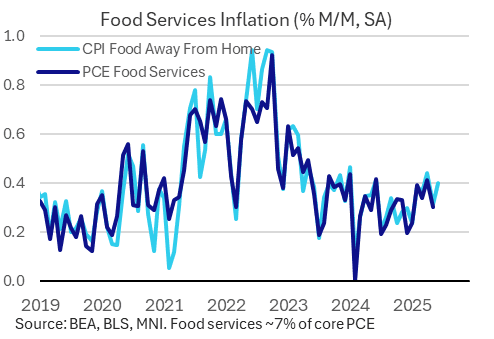

- The bigger surprise was in food prices, which rose to a 3-month high 0.33% M/M - an unexpected acceleration from 0.29% prior (0.24% MNI median expected).

- Food at home prices were steady at 0.28% M/M (0.27% prior) on a mixed performance across categories (BLS: "Three of the six major grocery store food group indexes increased in June, while the other three declined"), but food away from home inflation picked up to 0.40% (0.31% prior). The latter may provide a bit of a boost for core PCE expectations vs the initial CPI readthrough, as it feeds into the food services PCE category.'

US DATA: A Wide Range Of CPI Core Goods Items See M/M Acceleration In June

Jul-15 13:15

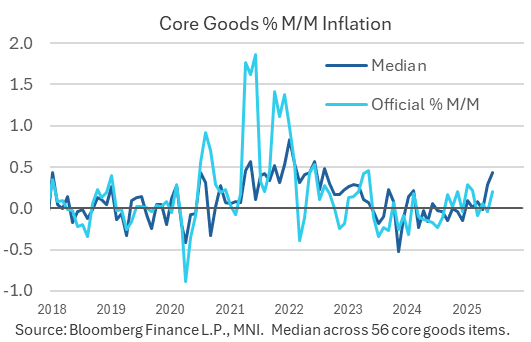

- Core goods inflation of 0.20% M/M was close to expectations in June (average of 0.18% M/M across seven analyst estimates) after -0.04% M/M in May and 0.06% in April.

- It came despite a slightly larger than expected decline in used car prices (-0.67% M/M vs median estimate of -0.50% or mean of -0.15%) along with new cars also falling -0.3% M/M.

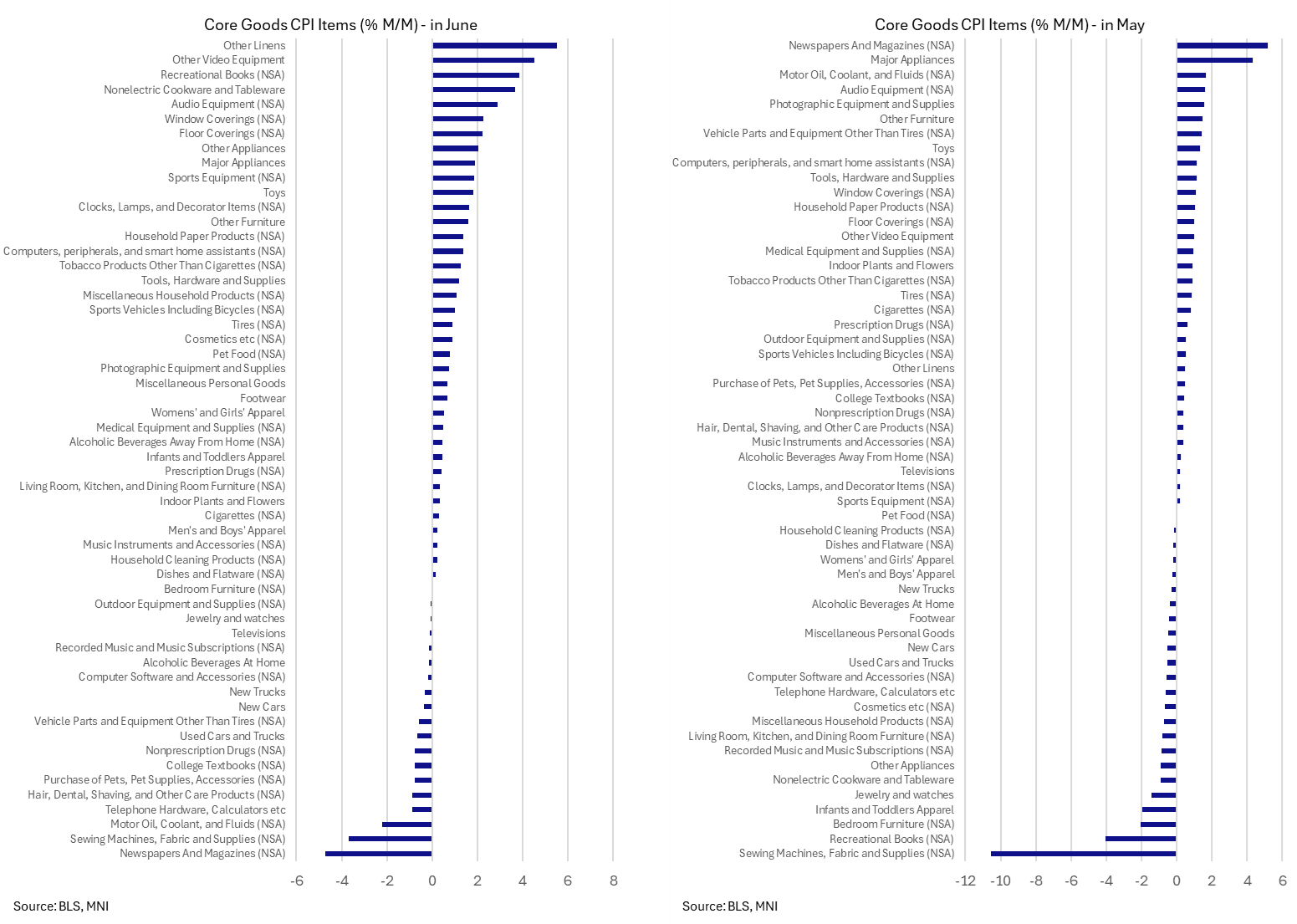

- These large ticket items masked a broader increase in core goods across 56 items for a second month, with a median increase of 0.44% M/M in June after 0.29% in May and -0.01% in April.

- This 0.44% M/M doesn’t materially change anything from a "largest since x" point (now since Aug and not Sep 2022) but is another marked acceleration – see chart.

- For context, this median averaged 0.32% in 2021 and 0.39% in 2022 and peaked at 0.84% in Jan 2022.

- One point of caution: you can see in the second chart below just how many of these series that feed into core goods are NSA.

STIR: Fed Pricing A Little More Dovish After CPI Took Edge Off Bessent's Comment

Jul-15 13:09

Fed pricing sees a modest dovish reaction to the CPI data, although the readings provided little differentiation vs. headline BBG survey expectations on net (but did include a 0.1ppt downside surprise for unrounded M/M core CPI & a 0.1ppt upside surprise for unrounded headline CPI).

- Unrounded supercore was pretty close to the average of a limited survey sample, with our macro team noting that it was core services that limited inflation, while core goods provided a slightly hawkish surprise (see previous bullets for greater details on the release)

- A reminder that hawkish adjustments were seen ahead of the data, after Treasury secretary Bessent’s left some feeling that there may have been a more hawkish surprise in the offing.

- We suggested that he may have just been referring to a roughly in-line print given consensus expectations for a move higher across the major CPI metrics vs. May levels. This seems to have been proven true.

- FOMC-dated OIS shows 1bp of easing for this month’s decision, 16bp through September, 31bp through October and 47bp through year-end.

- That compares to 1bp, 15bp, 29bp and 46bp ahead of the data and 1bp, 17bp, 31bp and 49bp before Bessent spoke.

- SOFR-implied terminal rate pricing at 3.22% vs. 3.25% ahead of the data and 3.23% pre-Bessent (corrected from 3.33% when previously published).