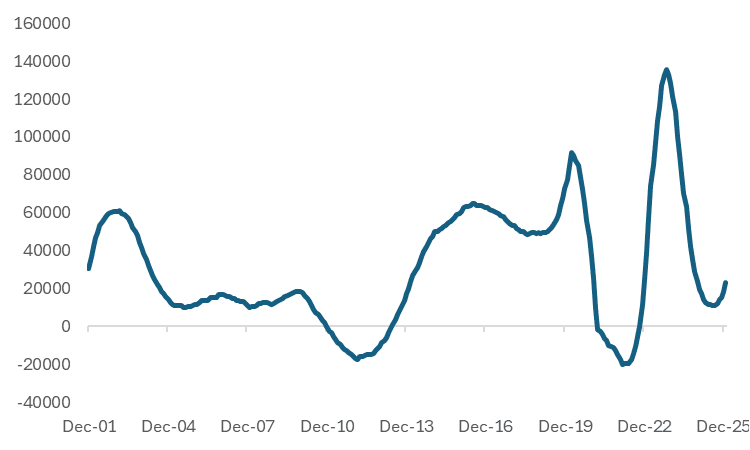

NEW ZEALAND: Further Improvement In Net Migration, But Rolling Annual Sum Modest

Jan net migration continued to improve, rising to 4460, from a revised 3600 gain in Jan. The Feb outcome was the highest since end 2023 in terms of net monthly migration. The start of 2025 was delivering close to flat net monthly migration. The rolling annual sum of net migration sits back at just over 23k. This takes us back to end 2024 levels for this metric. The chart below shows the trend improvement is coming from a low base though. Further improvement will support the broader economic recovery, all else equal.

Fig 1: New Zealand Net Migration - Rolling 12mth Sum

Source: Stats NZ/MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Richer With US Tsys, Focus Turns To Today's US NFP

NZGBs are 2-3bps richer after US tsys finished with a bull-flattener (benchmark yields 3-7bps lower).

- This came despite massive block sales over a 90 minute midday period: saw -115,000 TYH6 over 90 minutes from 112-17.5 to -15, as well as -95k FVH6 from 109-11.25 to -10.

- US tsys gained after Peter Navarro, counselor to Pres Trump, expressed the "need to revise expectations on monthly job numbers" BBG.

- All focus turns to today's US employment data. The report will need to be assessed holistically rather than focusing on any single number, although the unemployment rate should offer the cleanest single take.

- Swap rates are flat to 2bps lower, with a flatter 2s10s curve.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while December 2026 assigns 45bps.

- The local calendar will be light until Friday's release of BusinessNZ Manufacturing PMI, Net Migration and RBNZ Inflation Expectation data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond and NZ$200mn of the 4.5% May-35 bond.

Bloomberg Finance LP

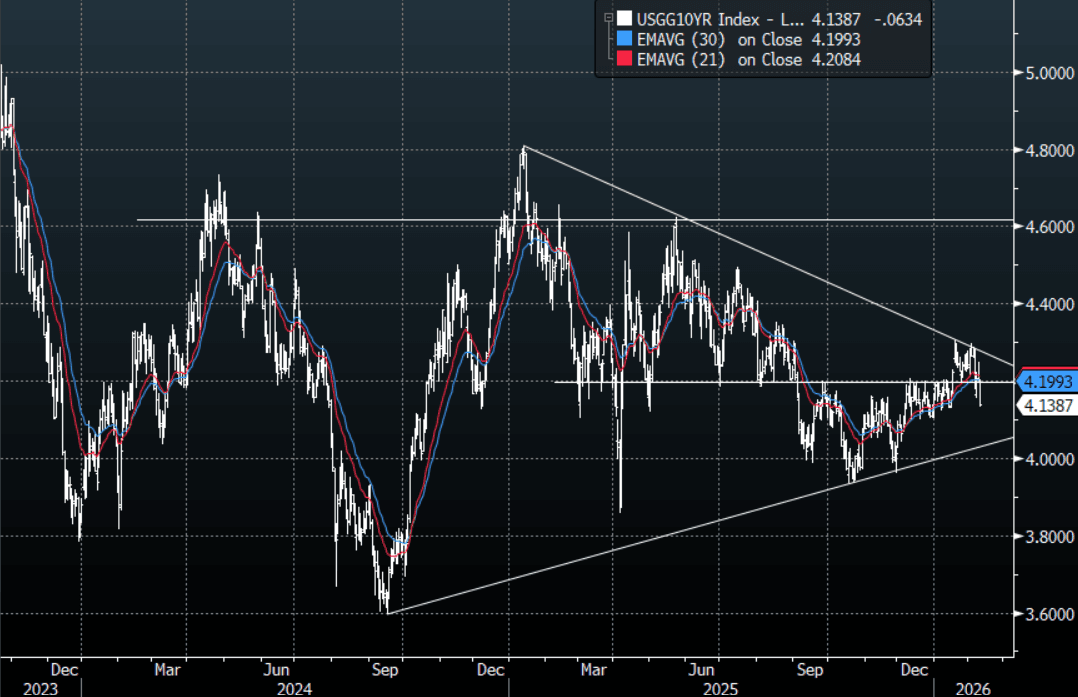

JPY: USD/JPY-Falls Through 155.00 As US Yields Break Lower Heading Into Data

The USD/JPY range overnight was 154.06 - 155.63, Asia is currently trading around 154.35. USD/JPY slipped lower again, slicing through most short-term supports as US Yields start to turn lower. The price action on Monday in response to the election outcome showed it was mostly priced in, and we have seen some “buy the rumour, sell the fact” play out. I thought we would see better demand back toward the 155.00 area initially but this move in US yields is causing the Yen shorts some angst. This price action does look messy but I still believe dips back toward the 149-152 will probably provide solid support again should we see it, until then it looks like we chop around albeit with a heavy tone as we await tonight's US labour data which will impact that move in US yields. On the day, the first resistance is back towards 155.05-155.35 and then 155.80-156.20 area as the market pares back its USD longs and looks for another base to form from which to move higher again.

- MNI BRIEF: Fed's Logan More Worried About Inflation Than Jobs. Federal Reserve Bank of Dallas President Lorie Logan said Tuesday she is more worried about persistently elevated inflation than further worsening in the labor market, and no further rate cuts would be needed if inflation comes down this year.

- MNI BRIEF: Fed's Hammack - Could Hold 'For Quite Some Time'. "Based on my forecast, we could be on hold for quite some time," she said in prepared remarks. "If we see progress on both sides of our mandate, that tells me that our policy rate is already at the right setting and that we should hold it there. Rather than trying to fine tune the funds rate, I’d prefer to err on the side of patience as we assess the impact of recent rate reductions and monitor how the economy performs."

- Options : Close significant option expiries for NY cut, based on DTCC data: 156.50($1.16b), 156.60($550mm). Upcoming Close Strikes : 158.50($1.57b Feb 13), 159.00($1.91b Feb 13),160.00($3.06b Feb 13) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 154 Points

Fig 1 : US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA: Government Bond Issuance Today

- Bank of Korea to Sell KRW500B 2.55% 1-Year Bonds

- Vietnam to Sell VND1 Trillion 4.1% 2041 Bonds

- Vietnam to Sell VND13 Trillion 4% 2036 Bonds

- Vietnam to Sell VND500 Bn 3.2% 2055 Bonds

- Thailand to Sell THB25 Bn of 2031 Bonds

- Thailand to Sell THB15 Bn of 2045 Bonds

- Malaysia to Sell MYR500 Million 365-Day Bills

- Hong Kong to Sell CNY4.0 Bn 2028 CGB Dim Sum Bonds

- Hong Kong to Sell CNY4.0 Bn 2029 CGB Dim Sum Bonds

- Hong Kong to Sell CNY3.0 Bn 2031 CGB Dim Sum Bonds

- Hong Kong to Sell CNY2.0 Bn 2036 CGB Dim Sum Bonds

- India to Sell INR140 Bn 91-Day Bills

- India to Sell INR 80 Bn 364-Day Bills

- India to Sell INR120 Bn 182-Day Bills

- South Korea to Sell KRW2.5T 63-Day Financial Bills

- Bank Indonesia to Sell 28-Day Dollar Sukuk Bills

- Bank Indonesia to Sell 89-Day Dollar Sukuk Bills

- Bank Indonesia to Sell 273-Day Dollar Sukuk Bills

- Bank Indonesia to Sell 181-Day Dollar Sukuk Bills

- Bank Indonesia to Sell 368-Day Dollar Sukuk Bills