EQUITIES: FTSE 100 Tops 10,000 For First Time

Also note that the rally in precious metals, which has provided support for mining names, has helped push the cash FTSE 100 and the futures contract covering the index above 10,000 for the first time on record.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Twist Flattening To Start

Long end UK paper rallies, taking cues from overnight trade in U.S. Tsys.

- Futures briefly rally more than 60 ticks from yesterday’s low, topping out at 91.50 before fading back below 91.40.

- Bulls remain in technical control, with our technical analyst deeming the recent pullback to be corrective.

- Initial support and resistance in the contract remain located at 90.87 & 91.93, respectively.

- Yields 1bp lower to 1bp higher, curve biased flatter. 2s10s ~3bp off last week’s post-Budget closing low, while 5s30s is ~2bp off last week’s closing low.

- Modest dovish extension in SONIA futures on the gilt open, contracts last flat to +2.5.

- Final services and composite PMI data is due this morning, tangible market reaction would only be seen on a meaningful departure from the preliminary 50.5 reading in the services PMI.

- Elsewhere comments from BoE’s Mann (hawk) are due at 17:00 London. She may not touch on monetary policy as the topic of the panel that she will appear on is “Eroding reserve currency status: A current and historical perspective”. There will be a Q&A session.

SPAIN DATA: Services PMI Downside From External Sector; Rather Bright Elsewhere

That is a downside surprise for the Spain November Services PMI (at 55.6, vs 56.3 cons) after October's 56.6 which was the highest reading since December 2024. However, the release remains quite positive, seemingly assigning the main downside in November to international demand while the overall picture remains on the brighter side. Key highlights below:

- "Spain’s service sector continued to expand markedly in November, with both activity and new business volumes rising since October despite a noticeable drop in international trade. Confidence in the outlook also remained positive, whilst firms again took on additional workers to help deal with increased workloads. "

- "However, labour costs and input prices in general were reported to have increased since October, leading to a marked rise in overall operating expenses. With output charge inflation concurrently dropping to a one-year low, operating margins subsequently came under pressure"

- "Higher activity was linked to working on new projects, existing contracts and new work. Latest data showed that demand improved again in November, with new business volumes rising for a fifth successive month. Growth was however the slowest since August, in part undermined by a drop in international sales which fell in November for the first time in five months. Moreover, the downturn was the steepest since the start of 2024. Panellists simply reported a lack of international demand."

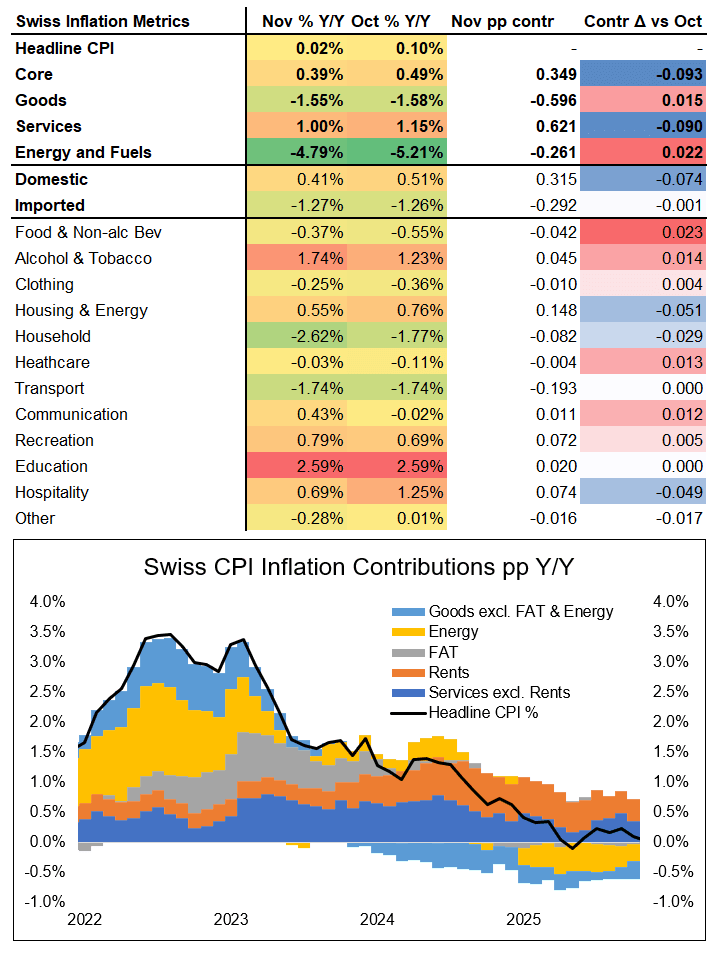

SWITZERLAND DATA: CPI Details Confirms Downside Centred Around Housing / Hotels

Looking at the details of the Swiss CPI print shows the following:

- Unrounded headline CPI was 0.02% (down from 0.10% in October, a 0.08ppt slowdown).

- Housing rentals contributed -0.05pp to the change in headline CPI (this only updates quarterly and is likely to remain persistent)

- Hospitality also contributed -0.05ppt to the change in headline CPI (coming from hotels, volatile package holidays playing only a minor part)

- Food and energy both contributed around +0.02ppt each, to partially offset this.

- These were the major drivers, for detailed calculations, see chart / table below.

What remains on net is a soft print which, while by itself is very unlikely to prompt an SNB cut into negative territory, warrants further monitoring. This applies especially as the downside this time was centred around domestic categories - which the SNB has flagged previously when looking at underlying inflationary pressures. Having said that, what's not quite so clear is their stance on the housing slowdown, with some previous comments suggesting that they merely view it as a lagged function of headline which may imply less feedthrough to policy. Also, we don't know what number they had pencilled in for rentals, either. So it's hard to know if this is the driver of the surprise, or if it is more broad based.

CHF saw a limited reaction to the release.