EURGBP TECHS: Fresh Cycle High

- RES 4: 0.8865 1.764 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 3: 0.8848 1.618 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 2: 0.8835 High May 3 2023

- RES 1: 0.8830 High Nov 5

- PRICE: 0.8811 @ 06:39 GMT Nov 6

- SUP 1: 0.8763 Low Nov 3

- SUP 2: 0.8747 20-day EMA

- SUP 3: 0.8710 50-day EMA

- SUP 4: 0.8656 Low Oct 8 and a key support

A bull cycle in EURGBP remains intact and the cross is holding on to its recent gains. A fresh cycle high this week confirms a resumption of the uptrend and maintains a bullish price sequence of higher highs and higher lows. Sights are on 0.8835, the May 3 2023 high. Initial support lies at 0.8763, the Nov 3 low. Note that the trend is overbought, a pullback would be considered corrective.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY TECHS: E-MINI S&P: (Z5) Uptrend Intact

- RES 4: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 2: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6800.00 Round number resistance and the Oct 3 high

- PRICE: 6778.75 @ 07:26 BST Oct 7

- SUP 1: 6694.17 20-day EMA

- SUP 2: 6624.25 Low Sep 25

- SUP 3: 6575.48 50-day EMA

- SUP 4: 6506.50 Low Sep 5

A bull cycle in S&P E-Minis remains intact. The contract traded to a fresh cycle high last week to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6694.17. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6575.48.

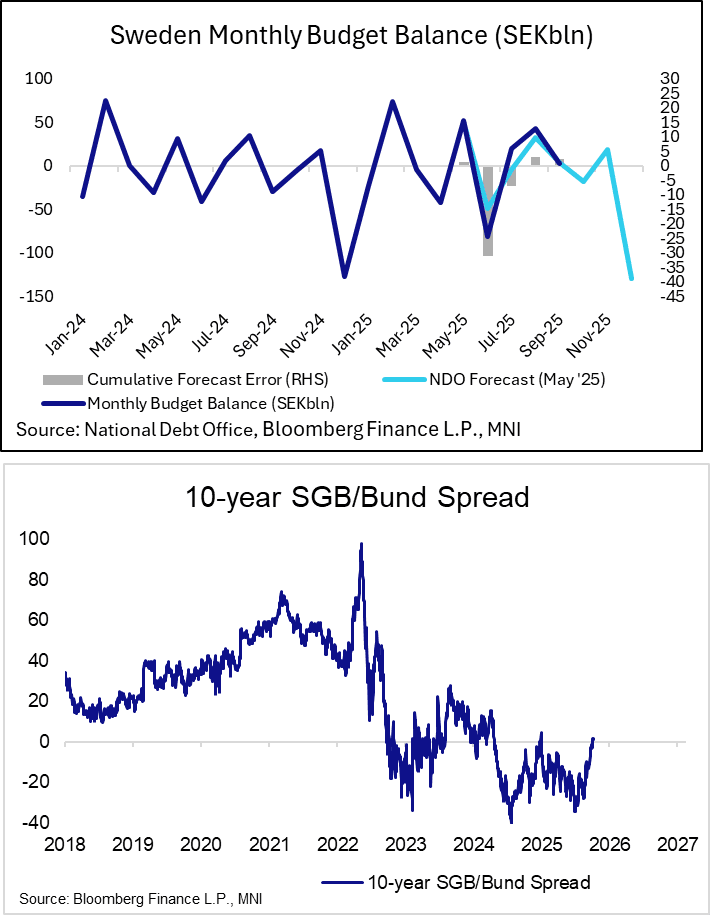

SWEDEN: Anticipated Increase In Borrowing Has Cheapened SGBs Since Aug

The Swedish budget surplus was SEK2.1bln in September, down from SEK42.9bln in August. This was a touch below the National Debt Office’s (NDO) SEK3.1bln surplus forecast from the May borrowing report. Since May, the cumulative NDO forecast error amounts to just SEK2bln. As such, most of the expected increase in borrowing in the November report will be driven by the Government’s expansionary 2026 fiscal package.

- In the May borrowing report, the NDO assumed SEK35bln of unfunded fiscal policy measures for 2026, well below the SEK80bln that was announced in August (and formally delivered in September).

- Taken alongside an increase in defence spending and Ukraine aid, the net borrowing requirement is set for another sizeable increase.

- Preliminary analyst estimates we have seen look for an increase in nominal bond auction sizes from SEK6bln to SEK7-8.5bln from next year to help finance the higher deficit.

- This increase in net supply has underscored expectations for a cheapening of nominal SGBs against peers (e.g. Bunds) and swaps in recent months. A good deal of these moves have already played out – the 10-year SGB/Bund spread has widened ~30bps since mid-August when the initial budget figures were announced.

- In September, the primary balance was SEK11.3bln lower than forecast, an expected dynamic due to the timing of a recent EU RRF payment (which came in July versus NDO expectations of September). However, this was offset by SEK10.3bln lower-than-expected net lending to government agencies. The NDO's next borrowing report will be released on November 27.

USD: USDJPY is heading towards big levels

- The early flows in G10 FX is the upside continuation for the Dollar, the Greenback is in positive Territory against all the majors, and test a intraday high versus the Yen, EUR, GBP, AUD, CAD, CHF, PLN, CZK, MXN and MYR.

- The Kiwi was and still is the worst performing major Currency, down 0.50%, albeit short of Yesterday's printed low of 0.5810 and the initial small support noted at 0.5803.

- The USDJPY is the early cross to watch, it is heading towards some big levels as Market participants positioned for a slower Rate Hike following Takaichi's win and stimulus stance.

- The Next big level in USDJPY comes at 150.92 High Aug 1 and a key resistance.