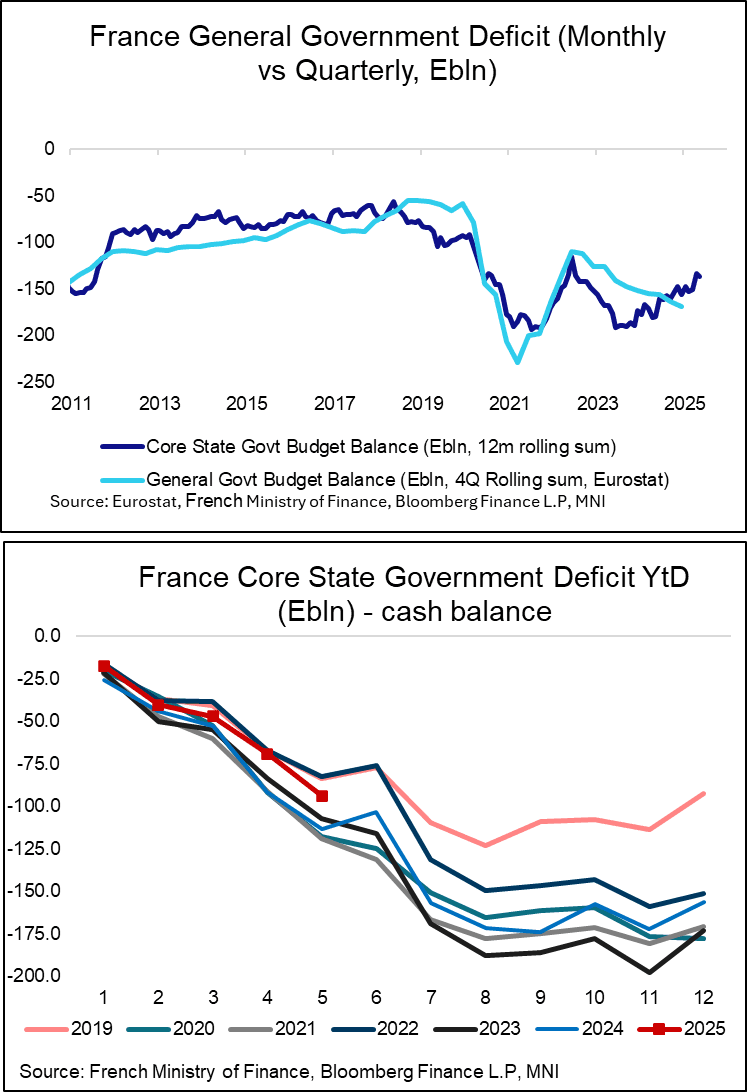

EUROPEAN FISCAL: France YTD Budget Deficit Tracks Below 2023/2024 Outturns

The French year-to-date budget deficit widened to E94bln in May, a step up from E69.3bln last month but comfortably below the E113.5bln seen in May 2024 and E107.2bln in May 2023. Although fiscal consolidation appears to be progressing from this perspective, last week the French government said it needs to find an extra E5bln of spending cuts to achieve its 5.4% deficit to GDP target. That's on top of the E40bln in savings required to meet its 4.6% 2026 target, with proposals set to be announced this month before a vote in the autumn.

- The press release notes that expenditures were E189.6bln in May, down from E197.6bln a year ago. Meanwhile, revenues were E137.8bln, up from E126.1bln a year ago.

- Yesterday, PM Bayrou survived a no-confidence vote following a breakdown in talks over controversial pension reforms pushed through by President Emmanuel Macron in 2023. This was an expected outcome, with the far-right RN party abstaining from the vote.

- With the National Assembly set to go on its summer recess from mid-July until September, the Bayrou gov't is likely safe until the 2026 budget process gets underway.

- Alternatively, from 7 July (one year after the last election) President Emmanuel Macron could look to dissolve the National Assembly and hold a snap election. This would be an even riskier move than in 2024, with his centrist alliance polling poorly and at risk of further seat losses.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Long End Futures are drifting lower

- The German and US Treasuries curves started flatter, but there's a small unwind here as the 30yr Futures have caught up to the downside, the German Buxl and TBond are back at session low, helping drag the rest of the strips lower.

- Small support in Bund is at 130.94, but most investors will be seeing better at 130.39.

SPAIN DATA: May Manufacturing PMI: Some Signs Of Tariff Reprieve

The Spanish May manufacturing PMI surprisingly moved into expansionary territory for the first time since January at 50.5, above the six-analyst strong consensus of 48.4 (vs 48.1 prior). The details of the release suggest some tariff reprieve was at play in May, but sales volumes were still down on the domestic and export markets.

Key notes from the release:

- "Supporting the PMI was a return to growth in manufacturing output following April’s contraction"..."Some panellists linked higher production to a relatively better trend in underlying demand and a partial lifting of global tariff uncertainty that weighed so heavily on market activity in April".

- "Sales volumes were down in May, but only modestly and to the least extent for four months. Similarly, new export orders fell to a much lesser degree. Several panellists noted a relative improvement in European and US demand, albeit still characterised by some hesitation in committing to new work amid the uncertain tariff outlook".

- "Sentiment about output for the next 12 months improved during May to a three-month high. There are expectations amongst many panellists for a more stable economic environment in the year ahead and that previous commercial actions and investment will bear fruit"

- "The soft trend in buying activity helped to explain a drop in input prices during May, which were down for the first time since the start of 2024"..."Despite falling demand and lower prices, supply side delays were again reported".

- "Firms sought to support their own sales by cutting output charges amid reports of intensive market competition".

SWITZERLAND DATA: Retail Sales Weak In April, Clothing/Footwear Driven

Swiss real retail sales were rather weak in April, printing -0.3% M/M (seasonally-adjusted) and 1.3% Y/Y (calendar adjusted, weakest yearly rate since June 2024). Overall, the print might be consistent with Swiss economic conditions cooling a little in Q2 vs a strong first quarter - the KOF barometer also indicated softer sentiment for the months ahead.

- On a broad Y/Y 3m average basis, Swiss retail sales continue to print above their long-term average recently - suggesting that the sector overall is in solid shape. However, the drop from March was noticeable also here - see first chart below.

- The April weakness appears to be driven by the clothing and footwear category, which can be volatile but saw its softest consecutive print since October 2024. Most other categories were also on the weaker side in April (see bottom chart).