EU CONSUMER CYCLICALS: Flutter: UK Tax Increase (x2)

(FLTR: Ba1/BBB-/BBB)

It's better than worst-case leaks/proposals (50% duty on gaming). For clarity;

Online gaming duty rises from 21% to 40%

- Online sports betting from 15% to 25%

Flutter did $1.7b/$1.74b revenue in each last year.

Unmitigated it is a circa $0.5b earnings hit.

It reported $1.1b in UK EBITDA last yr, which made up 46% of group earnings.

That same amount would be smaller this year (~mid-30%) on Italy acq. + US growth.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ECB: Q3 SAFE Survey Seems Consistent With Steady Policy Rates

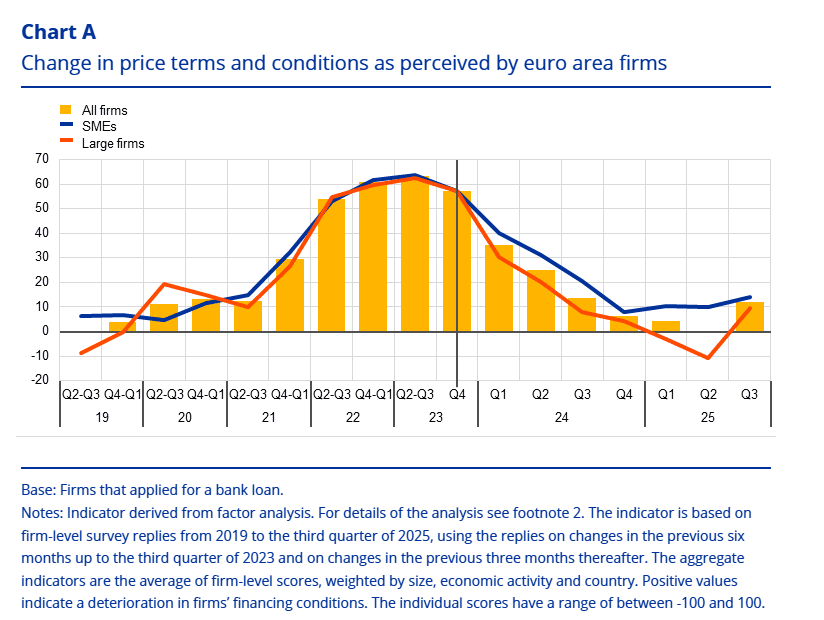

The ECB's Q3 SAFE survey did not send a clear signal for the ECB, thus is consistent with current signalling that rates are in a “good place”. While there was a slight tightening in financing conditions, this came alongside a strengthening in selling price, wage and non-labour input cost expectations over the next twelve months.

- The ECB surveyed over 10,000 firms in the latest SAFE round, of which 93% had fewer than 250 employees.

- The write-up notes that "an indicator of overall firms’ financing conditions constructed using firms’ responses shows a slight tightening"..."Across firm sizes, both SMEs and large firms reported a tightening impulse, reversing the easing observed among large firms in the previous quarter".

- Coming alongside growing consensus that the ECB is at (or at least very close to) the end of its easing cycle: "The survey results indicate that bank lending conditions have tightened marginally, with firms reporting a small net increase in interest rates charged on bank loans, following significant declines in the previous two waves. "

- "Firms continued to perceive the general economic outlook to be the main factor constraining the availability of external financing", while "firms continued to signal a deterioration in profits".

- "The availability of skilled labour, production and labour costs remain major concerns limiting production". Note that the EC's quarterly survey is due this week, which will include questions on capacity constraints in manufacturing and services.

- On prices: "Firms expected stronger increases in selling prices, wages and non-labour input costs over the next 12 months".

- Meanwhile, inflation expectations were steady: "Euro area firms’ median inflation expectations remained at 2.5% for the one-year horizon and at 3% for the three and five-year horizons"

- A reminder that both the Q3 Bank Lending Survey and the ECB's September consumer expectations survey are released tomorrow morning.

GLOBAL POLITICAL RISK: MNI POLITICAL RISK ANALYSIS - Week Ahead 27 Oct-2 Nov

Download Full Report Here

Monday 27 October:

- Japan-US: US President Donald Trump began a three-day state visit, starting with a ‘courtesy call’ meeting with Emperor Naruhito in Tokyo. Trump’s first in-person talks with new Prime Minister Sanae Takaichi will take place on the morning of Tuesday, 28 October, before Trump inspects troops aboard the USS George Washington and attends a dinner with business leaders in the evening. For Takaichi, a key aim of Trump’s visit will be to gain assurances that Japan will not face higher trade tariffs and that the US will maintain its security support in the Indo-Pacific.

EQUITIES: US Cash Opening Calls

SPX: 6,857.5 (+1.0%); DJIA: 47,503 (+0.6%/+296pts); NDX: 25,714.6 (+1.4%).