LATIN AMERICA: Fixed Income Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.64% -1bp

10yr UST 4.08% -1bp

5s-10s UST 44.0 +0bp

WTI Crude 57.9 -1.1

Gold 4083 +6.1

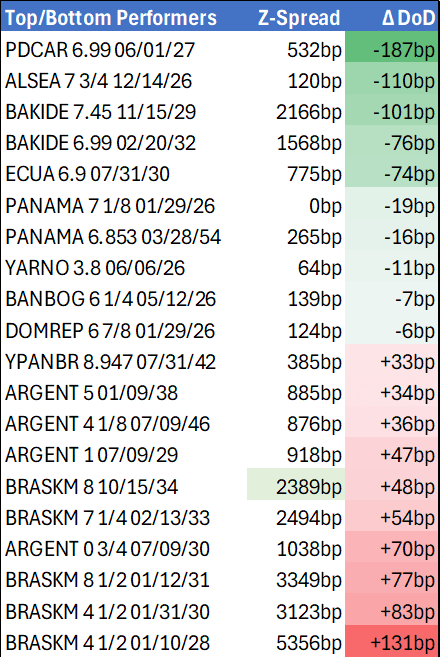

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 834bp +34bp

BRAZIL 6 1/8 03/15/34 241bp -0bp

BRAZIL 7 1/8 05/13/54 318bp -1bp

COLOM 8 11/14/35 302bp +5bp

COLOM 8 3/8 11/07/54 371bp +5bp

ELSALV 7.65 06/15/35 357bp +2bp

MEX 6 7/8 05/13/37 227bp -2bp

MEX 7 3/8 05/13/55 270bp -1bp

CHILE 5.65 01/13/37 125bp -0bp

PANAMA 6.4 02/14/35 226bp -0bp

CSNABZ 5 7/8 04/08/32 725bp +4bp

MRFGBZ 3.95 01/29/31 294bp -2bp

PEMEX 7.69 01/23/50 486bp +3bp

CDEL 6.33 01/13/35 184bp +0bp

SUZANO 3 1/8 01/15/32 174bp -1bp

FX Level Δ DoD

USDBRL 5.40 +0.07

USDCLP 939.30 +9.78

USDMXN 18.5 +0.09

USDCOP 3808.56 +44.62

USDPEN 3.39 +0.01

CDS Level Δ DoD

Mexico 102 1

Brazil 146 1

Colombia 205 3

Chile 53 0

CDX EM 98.24 0.03

CDX EM IG 101.28 0.00

CDX EM HY 94.73 (0.07)

Main stories recap:

· Treasury yields inched a bp lower while major U.S. equity indexes rallied strongly as influential Fed NY President John Williams leaned towards a December rate cut.

· LATAM secondary market benchmark USD bond spreads widened 1-3bp.

· Argentina sovereign bond prices fell ½ - 1 point as the govt. reportedly is talking with international banks about a short term borrowing secured by investments (repo) to help pay for 2026 debt payments.

· Ecuador sovereign bonds rose a point after Fitch upgraded debt ratings to ‘B-‘ from ‘CCC+’.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Corrective Pullback

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4167 50.0% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.4111 High Apr 10

- RES 1: 1.4080 High Oct 16 and the bull trigger

- PRICE: 1.3998 @ 15:47 BST Oct 22

- SUP 1: 1.3976/3900 20- and 50-day EMA values

- SUP 2: 1.3821 Bull channel base drawn from the Jul 23 low

- SUP 3: 1.3727 Low Aug 29 and a bear trigger

- SUP 4: 1.3689 Low Jul 28

USDCAD has pulled back from its recent highs. The trend condition remains bullish and a move lower is considered corrective. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.4111, the Apr 10 high, and further out, scope is seen for an extension towards 1.4167, a Fibonacci retracement. First key support lies at 1.3900, the 50-day EMA. Support at the 20-day EMA lies at 1.3976.

US OUTLOOK/OPINION: GS Below Consensus For CPI, Helped By Lower Airfares

Goldman Sachs are at the dovish end unrounded analyst estimates we've seen for monthly CPI inflation in Friday's September release, eyeing core CPI at 0.25% M/M after the 0.35% M/M in August and headline CPI at 0.33% M/M. We judge the median unrounded analyst estimate to be at 0.32% M/M for core CPI, with a range of 0.25-0.36%.

- Four key component-level trends Goldman expect to see in this report:

- “unchanged used car prices, reflecting the signal from auction prices, and a modest increase in new car prices, reflecting downward pressure on consumer prices from increased dealer incentives.”

- “a 0.3% increase in the car insurance category based on premiums in our online dataset.”

- “a 1.5% decline in airfares in September, reflecting a fading boost from seasonal distortions and a decline in underlying airfares based on our equity analysts’ tracking of online price data.”

- “upward pressure from tariffs on categories that are particularly exposed, such as communication, household furnishings, and recreation, worth +0.07pp on core inflation.”

- “Over the subsequent few months, we expect tariffs to continue to boost monthly inflation and forecast monthly core CPI inflation of around 0.2-0.3%. Aside from tariff effects, we expect underlying trend inflation to fall further, reflecting shrinking contributions from the housing rental and labor markets.” They see core CPI at 3.1% Y/Y in Dec 2025 and core PCE at 3.0% Y/Y (or 2.2% for both excluding tariff effects).

US TSYS: Tsys Buoyed Amid Ongoing Trade Tensions

- Treasuries look to finish modestly higher Wednesday, reversing midmorning losses after Reuters reported the Trump admin "is considering broad restrictions of exports to China made with US software, citing an unnamed US official and three people briefed by US authorities."

- No noticeable reaction in rates after late Bbg headline: "US TO ANNOUNCE 'PICK UP' IN RUSSIA SANCTIONS TODAY OR TOMORROW".

- Treasury futures gain slightly (TYZ5 113-24 +0.0) after $13B 20Y Bond auction re-open (912810UN6) stopped through - drawing a high yield of 4.506% vs 4.517% WI at the cutoff; 2.73x bid-to-cover vs. 2.74x prior.

- The Wall Street Journal reports citing sources that the ADP has stopped providing the Fed with weekly data on private payrolls and earnings. Per the WSJ piece, the Fed has had access to the data since "at least 2018", and was available to the Fed with "a roughly one-week delay". The publicly-available ADP payrolls report is published monthly.

- Equity earnings expected to release after the close include Southwest Airlines, Raymond James, Churchill Downs, Alcoa, Crown Castle, United Rental, Lam Research, Tesla and IBM.

- Thursday's weekly Jobless Claims & Chicago Fed data suspended.