US TECHNOLOGY: Fiserv: 3Q25 Results (x2)

S&P and Moody's have downgrade thresholds at 3.0x and 3.5x, respectively. Assuming no debt funded share repurchases or M&A, we see leverage at 3.2x and 3.1x at the end of 2025 and 2026 respectively. FI has historically managed its leverage within its 2.5x-3.0x target range and can flex share repurchases to maintain it, which are currently tracking at 150% LTM FCF. The new CFO was previously CFO at GPN after Tsys transaction (2019-2022) where he oversaw an active M&A period. While we still expect FI will be active in M&A, we expect transactions will be modest in size. We struggle with the rationale behind today's significant guidance reduction, but view a +20bps move as overdone.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Oct01 $1.1600-10(E3.3bln), $1.1700-10(E2.1bln), $1.1750(E1.3bln), $1.1791-00(E1.7bln), $1.1900(E1.3bln); Oct02 $1.1695-00(E1.5bln), $1.1750(E1.1bln), $1.1785-90(E2.5bln); Oct03 $1.1700(E1.1bln), $1.1845-55(E1.9bln), $1.1875(E1.2bln)

- USD/JPY: Oct02 Y147.95-00($1.4bln), Y149.50($1.0bln)

- AUD/USD: Oct01 $0.6600-10(A$1.1bln), $0.6700(A$1.6bln); Oct02 $0.6600(A$1.7bln); Oct03 $0.6600(A$1.5bln)

US: Speaker Johnson To Keep House Recessed During 'Shutdown Week'

Jake Sherman at Punchbowl News reporting on X that House Speaker Mike Johnson (R-LA) told Republican representatives in a conference call that he intends to bring the House of Representatives back from recess next week. Keeping the lower chamber shuttered this week suggests that the only route out of a government shutdown on October 1 is a capitulation from Senate Minority Leader Chuck Schumer (D-NY) or an unlikely 'handshake' deal with President Donald Trump and Republican leaders on an 'Obamacare' subsidy vote.

- Sherman notes that Johnson said that he wants Republicans to be 'unified'. On the call, he expressed 'confidence' about the GOP's position -- they passed a clean CR.

- On the conference call, lawmakers were told that House and Senate GOP leadership will have a joint news conference Wednesday morning, the first morning of a potential shutdown. Johnson also advised Republican lawmakers to "eschew political events during a shutdown," likely offsetting the risk of negative publicity.

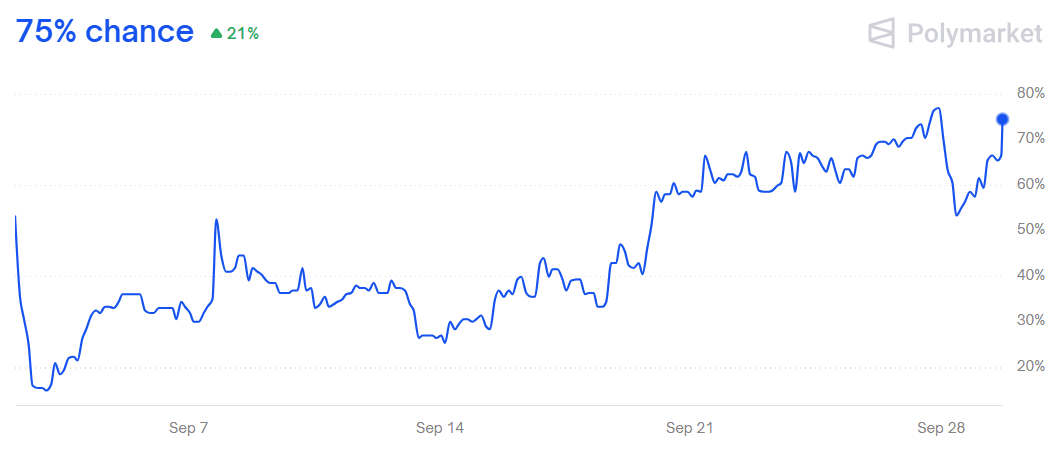

- Although there have yet to be any reported comments from Schumer, the most important figure in the shutdown standoff, Polymarket recorded a spike in the implied probability of a shutdown following Johnson's comments.

Figure 1: Government Shutdown on October 1

Source: Polymarket

US DATA: BLS's Shutdown Plan Confirms Key Data Wouldn't Be Published

The Bureau of Labor Statistics' key economic releases would be postponed in the event of a government shutdown, per the Department of Labor's plan for such an event - PDF link.

- "BLS will suspend all operations. Economic data that are scheduled to be released during the lapse will not be released. All active data collection activities for BLS surveys will cease. The BLS website will not be updated with new content or restored in the event of a technical failure during a lapse."

- Furthermore: "The releases of economic data will likely be delayed if a lapse is prolonged....A reduction in quality of data collected might impact the quality of future estimates produced."

- This was largely expected - at least for the key BLS data points in the next couple of weeks, namely the September employment report (due out this Friday Oct 3) and the September CPI report (due out Weds Oct 15)), as well as PPI (Oct 16). The shutdown would begin at midnight on Wednesday October 1 unless agreement is reached on government funding.

- It was unclear whether the weekly jobless claims reports would still be published, however, since while they are compiled and released by the BLS, they use state-by-state data and were published in 2013 during the last full federal government shutdown.