EUROPEAN INFLATION: Final German June Data Confirms Soft Services [1/2]

Jul-10 08:11

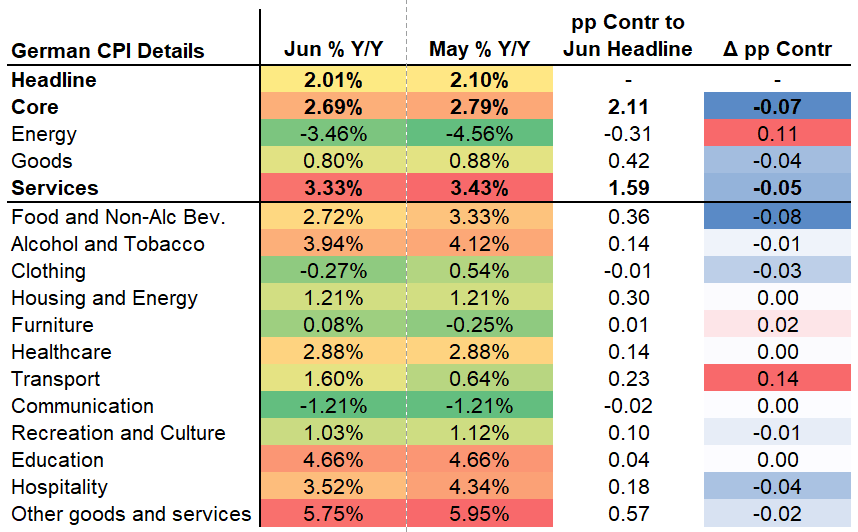

German final June HICP was unrevised from the flash readings at 2.0% Y/Y (2.1% prior) and 0.1% M/M. The final reading to CPI was also unrevised at 2.0% Y/Y (2.1% prior) and 0.0% M/M. Core CPI printed at 2.7% Y/Y (2.8% prior).

- Overall, the CPI data confirms the main conclusions from the flash reading. Services decelerated to 3.3% (as projected by MNI after state-level data, that was a downside surprise to consensus), the lowest rate since December 2023, with the contribution vs May falling 0.05pp. Goods inflation was also slightly softer (contribution-0.04pp vs May), driven by food.

- Within the services-heavy subcategories, restaurants and hotels inflation stood out in June, decelerating 0.8pp to 3.5% Y/Y, as projected after state-level data. The full 0.04pp contribution decrease was driven by hotels, the final data reveals.

- Analysts' prediction that energy was to accelerate has materialized; the category came in at -3.5% Y/Y, as in the flash release (-4.6% prior).

- This also filtered through to the transport category, with 0.09pp out of the 0.14pp higher contribution from transport being driven by motor fuels. 0.04pp came from airfares, meanwhile.

- Food inflation meanwhile was the main downside driver vs May (contribution decreased by 0.08pp). Looking deeper into the data shows that declines were quite broad-based here in June.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBP: Corrective Phase Lower Hinges on BoE Pricing, DXY Downtrend

Jun-10 08:04

GBP/USD's post-data sell-off is holding, but the sustainability of a corrective phase lower will hinge on conviction in BoE pricing and a nascent downtrendline in the USD Index.

- Weakness in GBP came in two phases this morning, first on the soft payrolls data, and then again on the SONIA open, with GBPUSD nearing 1.3462, its 20-day EMA. A clear break of this average would suggest potential for a deeper correction and expose the 50-day EMA for direction, at 1.3299. EURGBP meanwhile has cleared 0.8440, its 50-day EMA and key resistance, exposing 0.8541, the May 2 high.

- The sustainability of the move hinges in the short-term on BoE pricing: we note that OIS markets are returning closer to a further 2 x 25bps rate cuts this year: 46bp of cuts priced through December, with the next 25bp step almost fully priced at the September MPC.

- Should this pricing stick (or extend), the USD Index will come into sharper focus, with today's USD relief rally prompting the DXY to narrow the gap with a key downtrendline drawn off the early February highs - today at 99.575, a level across which markets were rangebound in the aftermath of Trump's Liberation Day announcement. This level could prove key into the US CPI print tomorrow.

Figure 1: Sustainability of GBP/USD Dip Could Hinge on USD Index Downtrendline

Source: Bloomberg Finance L.P. / MNI

GILT SYNDICATION: New 1.75% Sep-38 I/L gilt: Books open

Jun-10 08:03

- Guidance: 1.125% Nov-37 I/L gilt +11.75/+12.25bps

- Size: GBP Benchmark (MNI expected GBP3.5-5.0bln nominal with risks skewed to smaller)

- Maturity: 22-Sep-38

- Exp. Settlement: 11-Jun-25 (T+1)

- Coupon: 1.75% SA, ACT/ACT, short first to 22-Sep-25

- ISIN: GB00BMY62Z61

- Joint Leads: Barclays (B&D/DM), Citi, Nomura, RBC

- Timing: Books open, today’s business

From market source / MNI colour

EURIBOR OPTIONS: Longer dated Put Fly

Jun-10 07:47

ERH6 98.50/98.25/97.75p fly bought 2.75 in 5k.