EUROPEAN INFLATION: Final German August Data Sees Food, Energy Upward Drivers

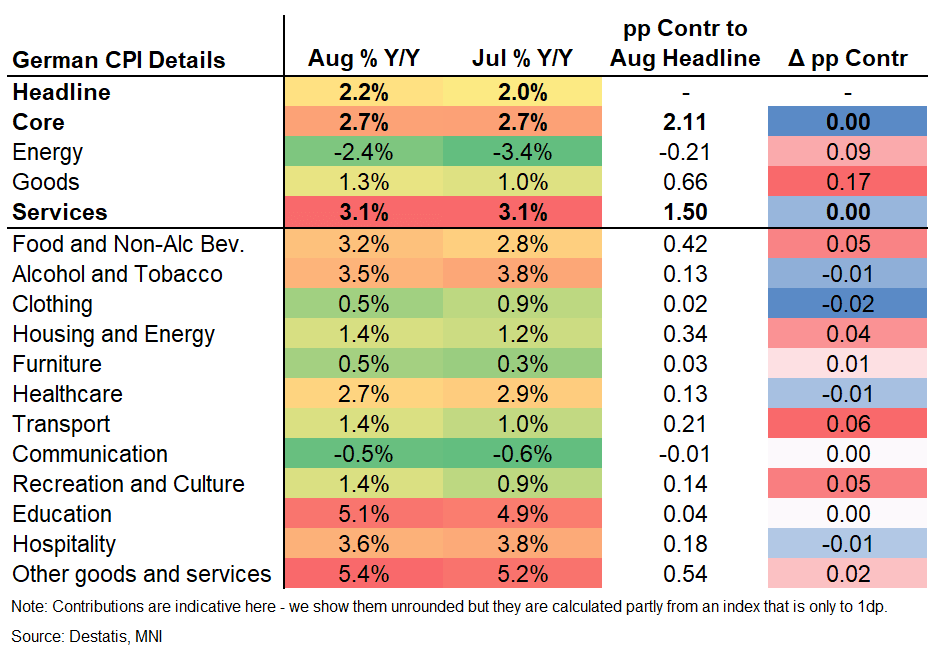

German final August HICP was unrevised from the flash readings at 2.1% Y/Y (1.8% prior) and 0.1% M/M. The final reading to CPI was also unrevised at 2.2% Y/Y (2.0% prior) and 0.1% M/M whilst core CPI printed at 2.7% Y/Y for the fourth consecutive month. The main conclusions from the flash reading were confirmed.

- Services remained at 3.1% Y/Y (as tracked after state-level data), the joint lowest rate since August 2022, with the contribution vs July unchanged. Goods inflation meanwhile accelerated, with a 0.17pp higher contribution to headline, mostly on the back of higher food and energy.

- Within the services-heavy subcategories, moves were mixed and limited for the most part. Recreation and culture stands out the most, increasing 0.05pp in contribution at 1.4% Y/Y (we saw it at 1.4% following state-level data).

- Behind the acceleration in the mixed-weighting transport category (1.4% vs 0.9% prior, we sat it at 1.4-1.5%), the main mover was auto fuel at -2.5% Y/Y (-4.6% prior). That also prompted a higher reading in overall energy (-2.4% vs -3.4% prior, contribution +0.09pp higher vs July).

- Food (and non-alc. beverages) meanwhile climbed to its highest rate since January 2024, at 3.2% Y/Y, adding 0.05pp in contribution vs July.

- Clothing and footwear meanwhile has given away some of its gains seen in July (which were driven by changing or less material seasonality around summer sales), printing at 0.5% Y/Y this time, also where we saw it after state-level data (0.9% July, -0.3% June).

- [See the disclaimer below the table on using the changes in contributions with caution]

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (U5) Holds Ground

- RES 4: 113-23 76.4% retracement of the Sep’24 - Jan’25 sell-off

- RES 3: 113-07 76.4% retracement of the Apr 7 - 11 sell-off

- RES 2: 112-23 High May 1

- RES 1: 112-15+ High Aug 5

- PRICE: 112-00 @ 08:36 BST Aug 13

- SUP 1: 110-19+/08+ Low Jul 24 / Low Jul 14 & 16

- SUP 2: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 3: 109-28 Low Jun 6 and 11

- SUP 4: 109.25 Low May 27

Treasury futures spiked sharply on the CPI print, hitting 112-06 before fading into the close. Despite the intraday reversal off highs, the bullish theme persists, supported by the clearance of the bull trigger at 112-12+, the Jul 1 high, on the NFP reaction. Prices remain toward the upper-end of the range, keeping the May 1 high at 112-23, the next upside level. Clearance here opens retracement levels layered between 113-07 and 113-23. On the downside, key support is 110-08+, the Jul 14 and 16 low. First support lies at 110-19+, the Jul 24 low.

USD: Cable Breaks Yesterday's high

- The Kiwi has taken over the SEK as the early best performer against the Greenback within G10 Currencies, now half a percent up, and looking to break back above 0.6000, with small resistance seen at 0.6011.

- The Pound might not be the best performer for Today, but it is up 1.41% for the past 5 days and leading, has broken above yesterday's high, and Market Participants will now be watching for the next resistance at 1.3589 High Jul 24.

(Chart source: MNI/Bloomberg Finance LP).

BUNDS: ING Wary Of Higher Long-End Yields & Steeper Curves

ING believe that “the long end will remain susceptible to yield increases”.

- “10s30s is testing the highs of 2021 again, but more common when the ECB rate cycle bottomed were curves of 60bp and beyond. Also, the underlying swap curve is still some 20bp away from the highs of 2021”.

- They still expect “further pressure to materialise for (ultra-) long-end rates from German fiscal policies as well as the ongoing transition of Dutch pension funds to the new defined contribution system. And that is on top of any bearish impulses that could still come from outside the Eurozone”.