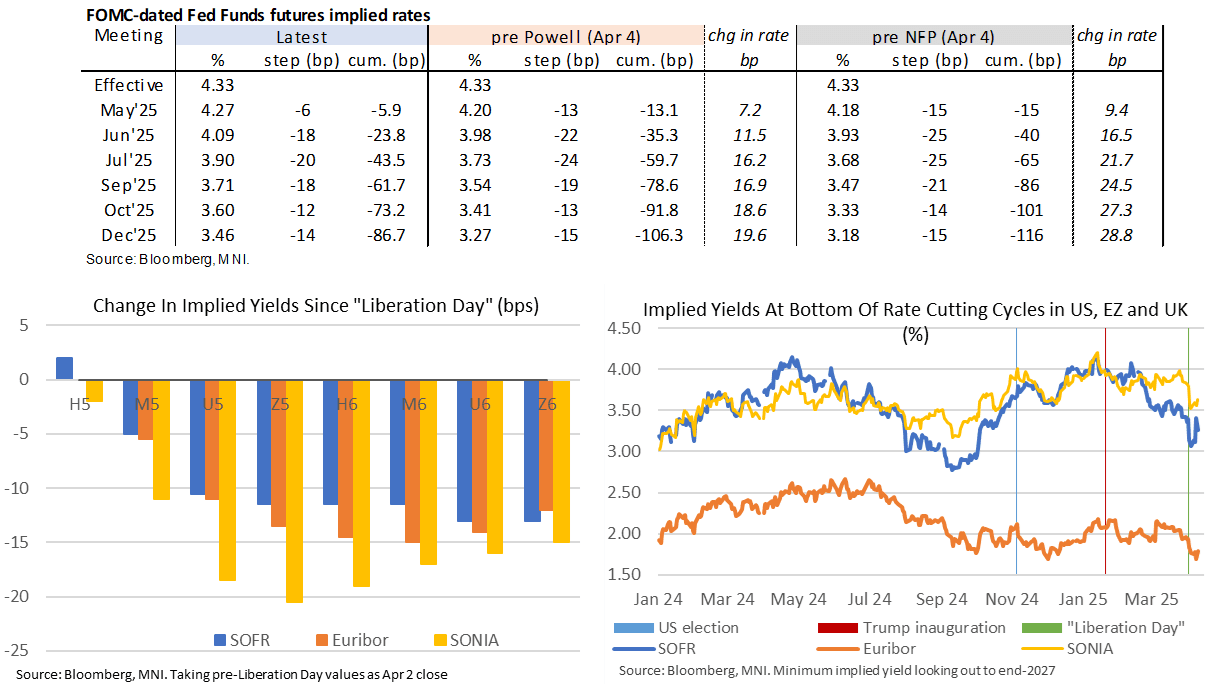

STIR: Fed Rates Pare Hawkish Shift, Still Very High Average Tariff Rate

- The Fed rate path has continued to pull back off yesterday’s hawkish extremes as part of the broader paring of risk touched in earlier comments.

- The 86bp of cuts priced for 2025 as a whole is down from yesterday’s 70bp although still a marked shift from ~100bp prior to Trump’s announcement.

- Cumulative cuts from 4.33% effective: 6bp May, 24bp Jun, 44bp Jul and 86bp Dec.

- Intermeeting cut odds are more negligible now, with FFJ5 showing just 1bp of cuts (vs as high as 6-7bp this week).

- In initial reaction yesterday, JPMorgan pushed their next Fed rate cut out to September from June previously but still see the top of the target range hitting 3.0% by 2Q26.

- Minneapolis Fed’s Kashkari (’26 voter) meanwhile sees a little less inflation impact if the tariff pause endures after yesterday’s dramatic changes although still sees a high bar for cutting rates.

- There’s much discussion about the still high average US tariff rate that’s in place and the caveat that it's now much more concentrated on China. For instance, JPM in yesterday’s reaction: “In static terms, today’s moves would actually increase the average effective tariff rate from 23% to 25%. But with Chinese tariffs going to punitive rates, even conservative estimates of the price elasticity of imports would suggest that China’s share of imports should shrink dramatically, taking down China’s contribution to the increase in the total average effective tariffs.”

- There’s a solid line-up of Fedspeak after today’s CPI report where we expect a continuation of patient rhetoric after various speakers yesterday. We expect the most hawkish commentary to come from Schmid (’25 voter) on the economy and policy at 1000ET (text tbd, Q&A) followed by Logan (’26 voter) at 0930ET albeit in welcoming remarks.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: EURUSD fully clears 1.0900

- Nearly a 100 pips range for the EURUSD as it extends and gather momentum above 1.0900, and as already mentioned, next immediate resistance comes at 1.0937 High Nov 5 / 6 2024.

- Cable on the follow targets Yesterday's high of 1.2947 High Mar 10.

- Although the Yen is steady against the Dollar, the Japanese Yen extends some losses versus the EUR, GBP and AUD.

- Gold firms above $2900.00, now $2909.00, with the next area of interest coming at $2930.3, the 7th March high.

COMMODITIES: Gold in Consolidation Mode, Trend Remains Bullish

A bearish trend condition in WTI futures remains intact and last week’s fresh short-term cycle lows reinforce current conditions. Recent weakness has resulted in a clear breach of support at $70.20, the Feb 6 low. This confirmed a resumption of the downtrend that started Jan 15 and has paved the way for an extension towards $63.61 next, the Oct 10 ‘24 low. Key short-term pivot resistance is seen at $70.36, the 50-day EMA. Gold is in consolidation mode. The trend condition remains bullish and the recent pullback appears to have been a correction. A stronger rally would refocus attention on $2962.2, a Fibonacci projection. This would also open the $3000.0 handle. On the downside, a resumption of weakness would instead suggest scope for a deeper correction and expose support around the 50-day EMA, at $2826.3. The 50-day average marks a key support.

- WTI Crude up $0.21 or +0.32% at $66.24

- Natural Gas down $0.02 or -0.49% at $4.475

- Gold spot up $21.08 or +0.73% at $2909.91

- Copper up $1.15 or +0.25% at $467.7

- Silver up $0.3 or +0.93% at $32.4075

- Platinum up $5.5 or +0.57% at $968.07

EQUITIES: E-Mini S&P Sell-Off Monday Strengthens Bearish Conditions

The trend in the Eurostoxx 50 futures contract is unchanged, it remains bullish and the latest pullback appears corrective. Support at the 50-day EMA, at 5309.38, remains intact for now. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. However, a clear break of the 50-day EMA would signal a possible reversal. A resumption of gains would refocus attention on the 5600.00. A bear threat in S&P E-Minis remains present and Monday’s extension strengthens bearish conditions. The move down also reinforces the significance of the breach of 5809.00, the Jan 13 low. This level marked the mid-point of a double top on the daily chart and the break confirms the pattern and an important short-term reversal. Sights are on 5499.25, the Sep 9 2024 low. Firm resistance to watch is 5979.06, the 50-day EMA.

- Japan's NIKKEI closed lower by 235.16 pts or -0.64% at 36793.11 and the TOPIX ended 30.04 pts lower or -1.11% at 2670.72.

- Elsewhere, in China the SHANGHAI closed higher by 13.665 pts or +0.41% at 3379.828 and the HANG SENG ended 1.35 pts lower or -0.01% at 23782.14.

- Across Europe, Germany's DAX trades higher by 132.55 pts or +0.59% at 22753.92, FTSE 100 lower by 1.67 pts or -0.02% at 8598.11, CAC 40 up 44.61 pts or +0.55% at 8093.93 and Euro Stoxx 50 up 24.04 pts or +0.45% at 5411.97.

- Dow Jones mini up 143 pts or +0.34% at 42093, S&P 500 mini up 19.75 pts or +0.35% at 5641.75, NASDAQ mini up 89.75 pts or +0.46% at 19547.25.