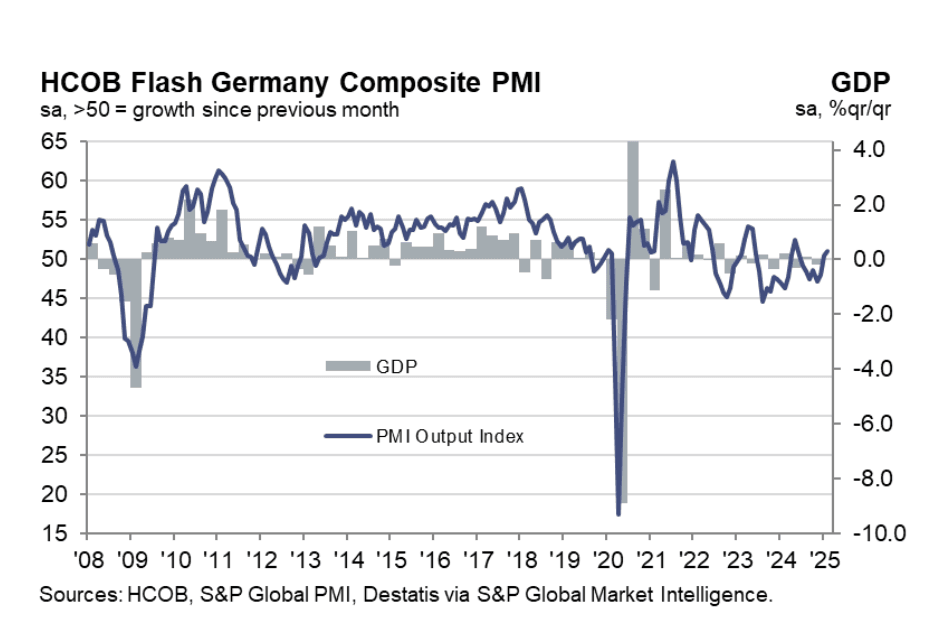

GERMAN DATA: Feb Flash PMIs

The German flash February manufacturing PMI was stronger-than-expected at 46.1 (vs 45.5 cons, 45.0 prior), reaching its highest level in two years. The index remains firmly stuck in contractionary territory though. The services index was a touch weaker-than-expected at 52.2 (vs 52.5 cons and prior), implying a small composite beat of 51.0 (vs 50.8 cons, 50.5 prior).

Divergences between services and manufacturing industries remain stark, however, from both an employment and inflation standpoint.

Key notes from the release:

- “Underlying demand for goods and services showed signs of stabilising at the midway point in the first quarter”… “sustained steady growth of services business activity midway through the first quarter coincided with a reduced drag from falling manufacturing production

- “Services firms reported a rise in workforce numbers for the second month running in February”….“However, the latest increase was only modest and offset by deeper job cuts in the manufacturing sector”.

- “Higher labour costs were a key factor behind a sustained sharp rise in services input prices in February”…“Combined with a quicker drop in manufacturing purchase prices, this led the overall rate of input cost inflation to retreat from January’s 22-month peak”.

- “The overall rate of output price inflation likewise ticked down from its recent high seen at the start of the year”….”The dichotomy between price rises in the service sector and discounting in manufacturing continued”

- “The degree of optimism was still the second-highest since July last year, but expectations moved back below the series long-run average as service providers and manufacturers alike reported less confidence towards the outlook than in the previous month. Concerns about tariffs and the general geopolitical backdrop were factors dampening sentiment”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: Spain 10-year Obli: Books open

- Guidance: 3.45% Oct-34 Obli (mid) +8bp area

- Size: EUR benchmark (MNI expects E10-15bln)

- Maturity: 30 April 2035

- Coupon: Short first

- ISIN: ES0000012O67

- Settlement: 29 January 2025 (T+5)

- Bookrunners: BBVA, CACIB, DB (B&D/DM), JPM, MS, SANTANDER

- Timing: Books open, today's business

From market source

BUNDS: BTP/Bund spread targets the December low

- French OAT and the BTP have been helping the German Bund back through its opening gap, small immediate resistance was seen at 132.14 Yesterday, and the contract printed a 132.15 high, this remains.

- Above that area, it opens to 132.41, but better is seen at 132.57.

- The price action is pushing the BTP/Bund spread towards 106.16bps, the December low, and tightest printed spread since October 2021.

(Chart source: MNI/Bloomberg):

EGBS: /SWAPS: Citi: Periphery Looks Attractive Vs Swaps

Citi note that “EGB supply pressure has likely peaked. There also seems little EGB supply indigestion so far. While these concerns remain, we find the overall risk-reward tilted supportive towards EMU periphery vs swaps.”

- They “especially like PGBs for this given we don’t expect the next syndication until April and today’s buyback absorbs some of the duration. This informed our recommendation last week to buy 20yr PGBs vs. swaps following the underperformance of the sector on the curve.”