US TSYS: Extending Highs as Trump Grants Mexico 90 Day Extension

Jul-31 15:22

- Treasury futures extend gains after Pres Trump's Mexico tariff 90 day extension tweet, see 1115ET bullet. Tsy Sep'25 10Y futures currently trades +10 at 111-10 (110-31 low, 111-10 high).

- Treasury futures faced resistance yesterday and pulled back from a key short-term hurdle at 111-14+, the high on Jul 22 and 30. A clear break of this level would highlight a stronger reversal and open 111-28, the Jul 3 high.

- Curves off flatter levels: 2s10s -1.495 at 41.033, 5s30s +0.145 at 93.501.

- Cross asset: Stocks paring gains (SPX eminis +14.75 at 6411.00), Gold at 3298.0, Bbg US$ index near steady at 1219.44 (+0.19).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

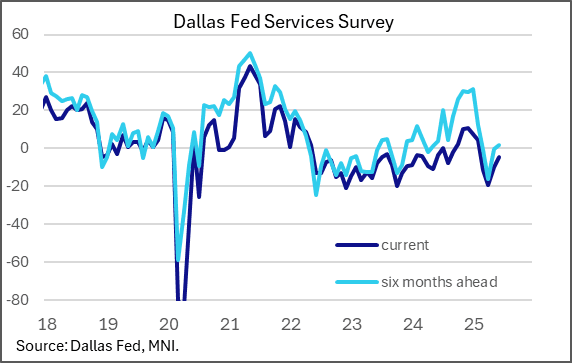

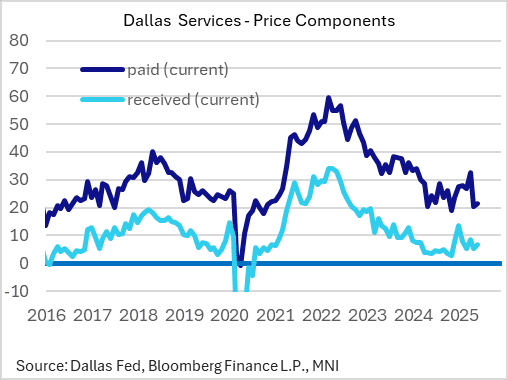

US DATA: Dallas Fed Services Activity Normalizing, Inflation Dynamics Tame

Jul-01 15:20

The Dallas Fed's Texas Service Sector Outlook Survey shows General Business Activity index rose to its best level in 5 months in June, -4.4 from -10.1 prior. That's still contractionary, but the 6-month ahead reading rose to 1.5 from -0.3, marking the first positive reading since February.

- The current reading is consistent with levels that prevailed through much of 2023-24, before volatility associated with the November 2024 elections through the tariff uncertainty that picked up strongly earlier in 2025. That said, the anecdotes to the report were almost universally negative, with several respondents citing elevated policy uncertainty and soft demand.

- Inflation didn't seem particularly pronounced. Prices paid ticked up to 21.3 from 20.5, though that's well below the average of 29 in the first 4 months of the year. Prices received also edged higher to 6.8 from 5.2 but still below the Jan-Apr average of 9.

- Highlights from the report: "Labor market measures indicated employment and hours worked were largely unchanged again in June. ... Perceptions of broader business conditions continued to worsen in June, though the indexes were less negative than the prior month.... The wages and benefits index remained largely unchanged"

- The retail sales index, a sub-category of the report, remained weak with the sales index at –29.5 vs –30.5 prior.

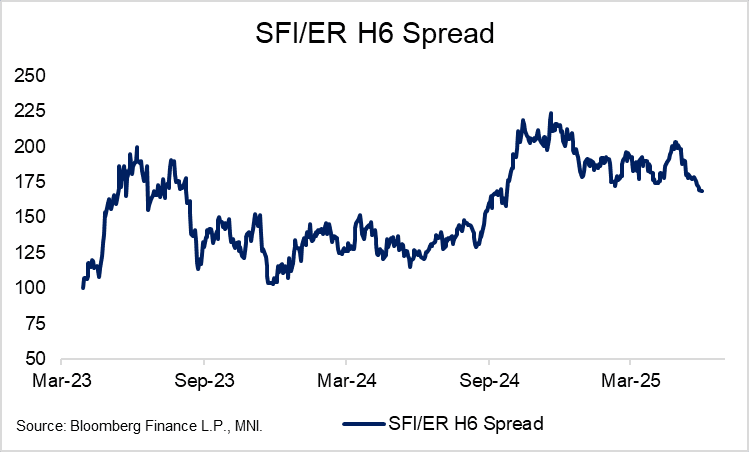

STIR: Lagarde Offers Little New At Sintra, SONIA/Euribor H6 Spread Near YTD Lows

Jul-01 15:18

- From a cross-market perspective, we note that the SONIA//Euribor H6 spread has consolidated below the March 11 closing low of 172.5bps over the past few sessions, currently trading at 169bps after closing above 200bps on May 30. The combination of a more cautious ECB stance and dovish BOE repricing drove movements in the spread through June.

- Looking ahead, markets probably need to see greater deterioration in the UK labour market/a swifter than expected moderation in inflation to be comfortable with discounting a meaningful deviation from the once per quarter cutting cycle that has become familiar in recent months.

- Meanwhile, the bar to significant near-term ECB repricing will likely hinge on any unexpected developments in the trade negotiations. The FT reported earlier today that "European capitals have hardened their position in trade talks with Donald Trump, insisting the US drops its tariffs on the EU immediately as part of any framework deal before the looming deadline on July 9". Such a stance could risk an inflammatory reaction from the President.

- President Lagarde offered little of note at today’s Sintra panel, re-iterating the ECB’s data-dependent approach and not elaborating on any questions pertaining to the exchange rate (now in more focus after VP de Guindos’ comments earlier this morning). As such, Euribor futures followed Treasuries lower through the panel, in response to some dovish leaning (or at least, non-committal) comments from Fed Chair Powell – see more above. Futures are flat to +2.5 ticks through the blues, while trendline resistance in the U5/U6 spread remains unchallenged.

- Tomorrow's regional calendar includes unemployment data from Spain, Italy and the Eurozone, though these aren't usually market moving releases.

STIR: BoE Pricing Steady Around 55bp Cuts Through Dec

Jul-01 15:05

GBP STIRs have pulled away from dovish session extremes given the adjustment in Fed pricing after the U.S. data.

- SONIA futures flat to +5.5, with the strip bull flattening.

- SFIZ5 & Z6 pierced respective May 9 & May 8 high before a retrace. Bulls will now look to target wider May highs in those contracts.

- BoE-dated OIS hasn’t been able to push consistently beyond 55bp of cuts through year-end, with markets probably needing to see greater deterioration in the labour market/a swifter than expected moderation in inflation to be comfortable with discounting a meaningful deviation from the once per quarter cutting cycle that has become familiar in recent months.

- Comments from BoE dovish dissenter Taylor are due tomorrow.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.005 | -21.3 |

Sep-25 | 3.931 | -28.6 |

Nov-25 | 3.758 | -46.0 |

Dec-25 | 3.665 | -55.2 |

Feb-26 | 3.531 | -68.7 |

Mar-26 | 3.495 | -72.2 |