US TSYS: Extending Highs

Jul-18 13:10

- Treasuries extending highs again, no particular headline driver, with the next data event - UofM sentiment/inflation expectations an hour away.

- Sep'25 10Y futures currently +11.5 at 110-28 vs. early Tuesday high of 110-30.

- Initial resistance is at 111-30.5, the 20-day EMA, followed by 111-13.5/111-28 (High Jul 10 / High Jul 3).

- Curves gaining: 2s10s +1.383 at 55.652, 5s30s +1.739 at 103.420 (after surging to Oct 2021 high of 107.895 midday Wednesday).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

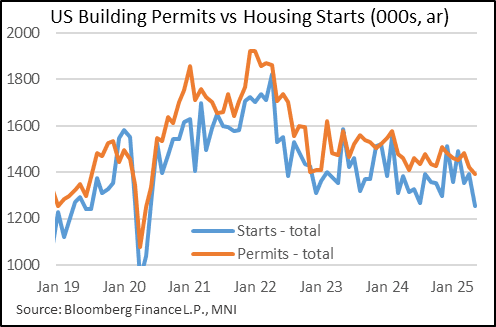

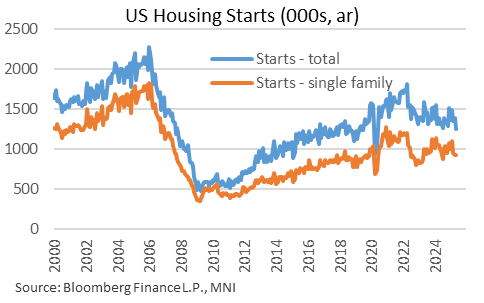

US DATA: Housing Activity Showing Increasing Signs Of Deterioration

Jun-18 13:06

May's New Residential Construction report was very weak, portending very negative current conditions for residential investment activity, as well as a dim outlook for the quarters ahead.

- Housing starts fell to the lowest level since July 2019 (seasonally adjusted) excluding the sudden stop in 2020's pandemic, with a 9.8% M/M decline bringing the seasonally-adjusted annual rate of starts to 1,256k in May (vs 1,350k expected, 1,392k prior rev from 1,361k).

- Permits at 1,393k also disappointed vs expectations of a steady reading vs April at 1,422k and also hit the ex-pandemic lowest since July 2019.

- Weakness was seen across the board: single family permits fell 2.7% (4th fall in 5 months) to a 25-month low 898k, with multi-unit permits down 0.8% (7th fall in 9 months). Starts, which lag permits, saw single-family activity actually pick up slightly (0.4%, but only after falls in 3 of the prior 4 months) to 924k, but multi-units fall almost 30% to 332k.

- Starts are now down 4.6% Y/Y with permits down 1.0% Y/Y.

- New homes continue to sell, but combined with June's very poor NAHB survey - which tends to lead single-family starts/permits - the housing market is due to weaken significantly this year after 2024's residential investment bounce.

- The recent downward pressure in prices is set to accelerate too, albeit against the backdrop of very limited sales volumes as existing homeowners stay put (that said, inventories-to-sales have clearly picked up). New home sales are fairly robust though as we learned in the NAHB survey, that may be because discounting is picking up sharply.

- There is likely no relief in sight absent a pullback in mortgage rates, with homebuilders' responses to supply-side reform (eg regulation) probably paling in importance.

- Permits are a leading indicator for starts but there is a bit more of a gap than usual building between the two - we wonder if there is some combination of factors here restraining starts, including uncertainty over government policy, "surprisingly" elevated interest rates, and immigration policy shifts (which were noted in the Fed's latest Beige Book as a constraint on construction companies).

STIR: Effective Fed Funds Rate

Jun-18 13:04

- FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $104B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $285B

- Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.31% (-0.01), volume: $2.692T

- Broad General Collateral Rate (BGCR): 4.29% (-0.01), volume: $1.087T

- Tri-Party General Collateral Rate (TCR): 4.29% (-0.01), volume: $1.063T

- (rate, volume levels reflect prior session)

STIR: Fed Pricing Little Changed Over Data, Under 50bp Of Cuts Through Dec

Jun-18 12:59

Fed Funds little changed on net over the 08:30 NY data, with much softer-than-expected housing market data and a roughly inline round of jobless claims readings having no lasting impact.

- Geopolitical risk and related spot inflation pressure remains front of mind for markets, negating any impact from the soft housing readings.

- Note that continuing claims data still signals a softening labour market.

- 0bp of easing priced for today’s Fed decision, 3.5bp showing through July, 18bp through September, 29.5bp through October & 46bp through year-end.

- SOFR futures also see limited reaction.

- The FOMC will hold rates for a 4th consecutive meeting today and continue to convey a patient stance on future rate cut decisions amid elevated government policy-related uncertainty.

- The new quarterly projections will still signal the resumption of rate cuts later this year, but likely only one 25bp reduction instead of the two cuts envisaged at the March meeting.

- Click for our full preview.