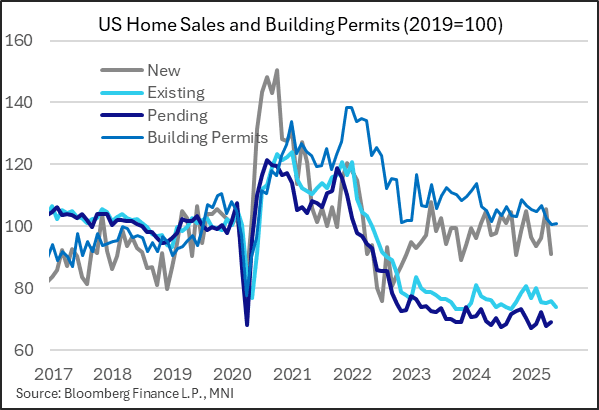

US DATA: Existing Home Sales Weaken, Rising Inventories To Pressure Prices

Existing home sales fell more than expected in June, to 3.93M (seasonally-adjusted annualized rate), vs 4.00M expected and 4.04M in May (upwardly revised by 10k). That's a 9-month low, breaking an 8-month streak of sales above 4 million.

- This is about 25% below the level of sales pre-pandemic (2019), and 40% below the level seen at the height of the pandemic frenzy in 2020-21. Sales dropped in 3 of four regions (sales in the West grew slightly), with all 4 below end-2024 levels.

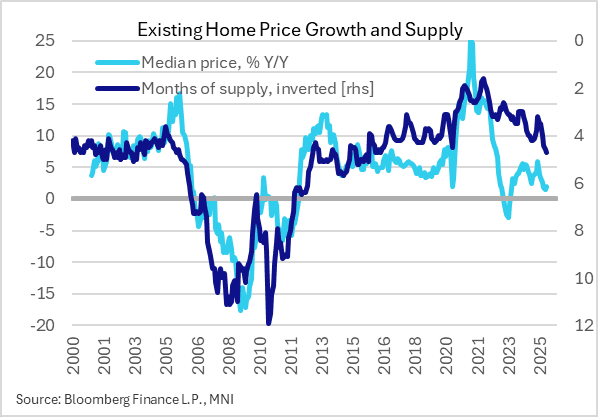

- The lack of activity hasn't dampened selling prices: median prices rose 2.0% Y/Y to an all-time high $435.3k (non-seasonally adjusted). While June tends to bring the highest prices of the year, the Y/Y change reflects continued price resilience.

- Even so, the market is beginning to loosen in at least one regard: with inventory remaining above 1.5M (1.53M) and sales at 391k in June (non-seasonally adjusted), the implied number of months of supply rose to 4.7, the highest since 2016. A similar rise is being seen in new home inventories. Amid continued affordability issues with mortgage rates high, it's likely that downside pressures on prices will increase.

- Against this backdrop, residential investment is likely to remain moribund through the rest of 2025.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Large Sep'25 5Y Sale

- -14,000 FVU5 108-16.75, sell through 108-17.5 post time bid at 1021:38ET, DV01 $610,000.

- The 5Y contract trades 108-16.5 last (+8.25)

FED: VC Bowman Eyes July Cut Amid Inflation Progress, Labor Market "Fragility"

Fed Vice Chair Bowman, one of the most hawkish FOMC members coming into the year (and a permanent voter), appears to now be on the most dovish end of the spectrum in suggesting she conditionally would support a rate cut as soon as the next meeting in July. This doesn't appear to be a widely shared view on the Committee (only expressed by Gov Waller so far) but it is a jarring shift in view.

- The last time we heard from her on current monetary policy was between the January and March meetings. At that time, she said she didn't think the Fed funds rate was "exerting meaningful restraint" (it hasn't changed since then at 4.25-4.50%) and had dissented against the 50bp cut to start the cycle in September, though in fairness even in late January she had seen inflation would be beginning to decline by year-end.

- In short, while she now argues "we have not seen significant economic impacts from trade developments or other factors" with a labor market remaining "solid", she also sees growth "slowing" with it "possible" that this is translating into weaker labor market conditions. And overall, she appears very optimistic on the trajectory of inflation, that while she recognizes upside risks she is "not yet seeing a major concern" over tariffs and has seen a pickup in core PCE goods "more than offset by a considerable slowing in core PCE services inflation".

- In short, "With inflation on a sustained trajectory toward 2 percent, softness in aggregate demand, and signs of fragility in the labor market, I think that we should put more weight on downside risks to our employment mandate going forward."

- She says that "If inflation remains near its current level or continues to move closer to our target, or if the data show signs of weakening in labor market conditions, it would be appropriate to consider lowering the policy rate, moving it closer to a neutral setting."

- "the data have not shown clear signs of material impacts from tariffs and other policies. I think it is likely that the impact of tariffs on inflation may take longer, be more delayed, and have a smaller effect than initially expected...we should recognize that inflation appears to be on a sustained path toward 2 percent and that there will likely be only minimal impacts on overall core PCE inflation from changes to trade policy."

- In sum: "Before our next meeting in July, we will have received one additional month of employment and inflation data. If upcoming data show inflation continuing to evolve favorably, with upward pressures remaining limited to goods prices, or if we see signs that softer spending is spilling over into weaker labor market conditions, such developments should be addressed in our policy discussions and reflected in our deliberations. Should inflation pressures remain contained, I would support lowering the policy rate as soon as our next meeting in order to bring it closer to its neutral setting and to sustain a healthy labor market. In the meantime, I will continue to carefully monitor economic conditions as the Administration's policies, the economy, and financial markets continue to evolve."

SLOVAKIA: PM Fico Backs Spanish Stance On NATO Defence Spending

Reuters reports comments from Prime Minister Robert Fico regarding the upcoming NATO summit. Fico says that "Slovakia, like Spain, must reserve the right to decide on the pace and structure of the increase in defence spending towards the [new] NATO target." He adds that any increase in 2026 defence spending above 2025 levels will go towards dual-use purposes such as infrastructure.

- While the NATO members have seemingly agreed on Secretary General Mark Rutte's '3.5%+1.5%' plan (3.5% of GDP equivalent going on frontline spending, 1.5% on defence-related expenses such as infrastructure or cybersecurity) to allow countries to hit US President Donald Trump's demand of 5% of GDP going on defence, there are disagreements. Spanish PM Pedro Sanchez has argued that the 5% target is too high, and would threaten his gov'ts ability to make welfare payments without raising taxes.

- Fico has recently raised hackles domestically with comments apparently advocating Slovakian neutrality (see 'SLOVAKIA: Gov't & Oppo. Politicians Criticise Fico's 'Neutrality' Comments', 18 June), although the parties forming his governing coalition were not due to oppose the 5% NATO target.

- The PM's increasingly NATO-sceptic statements will cause concern in Brussels and among NATO allies, given that as a state bordering Ukraine, Slovakia remains a crucial partner for the alliance.