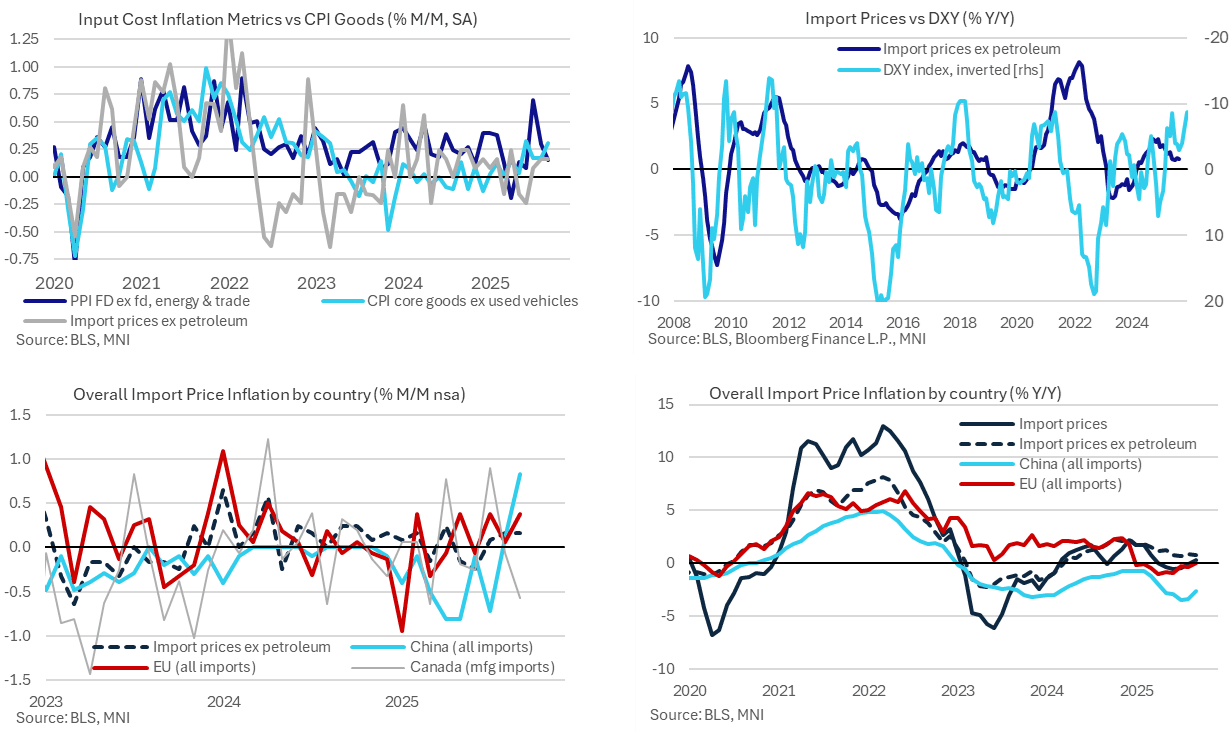

US DATA: Ex-Oil Import Price Inflation Returns To More Typical Pace In Q3

Dec-03 14:12

Headline import price inflation was softer than expected in September but our preferred ex-petroleum metric was on balance stronger and showed a return of continuation of more typical increases in Q3 after tariff-driven concessions in 1H25.

- Import prices inflation was softer than expected at 0.0% M/M (cons 0.1) in the shutdown-delayed September report. It also saw a downward revised 0.1% M/M in Aug vs an initial 0.3% but this was offset by upward revisions to Jul and Jun.

- More importantly, import prices ex petroleum increased a slightly stronger than expected 0.2% M/M (cons 0.1) after an unrevised 0.2% in Aug and upward revised 0.1% in Jul.

- It sees a return of somewhat more typical ex-oil import price inflation in Q3 after softer run rates in 1H25 were seen as foreign producers/exporters took some of the tariff burden (a reminder than import price data doesn’t include tariffs). Specifically, 1H25 saw average import price inflation of 0.0% M/M after 0.2% M/M through 2024.

- Annual ex-oil import price inflation held within recent ranges meanwhile, at 0.8% Y/Y having been between 0.7-0.9% since June at its softest since May 2024.

- The country-level data for key trading partners, which are generally on an all import price basis, reveal mixed latest trends along with some sizeable downward revisions specifically to August.

- In particular, import prices from China increased 0.8% M/M in September, a strong rise albeit after a large downward revision to 0.1% M/M in Aug vs the 0.6% initially reported. Bearing in mind the scope for similarly sized revisions ahead, it currently shows a marked uptick from the -0.5% M/M averaged through Jan-Jul. For context, Chinese import price inflation averaged -0.1% M/M in 2024.

- Elsewhere, Canada saw the other more notable development, with manufactured import prices -0.6% M/M (to avoid the impacts from a large decline in oil prices) for their weakest since March on the initial escalation in US-Canada trade tensions. The data are volatile however.

- In trend terms, China import prices are -2.6% Y/Y, EU 0.1% Y/Y, Canada manufactured -0.2% Y/Y and Mexico manufactured 2.3% Y/Y.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: ISM Mfg New Orders May Have Bounced From Sept Decline [2/2]

Nov-03 14:08

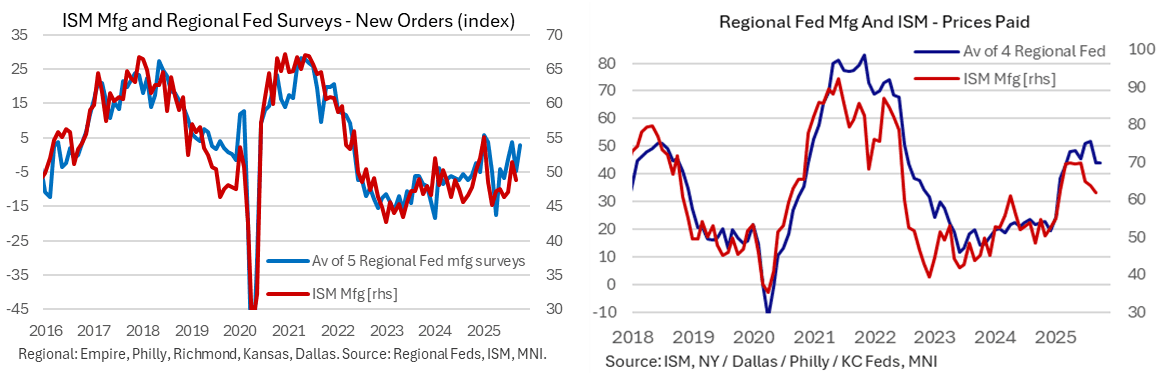

- Within the ISM manufacturing details, the new orders index looks set to have seen a reasonable improvement judging by the regional Fed surveys, reversing a large part of its drop from 51.4 to 48.9 in last month’s release.

- That’s supported by the MNI Chicago PMI new orders index seeing a strong increase to unwind the majority of what was also a large decline in September. It marked the first gain in the index since July.

- Bloomberg consensus sees the price index nudge up from 61.9 to 62.5. It’s from a typically limited survey of six analyst estimates but looks reasonable looking at the regional Fed surveys, which on average were little changed on the month but continue to run at higher levels – see chart.

- We tend not to focus on the employment index as much in the manufacturing survey, with manufacturing being only about 10% of payrolls, but it will nevertheless receive some interest after improving in September but only to 45.3.

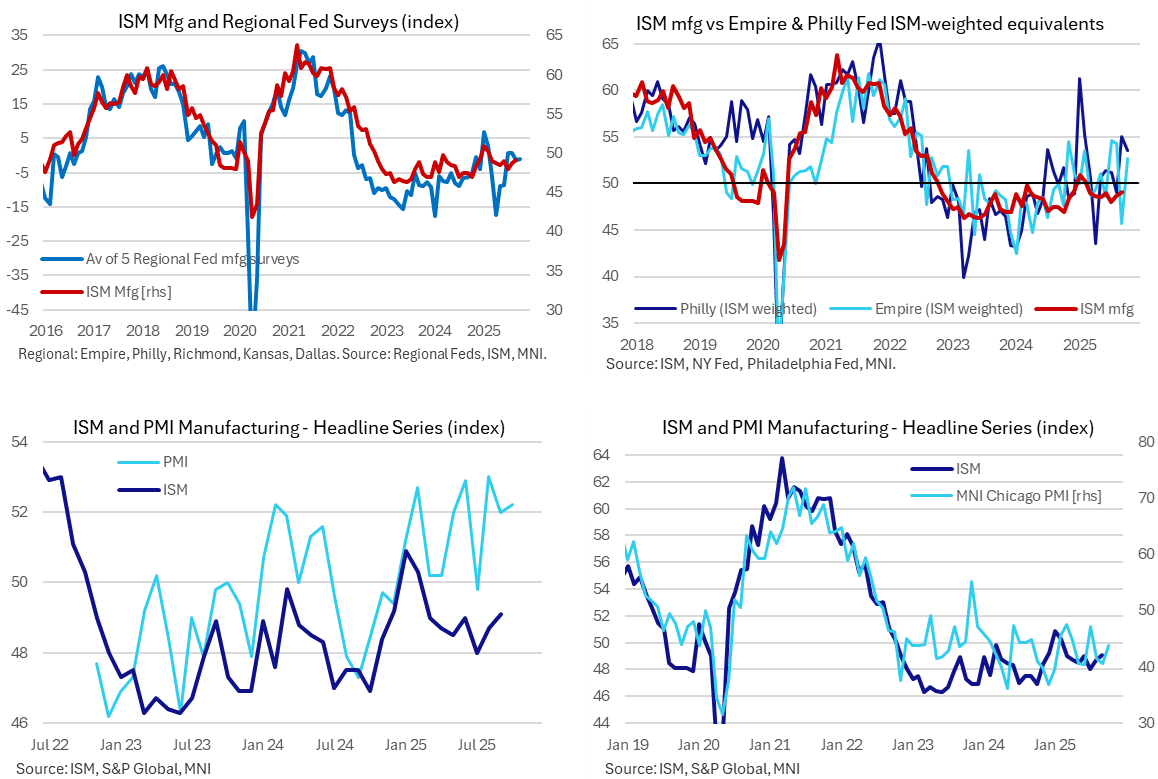

US OUTLOOK/OPINION: Scope For Small Beat For ISM Mfg [1/2]

Nov-03 14:07

- Bloomberg consensus looks for a minor increase in the ISM manufacturing index from 49.1 to 49.5 in October, for what would be a third consecutive increase and its highest since February.

- We suspect risks are to a slightly larger increase but don’t wish to overemphasize the possible magnitude. An unweighted average of five regional Fed surveys may be consistent with little change but both the Empire and Philly Fed surveys are stronger on an ISM-weighted basis (52.7 after 45.7 and 53.5 after 55.0 respectively).

- We’d caution placing too much weight on the more optimistic manufacturing PMI reading however, at 52.2 in the October flash (final due today at 0945ET) after 52.0.

- Rounding out the other main monthly manufacturing indicators, the MNI Chicago PMI also firmed to 43.8 from what was a notably low 40.6 in September, although has seen wide ranges so far this year of 39.5 to 47.6.

FRANCE T-BILL AUCTION RESULTS: 13/26/28/52-week BTFs

Nov-03 13:56

| Type | 13-week BTF | 26-week BTF | 28-week BTF | 52-week BTF |

| Maturity | Feb 4, 2026 | May 6, 2026 | May 20, 2026 | Nov 4, 2026 |

| Amount | E3.2bln | E497mln | E1.799bln | E2.1bln |

| Target | E2.8-3.2bln | E0.1-0.5bln | E1.4-1.8bln | E1.7-2.1bln |

| Previous | E3.3bln | E360mln | E1.798bln | |

| Avg yield | 2.010% | 2.029% | 2.050% | 2.059% |

| Previous | 2.011% | 2.015% | 2.029% | 2.053% |

| Bid-to-cover | 3.23x | 5.51x | 2.77x | 3.15x |

| Previous | 2.41x | 4.33x | 5.51x | 3.02x |

| Previous date | Oct 27, 2025 | Oct 27, 2025 | Nov 03, 2025 | Oct 27, 2025 |