LOOK AHEAD: Eurozone Timeline of Key Events (Times BST)

Apr-24 05:18

---------------------------------------------------------------------- Date Time Country Eve...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

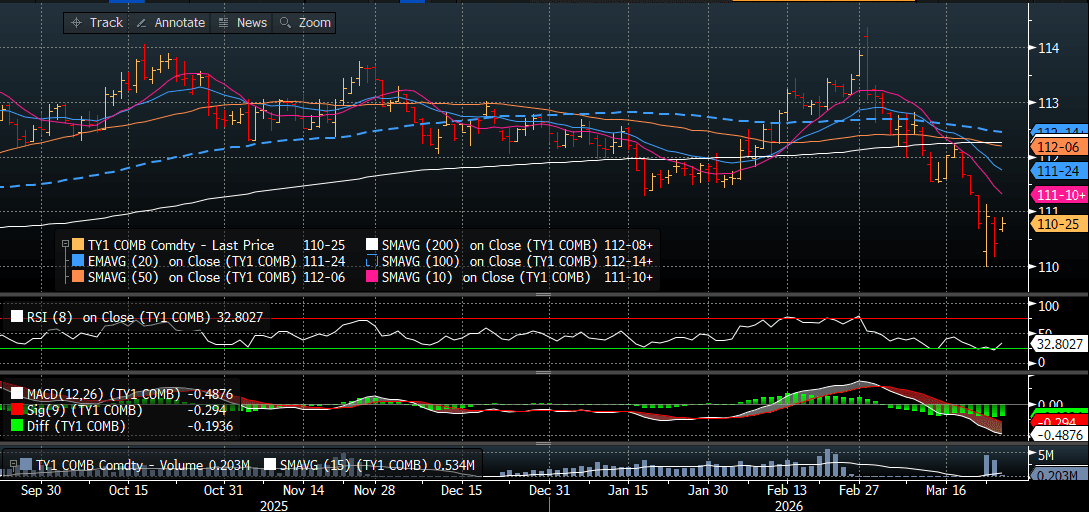

US TSYS: US's Diplomatic Push To End Middle East Conflict Buoys Mkt

Mar-25 05:07

TYM6 is dealing at 110-25+, +0-12 from closing levels in today's Asia-Pac session

- The market has been buoyed by optimism around Washington's diplomatic push to resolve the Middle East conflict. Cash US tsys are 2-4bps richer in today's Asia-Pac session.

- The US has drafted a 15-point plan intended to help bring the war with Iran to a close, according to people familiar with the matter. - BBG

- However, The Spectator Index on X: "Iran has demanded closure of US bases in the Gulf, end of all sanctions, end of Israeli campaign against Hezbollah and a framework that would allow it to collect fees from ships transiting through the Strait of Hormuz, as part of a response to Trump proposal, according to Wall Street Journal report."

- (Bloomberg) Citi Wealth sees opportunities in shorter-dated US Treasuries as the Iran war deepens inflation concerns and spurs bets on higher interest rates. “We believe this sharp repricing looks excessive without clear evidence that higher energy prices will feed through to underlying inflation,” chief investment officer Kate Moore and others write in a report.

Source: Bloomberg Finance LP

JGBS: Twist-Flattener As Geopol Optimism Strengthens

Mar-25 04:48

At the Tokyo lunch break, JGB futures are stronger, +10 compared to settlement levels.

- The market has been buoyed by optimism around Washington's diplomatic push to resolve the Middle East conflict. Cash US tsys are 2-4bps richer in today's Asia-Pac session.

- The US has drafted a 15-point plan intended to help bring the war with Iran to a close, according to people familiar with the matter. – BBG

- However, The Spectator Index on X: "Iran has demanded closure of US bases in the Gulf, end of all sanctions, end of Israeli campaign against Hezbollah and a framework that would allow it to collect fees from ships transiting through the Strait of Hormuz, as part of a response to Trump proposal, according to Wall Street Journal report."

- MNI: BOJ Minutes: Neutral Rate Difficult To Assess. Most Bank of Japan board members agreed the neutral rate remains difficult to identify in advance, underscoring the need to gauge it gradually by assessing the impact of each rate hike on economic activity and prices, minutes of the Jan 22-23 meeting showed Wednesday.

- Cash JGBs have twist-flattened across benchmarks, with yields 1bp higher to 4.5bps lower.

- Tomorrow, the local calendar will see PPI Services and Investments Flow data alongside Enhanced-Liquidity Auction 1-5 YR.

Source: Bloomberg Finance LP

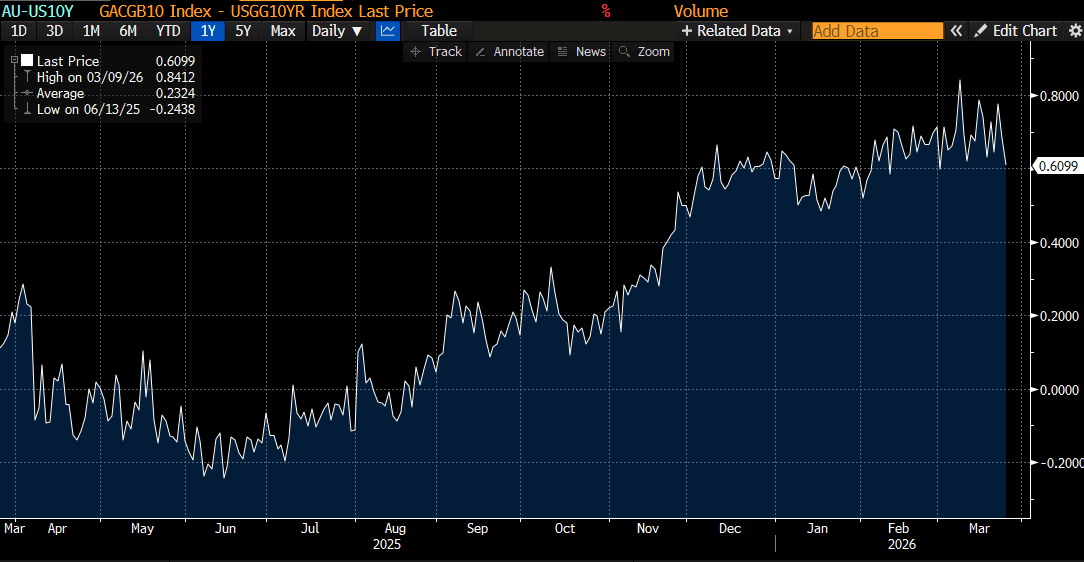

AUSSIE BONDS: Strong Rally On US's Push To End Middle East Conflict

Mar-25 04:26

ACGBs (YM +11.5 & XM +9.5) are sharply stronger but a tad off session bests.

- Inflation pressures appear to have stabilised before fuel prices jumped in response to supply fears following the closure of the Strait of Hormuz. February CPI inflation was slightly lower than expected with headline at 3.7% y/y after 3.8% and trimmed mean 3.3% y/y following a downwardly revised 3.3%, and around the rate seen since October.

- We won't get a feel for any second-round effects from higher fuel prices until March CPI (29 April) at the earliest, but the March PMI showed increased cost pressures being partially passed on.

- Cash US tsys are 2-3bps richer in today’s Asia-Pac session following Washington's diplomatic push to resolve the Middle East conflict.

- Cash ACGBs are 9-12bps richer with the AU-US 10-year yield differential at +61bps, the lowest since early March.

- The bills strip has bull-flattened, with pricing +9 to +16 across contracts.

- RBA-dated OIS pricing is softer today but continues to show tightening across all meetings, with the probability of a 25bp hike rising from 59% for May to 148% by August and 223% by December 2026.

- Tomorrow, the local calendar will see a speech from RBA Kent at the KangaNews Debt Capital Market Summit.

Bloomberg Finance LP

Related bullets

Related by topic

European Central Bank

Schatz

Germany

Bobl

Bunds

France

Spain

Italy

Trending Top

Apr-24 05:45