EUROPEAN FISCAL: France Sees Higher Net M-T/L-T Debt Issuance In 2025

Oct-10 18:56

AFT (French Treasury) Issues the following regarding state funding for 2025 (with an update for 2024), reflecting the French Budget Bill for 2025 which was presented to the Council of Ministers today. Judging from the modest move higher in OAT futures (22 ticks to 125.95 high), the announcement overall was in line with expectations and relieves some uncertainty over the fiscal situation.

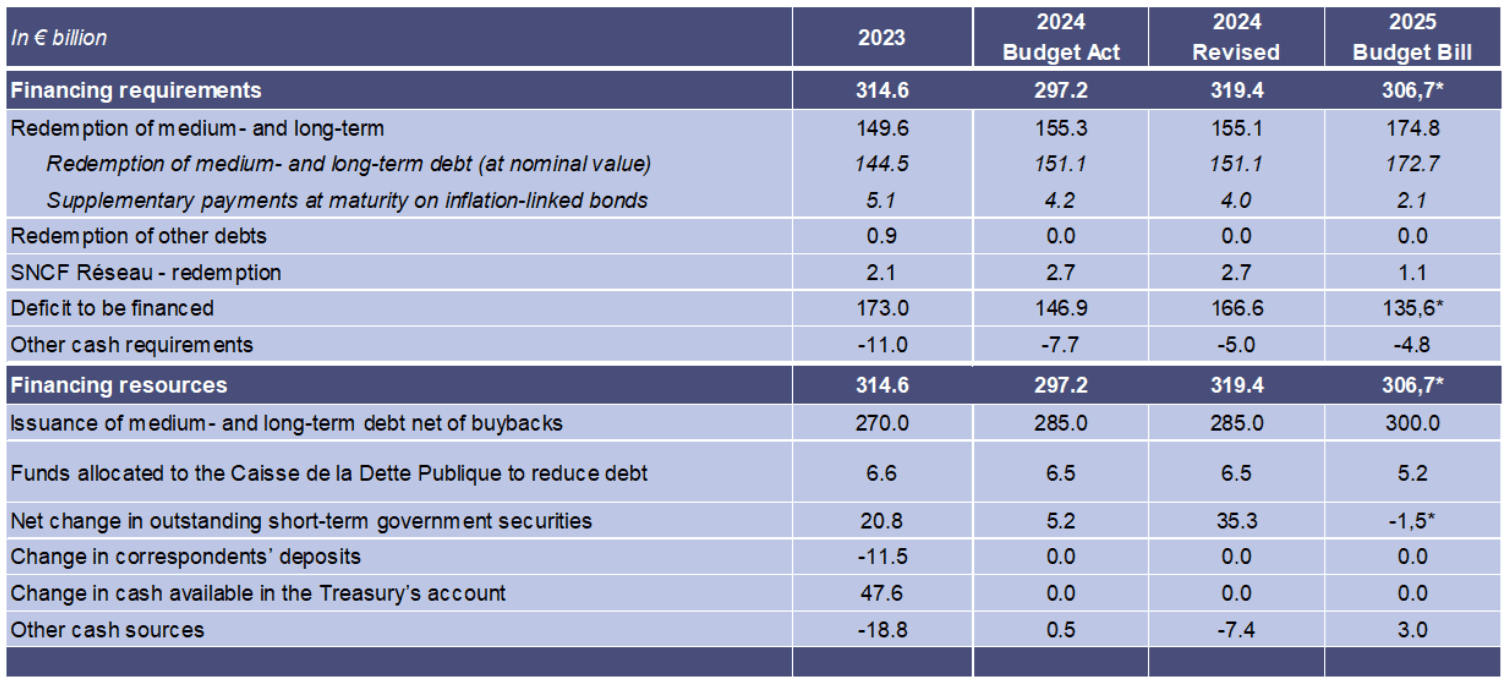

- In sum, France's financing needs are set to total E307B in 2025, compared with E319B in 2024, with E41.3B in spending cuts vs E19.3B tax hikes in 2025 as part of the Government's effort to get the deficit below 5% of GDP. See AFT table graphic below.

- The 2024 deficit financing requirement was upped nearly E20bln to E166.6B vs the initial budget set last December. BTFs outstanding will amount to E35.3B, vs E5.2B initially planned, though issuance of M-T/L-T debt net of buybacks remains unchanged at E285B.

- For 2025, the total financing requirement is down nearly E13B vs the 2024 updated financing requirement, to E306.7B - reflecting both a E31B lower deficit projection and just under E20B increase in M-T/L-T debt redemptions. 2025 M-T/L-T issuance (net of buybacks) is upped E15B to E300B vs 2024, with the 2024 increase in bills partially reversing (net negative E1.5B vs E35B seen in the 2024 revised budget).

- Official link here for full details from AFT

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Analysts Expect Large Reversal Of Primary Rents Jump

Sep-10 18:48

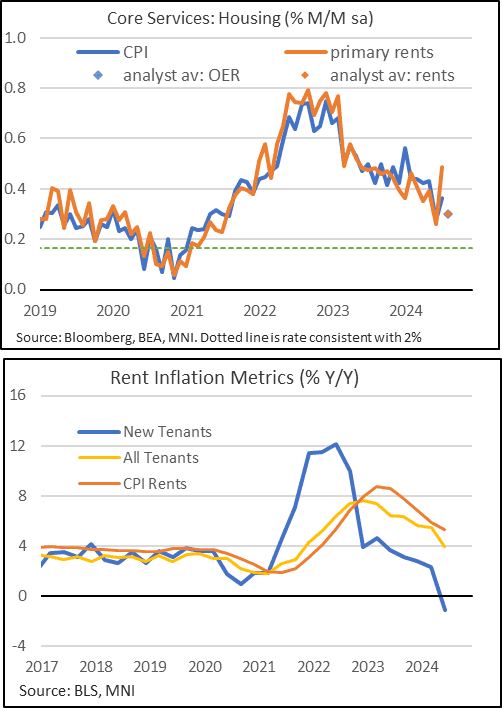

- Rent inflation was much stronger than expected back in July as primary rents in particular surged 0.49% M/M vs analysts clustered around a ‘mid-to-high’ rounded 0.3% reading.

- Primary rents inflation has been volatile in recent months, with that 0.49 in July after 0.26 in June, following what was a relatively consistent 0.40% averaged through Jan-May.

- The 0.30% broadly expected this month likely incorporates some reversal of a particularly strong increase in primary rents in the West although as we showed in last month’s MNI Inflation Insight this could also have been seen as payback for what had been soft monthly increases relative to other major regions.

- If realized, a 0.30% M/M print would likely be seen as continuation of a bumpy but moderating trend in rental inflation, although we feel risks of a surprise are skewed to the upside this month.

- Putting these monthly rates into context and the progress that the FOMC needs to see, weighted OER and primary inflation saw a weighted average of 0.27% M/M pre-pandemic. We have only had one month meet that rate over recent years (June, with 0.27% as well). It re-accelerated to 0.39% M/M although the 0.30% broadly expected for August would come close to this.

- Experimental data from the BLS’s New Tenants Rent index has slowed to -1.1% Y/Y for Q2 but we again stress it is particularly prone to revisions and latest quarters have tended to be revised up (Q1 is currently seen at 2.3% vs its first released 0.4%, Q4 is currently seen at 2.8% vs 0.9% and before that -4.7%).

PIPELINE: $22.05B High Grade Corporate Debt to Price Tuesday

Sep-10 18:45

Still waiting for $800M Wynn Resorts and Provence of Ontario to launch, however:

- Date $MM Issuer (Priced *, Launch #)

- 9/10 $7B #Oneok $1.25B 3Y +80, $600M 5Y +100, $1.25B 7Y +130, $1.6B 10Y +145, $1.5B 30Y +175, $800M 40Y +190

- 9/10 $2B #Bunge Ltd Finance $400M +3Y +65, $800M 5Y +80, $800M 10Y +105

- 9/10 $2B *IADB 7Y SOFR+52

- 9/10 $2B *AfDB 5Y SOFR+41

- 9/10 $1.25B #APA Infrastructure $750M 10Y +165, $500M 20Y +182

- 9/10 $1.25B #Helmerich & Payne $350M 3Y +120, $350M 5Y +145, $550M 10Y +190

- 9/10 $1B #Nissan Motor Acceptance Co $400M 3Y +185, $300M 3Y SOFR+205, 400M $5Y +215

- 9/10 $1B #CK Hutchinson $500M 5.5Y +95, $500M 10Y +115

- 9/10 $1B *Kommuninvest WNG 2027 SOFR+36

- 9/10 $1B *Blue Owl Credit +5Y +260

- 9/10 $800M Wynn Resorts 8.5NC3

- 9/10 $750M *IDB Invest +2Y SOFR+35

- 9/10 $500M #MassMutual 7Y +85

- 9/10 $500M #Macquarie Airfinance 5.5Y +172

- 9/10 $Benchmark Provence of Ontario 5Y SOFR+57

COMMODITIES: Crude Lowest Since Dec 2021, Spot Gold Consolidates

Sep-10 18:41

- WTI is headed for its lowest close since December 2021 as the market’s bearish feel grows. A slight downward revision of demand growth from OPEC, coupled with continued weakness from the USA and China maintain price pressure.

- WTI Oct 24 is down 4.2% at $65.8/bbl.

- OPEC lowered its demand growth to 2.0m b/d for 2024, down 80k b/d compared to last month’s assessment, according to their August MOMR.

- WTI futures remain in a bearish condition, having pierced key support at $66.66. Next support is at $65.30 - 1.50 projection of the Apr 12 - Jun 4 - Jul 5 price swing.

- In contrast, spot gold has edged up by 0.4% to $2,516/oz today, as the yellow metal remains close to last month’s record high, ahead of key US CPI data tomorrow.

- Gold is in consolidation mode, although the trend condition is unchanged and the primary direction remains up, with sights on $2,536.4 next, a Fibonacci projection.

- Meanwhile, copper has fallen by 1% to $410/lb.

- Chile’s copper commission Cochilco today lowered its copper price forecast for this year to average $4.18/lb, from $4.30 previously, amidst a weaker demand outlook.

- A bear cycle in copper futures remains intact, with initial support seen at $396.45, the Aug 7 low. On the upside, a clear break of the 50-EMA at $423.34 would signal scope for stronger gains.