HUF: EURHUF Targets Close Above Key Resistance Level on Orban Presidency Report

Dec-11 12:34

- The prospect of an Orban presidency has prompted a solid spike for FX implied vols, but HUF FRAs have reacted only marginally to the report – suggesting that convictive market positioning in the base rate being left at 6.50% in the near future remains unchanged. Meanwhile, the 25-delta EURHUF vol skew shifted further in favour of calls on the back of the report, albeit briefly and moderately, indicating that option markets are hedging against the risk of further HUF weakness ahead.

- EURHUF remains close to session highs, up around 0.6% at typing, with the cross not far off key resistance at 385.801, the 50-day EMA. This level has provided solid resistance since June, with a number of tests of the average over the past 6 months subsequently followed by a failure to close above it. Note too that trendline resistance intersects just ~0.5% above current levels at 386.46 (see chart below). Yields on HUF bonds have risen 2-5bps across the curve, with the 10-year yield now up 10bps compared to the week’s lows.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

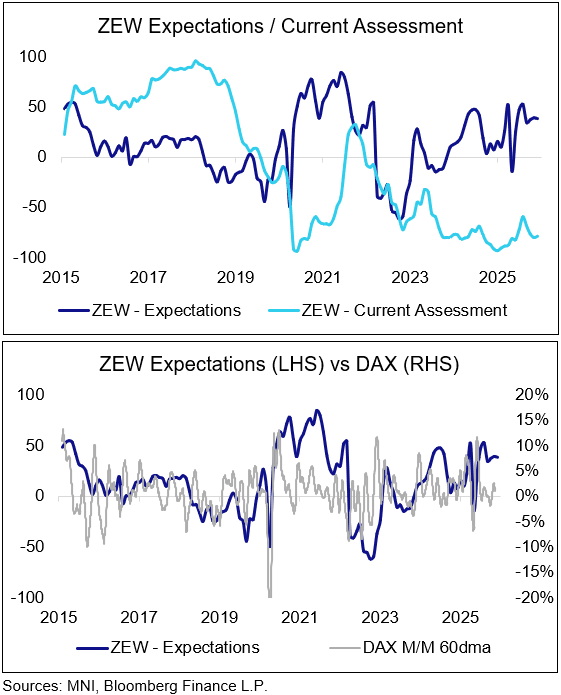

GERMAN DATA: ZEW Underperforms In Both Expectations And Current Conditions

Nov-11 12:33

The November German ZEW survey’s expectations component was weaker-than-expected at 38.5 (vs 41.0 cons), also falling versus October's 39.3 reading. The ZEW has historically been sensitive to prior M/M stock market moves, though this signal appears to have lost some power in recent months.

- The current conditions component meanwhile was also weaker-than-expected at -78.7 in November (vs -74.2 cons, -80.0 prior), down from a cycle high of -59.5 in July.

- The ZEW mirrors the German IFO in that expectations seem to not filter through to a) current assessment readings and b) hard data for now.

- "186 analysts participated in the November-survey which was conducted during the period 3.11.2025 - 10.11.2025"

- A reminder that the ZEW index is based on a survey of "experts from banks, insurance companies and financial departments of selected corporations [which] have been interviewed about their assessments and forecasts for important international financial market data". It can exhibit elevated levels of correlation with German stock indices such as the DAX.

OUTLOOK: Price Signal Summary - Recovery In Gilts Exposes The Bull Trigger

Nov-11 12:24

- In the FI space, a short-term bear cycle in Bund futures remains intact and Monday’s fresh short-term cycle low reinforces current conditions. The latest move down undermines a recent bull theme and the contract has cleared a number of important support points; the 50-day EMA, at 129.14, and 128.92, the 61.8% retracement of the Sep 25 - Oct 17 bull leg. Sights are on 128.52, the 76.4% retracement. Resistance is at 129.31, the 20-day EMA. The trend structure in

- Gilt futures remain bullish and a recent shallow correction reinforces this theme - for now. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Support to watch lies at 92.98, the 20-day EMA. It has been pierced, a clear break of it would signal scope for a deeper correction and allow a recent overbought trend condition to unwind. Support at the 50-day EMA lies at 92.26. The bull trigger is 93.98, the Nov 4 high.

UK FISCAL: BOE estimated APF programmes lowered issuance costs by GBP50-125bln

Nov-11 12:21

- The BOE has estimated that the APF programme has lowered issuance costs by GBP50-125bln in NPV terms, with "only about half of this benefit realised to date, given the UK's long debt maturity structure."

- There are a number of assumptions going into this on where yields would otherwise have been (and always where interest rates will end up in the future and the pace of future APF rundown). But the purpose of this exercise is not really to give the gilt market any additional clarity or even to help with any Budget calculations. It is more to head off increasing political pressure that the Treasury should not be indemnifying the BOE's APF holdings and to reduce the political pressure that has been building as instead of the Treasury receiving a quarterly payment from the BOE, it is now making a quarterly payment (which is quite substantial). Reform UK has been particularly scathing around this process.

- More details are in the BOE's quarterly APF report here.

- Separately, there has been an decrease in the APF size limit agreed in a letter exchange between Governor Bailey and Chancellor Reeves. This is completely in line with usual practice and generally happens every 3-6 months after there has been a large redemption. It has no bearing on APF operations at all, unless the BOE wanted to restart QE. Even in this scenario, it usually is just a letter from the Governor to the Chancellor including the reason and creates little overall delay. The letter exchange is available here.