HUF: EURHUF Rises to New Weekly High as Cross Approaches Initial Resistance

Dec-04 10:33

- EURHUF has risen 0.45% this morning, taking the pair to a new weekly high. There is no obvious driver behind today’s move, but forint weakness comes alongside similar – albeit more moderate – weakness for the Polish zloty and Czech koruna, with the fade for EURUSD off this morning’s highs likely weighing on the euro proxies at the margins. For EURHUF, today’s move places spot just below initial resistance at 383.14, the 20-day EMA. More significant resistance is further out at 386.29, the 50-day average.

- We noted yesterday that the November NBH minutes could potentially set the stage for a language shift from the central bank in December, as officials pinned the stance for monetary policy in 2026 on its next quarterly inflation report: “The Council was in agreement that the projection in the December issue of the Inflation Report was going to be crucial from the perspective of next year’s monetary policy stance”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GERMAN AUCTION RESULTS: 2.00% Dec-27 Schatz

Nov-04 10:33

| 2.00% Dec-27 Schatz | Previous | |

| ISIN | DE000BU22114 | |

| Total sold | E5bln | E5.5bln |

| Allotted | E3.766bln | E4.25bln |

| Avg yield | 1.98% | 1.91% |

| Bid-to-offer | 1.26x | 1.07x |

| Bid-to-cover | 1.67x | 1.39x |

| Avg Price | 100.026 | 100.178 |

| Low Price | 100.020 | 100.175 |

| Pre-auction mid | 100.021 | |

| Previous date | 14-Oct-25 |

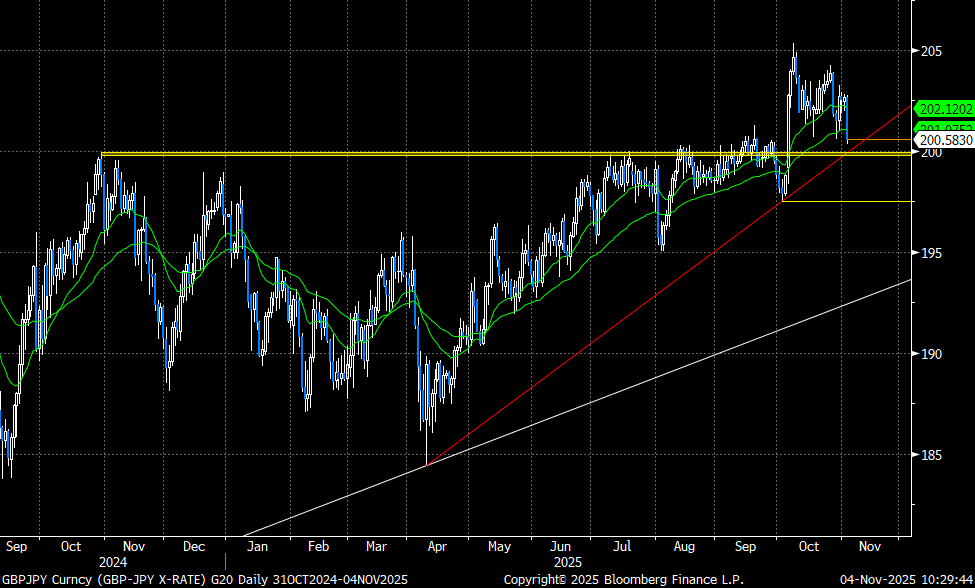

FOREX: GBP Levels Update, GBPJPY Approaching 200.00 and Trendline Support

Nov-04 10:30

- GBPUSD: As noted, pressures surrounding the fiscal trajectory for the UK are further weighing on sterling this morning, combining with the risk-off sentiment across global markets. This has prompted GBPUSD to extend pullback lows – continuing to erode the post Liberation Day rally in April. Cable trades within 30 pips of 1.3041 (Apr 14 low), of which a break would bolster bearish conditions. 1.2971 would be an interim support on the way to 1.2709, a key medium-term level.

- EURGBP: In the crosses, EURGBP has had a solid bounce from support, broadly respecting the prior breakout point at 0.8769 and initial support at 0.8751, the Sep 25 high. Topside targets for the broader rally include 0.8835 and 0.8875, the April 2023 high.

- GBPJPY: The risk off moves and fresh FX jawboning from the finance minister in Japan have contributed to the sharp 1.1% downswing for GBPJPY (shown below) today. The cross has notably breached the 50-day EMA, and is rapidly approaching the psychological 200 mark, an area that provided pivotal significance in 2024. Furthermore, a move below 200 would coincide with a break of trendline support, drawn from the April lows, which would provide additional bearish impetus for the move. 197.49 is the primary target.

- GBPCHF: Swiss franc weakness in the aftermath of soft inflation data on Monday assisted a moderate GBPCHF recovery, however, initial resistance at the 20-day EMA has been well respected, with a quick return sub-1.06 today. Moving average indicators highlight a dominant downtrend, with the focus remaining on cycle lows at 1.0501.

FOREX: GBP Soft on Clearest Signal Yet of "Unpopular" Tax Policy Ahead

Nov-04 10:28

- GBP traded softer on the back of another pre-Budget appearance from UK Chancellor Reeves. While not drawn into details on the Budget measures specifically - it was certainly her clearest signal yet that sizeable tax rises are incoming (suggested by the statement of working in the national interest, rather than political popularity), as well as indicating her intention to pave the way with fiscal policy to allow for further BoE rate cuts.

- What does this mean for GBP? GBPUSD has broken to a new pullback low - trading at comparable levels with the Liberation Day rally in April. This makes 1.3041, the Apr 14 low the area of interest ahead of 1.2971, the 1.382 proj of the Sep 17 - 25 - Oct 1 price swing.

- Outside of GBP, risk-off trade pervades after slippage in US equity futures held through overnight trade and remains the dominant theme into the crossover. Palantir is set to drop over 7% at the open as markets caution on extreme valuations and the scale of the recent rally - a move mirrored in South Korea's SK Hynix overnight - a key supplier to Nvidia.

- Resultantly, the best performing currency today is JPY, rallying against all others, will risk proxy currencies slide - namely the NZD. Initial support in USD/JPY comes in at 153.27, followed by 152.06. The technical trend structure in the pair remains bullish at this stage.

- JOLTs, trade balance and durable goods orders data were originally set for release today - but the extension of the government shutdown will keep focus on private sector data and corporate earnings as the best bellwether for the state of the economy. As such, tomorrow's ADP employment change, S&P Global final PMI and ISM services index are of utmost importance.