EUR: EURCAD hits a fresh 16yrs High

Sep-17 13:56

- Just a 19 pips swing for now in the USDCAD, initially fell but remains fairly close to where it trading at pre decision.

- The one to watch is the EURCAD that did managed a new 16yrs high, highest since July 2009.

- Immediate resistance is still right here at 1.6330, this was the June and July 2009 highs.

(Chart source: MNI/Bloomberg Finance LP).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Sep'25 5Y Ratio Put Fly

Aug-18 13:50

- 4,000 FVU5 107.75/108/108.5 2x3x1 put flys, ref 108-22.5

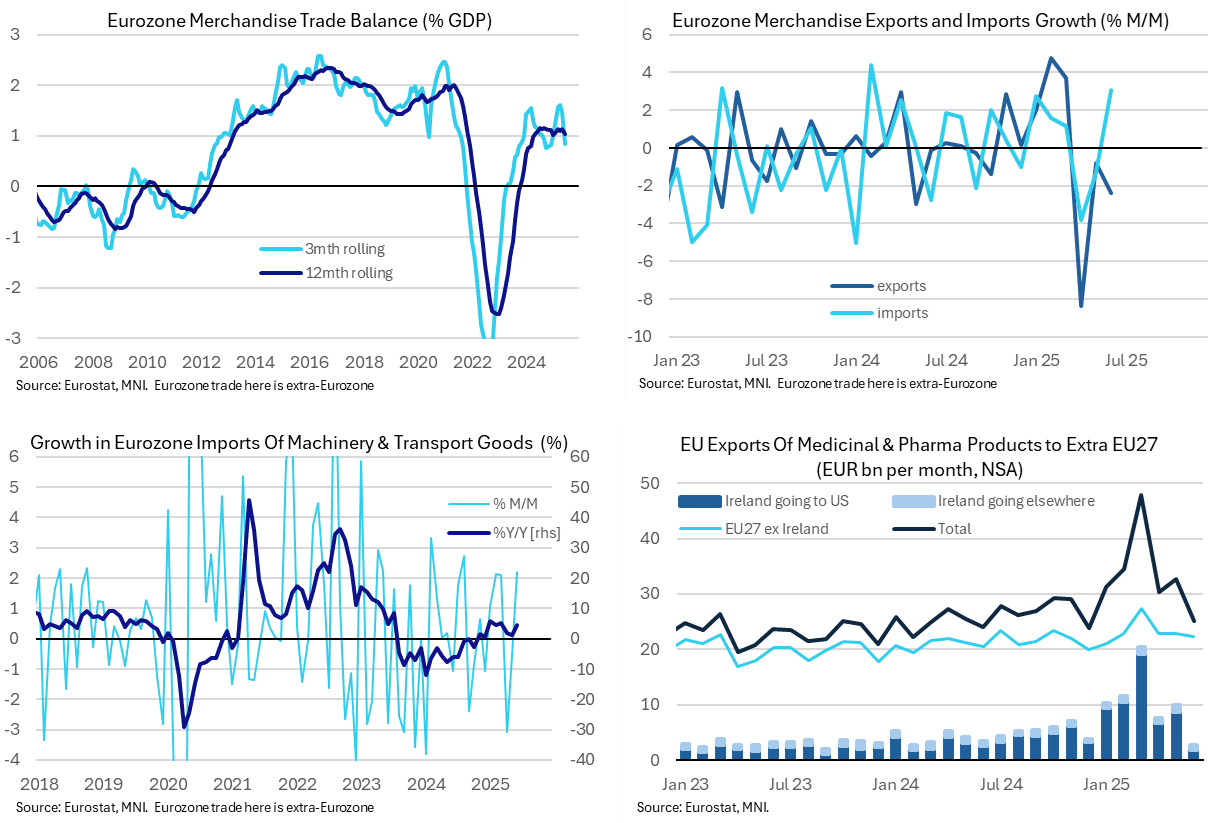

EUROZONE DATA: Trade Surplus Slips Further As Irish Pharma Surge Dries Up

Aug-18 13:45

- The Euro area goods trade surplus was smaller than expected in June at E7.0bln (cons E14.5bln).

- It saw the seasonally adjusted equivalent fall to just E2.8bln after E15.6bln in May for the lowest monthly surplus since May 2023.

- It’s an abrupt further narrowing in surpluses from the E15.0bln averaged in Apr-May and E20.5bln in Q1 (including E27.7bln in March) compared to a more typical E11.6bln in Q4.

- Alternatively, it left a goods trade surplus at ~0.8% GDP in Q2 after 1.6% GDP in Q1 and 0.8% GDP in Q4, with that 2Q25 estimate biased higher by figures earlier in the quarter.

- The narrowing came from a combination of a third consecutive monthly decline for exports (-2.4% M/M) whilst imports firmed (3.1% M/M).

- Export weakness was driven by manufactured goods shipments fell by -4.2% on a -13.2% decline in chemicals & related products likely owing to Irish pharmaceutical exports to the US.

- The more detailed NSA data show that Irish pharmaceutical exports to the US registered an unusually small E1.8bln in June (smallest since Sep 2023) after E8.7bn in May. It’s continued payback from a surge in Q1 when exports summed to E39bln vs the E44bln through 2024 as a whole. As such, it may not necessarily be surprising but it’s still notable and could see similarly small readings ahead.

- Back to the swda data, imports strength looks particularly concentrated meanwhile, with the commodities & other unclassified category surging 148% (from E2.8bln to E7.1bln) and a 7% rise in chemicals & related products (from E30.2bln to E32.3bn).

- As for somewhat more forward-looking indicators of domestic demand, imports of machinery & transport equipment increased a modest 2.2% M/M considering it followed a cumulative -3.6% decline in April and May. It left them up 4.6% Y/Y on this calendar adjusted basis for one of the faster readings in recent years but still relatively tepid for a nominal measure.

US SWAPS: J.P.Morgan Recommend 2-Year Spread Wideners

Aug-18 13:26

Late on Friday J.P.Morgan recommended 2-Year swap spread wideners.

- They reasoned that “swap spread volatility is back to year-to-date lows, making wideners attractive from a carry perspective. The 2-Year sector also offers the most favorable risk-adjusted carry relative to other sectors. Moreover, T-Bill supply in July was well digested from money funds and demand is likely to continue, which will likely keep funding conditions orderly through the remainder of the TGA rebuild phase. Lastly, front end swap spreads appear narrow to fair value”.