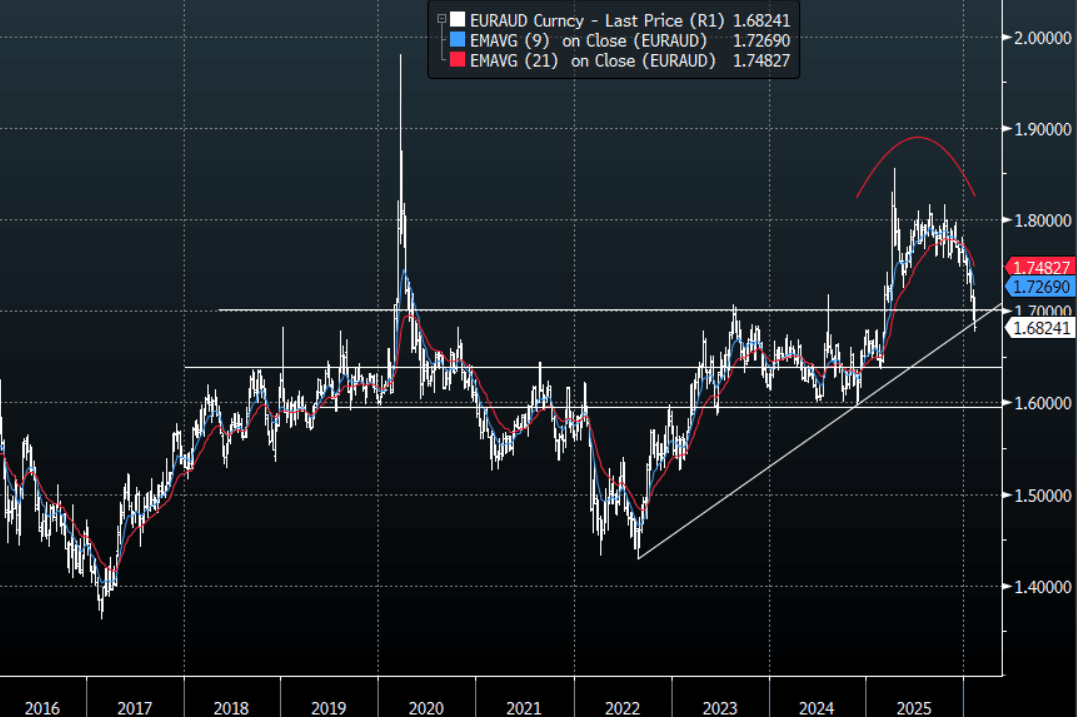

AUD: EUR/AUD - Breaks Below 1.69-1.70, Targets The 1.60-1.64 Area

The overnight range was 1.6763 - 1.6884, Asia is currently trading around 1.6830. The pair collapsed and broke powerfully back through the 1.69-1.70 support thanks to the hawkish hike from the RBA. This looks to now potentially be signaling a deeper pullback and any decent rallies should now find eager sellers. On the day, the first sell-zone is back toward the 1.6915-1.6945 area and then 1.7000-1.7050. The AUD bulls would be cheering this move and adding to AUD longs that have been outperforming across the board. This move potentially targets the 1.6000-1.6400 area.

- Bloomberg - Citigroup currency strategists are targeting an even steeper decline for EUR/AUD to 1.64 after the pair reached their previous target of 1.68. They cite interest-rate divergence between the European Central Bank and Reserve Bank of Australia

- “The RBA will probably raise its benchmark rate by 25 bps to 4.1% in May, Goldman projected, with CBA and Westpac echoing those sentiments.” - BBG

- The EUR/AUD Average True Range(ATR) for the last 10 Trading days: 141 Points

Fig 1: EUR/AUD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

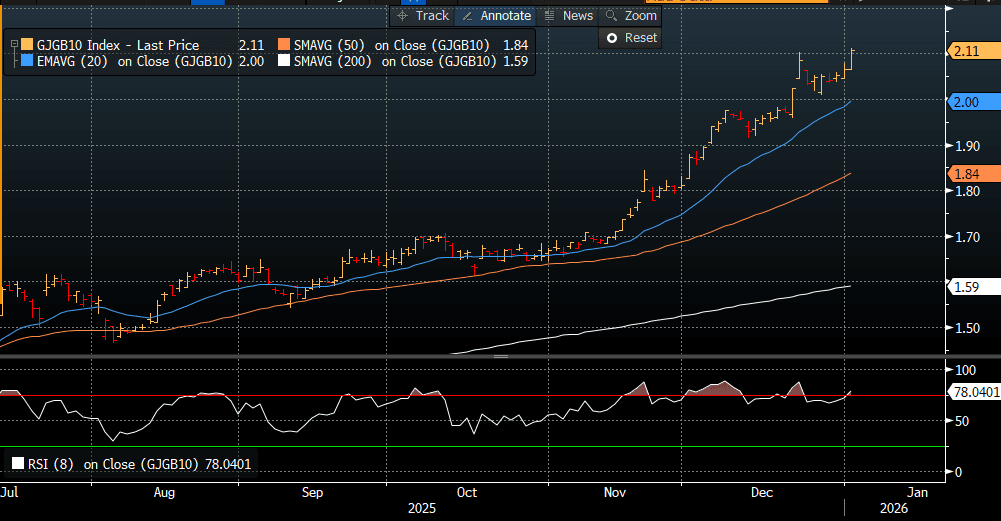

JGBS: 7Y Leads Yields Higher After Extended NY Break

In Tokyo morning trade after the extended NY break, JGB futures are weaker, -36 compared to settlement levels, and at a fresh cycle low (see chart).

- Cash US tsys are little changed in today's Asia-Pac session after Friday’s modest bear-steepener. Focus in the first two full weeks of the year will be on nonfarm payrolls (Friday) and CPI reports (Jan 13) for December, with those two key reports back on their original schedules having been prioritized by the BLS. Private sector reports meanwhile are highlighted by ISM manufacturing and services reports Jan 5 and 7. No scheduled Fed speakers today.

- Cash JGBs are flat to 5bps cheaper across benchmarks, led by the futures-linked 7-year. The benchmark 10-year yield is 4.3bps higher at 2.109%, a fresh cycle high.

- (Bloomberg) “The Japan 2-year to 10-year yield curve will flatten to 82 basis points by the end of the first quarter, from the current 89 basis points, based on Bloomberg surveys of market forecasts.”

- Swap rates are 1-4bps higher, with a steepener curve.

Source: Bloomberg Finance LP

CNH: Holding Above 6.9750, But Downtrend Still Intact, USD/CNH Oversold Per RSI

USD/CNH tracks near 6.9750 in early Monday dealings, slightly up from end Friday levels. Friday delivered fresh cycle lows of 6.9664 in the pair, with a firm downtrend still in play. Onshore markets return today after the new year break (out last Thurs/Fri). Onshore spot last closed at 6.9880, while the last USD/CNY fixing was 7.0288. A downtrend also remains in play for the fixing outcome, albeit which is still comfortably above market estimates. A positive fixing error hasn't deterred yuan bulls though.

- For USD/CNH a clean break under 6.9700 is likely to bring 6.9500 downside risks into focus. On the topside, all key EMAs are trending lower, the 20-day last near 7.0135.

- USD/CNH is oversold per RSI (14), but market focus is likely to remain on positive January seasonality for CNH and CNY. January tends to be the best month of the year for CNH, although in recent years this directional record has been more patchy. Note that the China lunar new year falls in mid Feb this year.

- On the data front today, we have the Dec RatingDog Services and composite PMI reads. The market expects a 52.0 services read against 52.1 in Nov.

- There may be some focus on the fallout from the US action in Venezuela over the weekend, but broader China macro implications are likely to be fairly limited, particularly for FX markets.

LNG: US Gas Prices Start Week Lower Following US Ousting Of Maduro

The US ousting of Venezuelan dictator Maduro over the weekend may also be important for the gas market. There is gas as a byproduct of Venezuela’s oil production and as a result it has the third largest gas supply in Latin America. However, given the country’s oil sector has been neglected and significant investment will needed to increase its output substantially, the shift from gas importer to exporter could also take some time.

- US Henry Hub has started Monday’s trading sharply lower at $3.46 after falling 1.2% on Friday to $3.641 to be down 6.1% on the week as the weather outlook into mid-January shifted warmer. Bloomberg notes that it is approaching oversold territory on the 9-day RSI.

- Atmospheric G2 is forecasting well above average temperatures for the eastern two-thirds of the US over the second week of January. The shift to a milder winter is reflected in demand rising only 0.7% y/y last Friday. Production rose 4.6% y/y.

- European gas rose 2.25% to EUR 28.795 on Friday just off the intraday high at EUR 29.075. After a mild start to winter, the weather has shifted significantly colder driving a 3.1% increase in prices last week as heating demand rose. European storage has started January at around 60.5% down from 75% at the start of December and well below the seasonal average but consistent import and pipeline flows are helping.