FOREX: EUR Stages Late Rally on French Political Progress

Oct-14 16:54

- The EUR staged a late rally, putting EURUSD through to a new intraday high at the London close as French politics progressed quickly: some opposition parties appear to have conceded that they will not proceed with a no confidence vote - providing interim stability for parliament - while gaining further pledges from cabinet on pensions reform. While the rally looks firm, initial firm resistance at 1.1779, the Oct 1 high, is still some way away, leaving the medium-term bear trend intact for now.

- The USD traded mixed despite a strong start Tuesday. The USD Index faded quickly off any test of multi-month highs, as USTR's Greer confirmed that staff-level communications between US and Chinese representatives was underway. This left markets to factor out the frostier conditions between Beijing and Washington. Resultantly, risk proxies recovered, putting AUD clear of new lows, although well short of resistance.

- Meanwhile, equities traded mixed, with no visible support from the beginning of equity earnings season. Financials make up the bulk of reports this week, building up to 50% of the S&P 500 by market cap having reported by the end of the month.

- Australia's Westpac Leading Index, Chinese inflation for September and French final CPI are the data highlights Wednesday. Instead, the central bank speaker slate is likely of more interest to markets, and Wednesday is busy: Fed's Miran, Waller & Schmid, ECB's de Guindos, Rehn & Villeroy, BoE's Ramsden & Breeden and RBA's Hunter are all set to speak.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (U5) Bounces Further Off Support

Sep-12 21:45

- RES 3: 97.190 - High May 5 2023

- RES 2: 96.932 - 76.4% of Mar-Nov ‘23 bear leg

- RES 1: 96.860 - High Apr 07

- PRICE: 96.550 @ 15:36 BST Sep 12

- SUP 1: 96.430/95.900 - Low Sep 3 / Low Jan 14

- SUP 2: 95.760 - Low 14 Nov ‘24

- SUP 3: 95.480 - Low Jan 11 2023 and a major support

Aussie 3-yr futures are trading off recent lows. A resumption of gains from here would further narrow the gap with resistance at 96.730, the Sep 17 ‘24 high, leaving 96.860 as the next key level. Any continuation lower would instead strengthen a bearish threat. This would refocus attention on 95.760, the 14 Nov ‘24 low. Conversely, a reversal higher would open 96.860, the Apr 7 high.

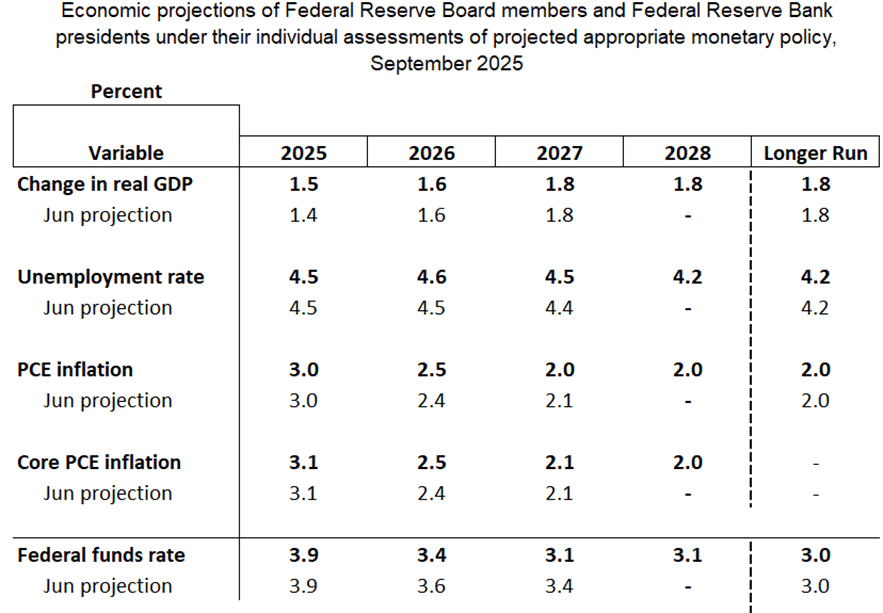

FED: MNI Fed Preview-September 2025: A Reluctant Return To Easing

Sep-12 21:16

We've published our preview of the upcoming FOMC meeting - Download Full Report Here

- The Federal Reserve is set to resume its easing cycle at the September 16-17 meeting with a 25bp cut to the funds rate range to 4.00-4.25%.

- The decision to cut after a 5-meeting pause was well-telegraphed by Chair Powell, whose Jackson Hole speech described a “shifting balance of risks” toward a weaker labor market that “may warrant adjusting our policy stance”.

- The updated quarterly projections aren’t likely to bring many changes to the macroeconomic variables, but as usual the signal sent from the Fed rate “Dot Plot” will garner attention. A Committee split between expecting one or two further cuts this year is likely, keeping each of the remaining meetings of 2025 “live”.

- The Statement will downgrade the description of the labor market to reflect a rise in the unemployment rate and poor payrolls growth, and is likely to include at least one dissent to the rate decision.

- But with a Committee that is fairly divided on the way forward, Powell will be noncommittal on future action, reiterating that policy is not on a preset course, and upcoming decisions will be data-dependent.

- A key undercurrent is an increasingly activist approach to Fed personnel management from the White House, which leaves the composition of the FOMC uncertain not just over the medium-term but also at this meeting.

MNI’s separate preview of sell-side analyst summaries to follow on Monday Sep 15

RATINGS: Fitch: France Cut To A+ From AA, Portugal Up To A From A-

Sep-12 21:07

Fitch has downgraded France's sovereign rating to A+ (with stable outlook) from AA-. Release here.

- Among other factors in the decision, Fitch cites "High and Rising Debt Ratio", "Political Fragmentation Hinders Consolidation", "Weak Fiscal Record", "High 2025 Deficit", "Uncertain Fiscal Consolidation Path", and "Fiscal Rigidities".

- In "Factors that Could, Individually or Collectively, Lead to Negative Rating Action/Downgrade", Fitch cites "Public Finances: A sustained increase in government debt/GDP over the medium term, due to failure to implement fiscal consolidation measures and/or a persistent increase in financing costs" and "Macro: Materially lower economic growth prospects and weakened competitiveness." Conversely, potentially leading to positive ratings action would be "Public Finances: Confidence that government debt/GDP will be put on a downward trajectory over the medium term, for example, due to fiscal consolidation and/or stronger economic growth".

- Fitch also raised Portugal to A (stable outlook) from A-, while elsewhere, S&P raised Spain to A+ (stable outlook) from A.

- As MNI wrote earlier, we expected France to be downgraded to A+ and Portugal to be upgraded to A.