CREDIT PRE-MARKET: EUR Market Wrap

- 2y/10y bunds closed -4bp/+1bp – yields were little changed in the afternoon with our DM flagging very light spillover from dovish-leaning BoC decision into ECB cutting expectations. Given the expected “bumpiness” in core inflation through the remainder of this year, the scope for material further dovish repricing should be limited, absent a notable deterioration in growth prospects.

- Main/XO ended +1bp/+5bp at 54.4bp/298bp while €IG/€HY was flat/+3bp with short-dated spreads underperforming by under 1bp and Energy, Fins and Utils marginally in he red. €IG remains closed though £IG was open with Severn Trent’s (SVTLN Baa2/BBB/BBB) GBP 350mn 14yr tightening just 15-20bp to price with a NIC of ~19bp after sector peer Severn Trent was downgraded while books were open.

- SXXP ended -0.6% with Tech and Consumer P&S over 2% lower while SPX was -2.3%. Notable €IG movers included SGS SA +11%, Nidec +6%, AT&T +5%, Deutsche Bank -9%, Fortive -8%, Dell -8%, Otis Worldwide -7&, Eaton Corp -7%, Stora Enso -7%

- SX5E futures are -0.6% while SPX futures are +0.2%. UST futures have edged slightly higher throughout the night with the front-end out-performing again which has been helped by multiple block steepener trades going through. Safe haven gains again dominate the G10 FX space.

- Later US Q2 GDP, jobless claims, June durable orders and German July Ifo survey print. Also ECB President Lagarde speaks.

| Date | GMT/Local | Impact | Country | Event |

| 25/07/2024 | 0600/0800 | ** | SE | PPI |

| 25/07/2024 | 0645/0845 | ** | FR | Manufacturing Sentiment |

| 25/07/2024 | 0800/1000 | ** | EU | M3 |

| 25/07/2024 | 0800/1000 | *** | DE | IFO Business Climate Index |

| 25/07/2024 | 1000/1100 | ** | UK | CBI Industrial Trends |

| 25/07/2024 | - | EU | ECB's Cipollone at Rio de Janeiro G20 Fin min/central bank meeting | |

| 25/07/2024 | 1230/0830 | *** | US | Jobless Claims |

| 25/07/2024 | 1230/0830 | ** | US | WASDE Weekly Import/Export |

| 25/07/2024 | 1230/0830 | *** | US | GDP |

| 25/07/2024 | 1230/0830 | * | CA | Payroll employment |

| 25/07/2024 | 1230/0830 | ** | US | Durable Goods New Orders |

| 25/07/2024 | 1230/0830 | ** | US | Advance Trade, Advance Business Inventories |

| 25/07/2024 | 1300/1500 | ** | BE | BNB Business Sentiment |

| 25/07/2024 | 1430/1030 | ** | US | Natural Gas Stocks |

| 25/07/2024 | 1500/1100 | ** | US | Kansas City Fed Manufacturing Index |

| 25/07/2024 | 1500/1700 | EU | ECB's Lagarde attends Paris Summit | |

| 25/07/2024 | 1530/1130 | * | US | US Bill 08 Week Treasury Auction Result |

| 25/07/2024 | 1530/1130 | ** | US | US Bill 04 Week Treasury Auction Result |

| 25/07/2024 | 1700/1300 | ** | US | US Treasury Auction Result for 7 Year Note |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Approaching The Bull trigger

- RES 4: 173.01 2.0% 10-dma envelope

- RES 3: 172.77 Round number resistance

- RES 2: 171.56 High Apr 29 and the bull trigger

- RES 1: 171.45 High Jun 24

- PRICE: 171.22 @ 06:50 BST Jun 25

- SUP 1: 169.60 20-day EMA

- SUP 2: 168.68/167.53 Trendline from the Dec 7 ‘23 low / Low Jun 14

- SUP 3: 167.33 Low May 16

- SUP 4: 165.64 Low May 7

The EURJPY trend structure remains bullish and the cross traded higher Monday. The key trendline support - currently at 168.68 - remains intact. The line is drawn from the Dec 7 ‘23 low. A clear breach of it is required to threaten a bullish theme and highlight a potential reversal. 170.89 resistance, the Jun 3 high, has been breached. Sights are on the bull trigger at 171.56, Apr 29 high.

BTP TECHS: (U4) Trading Below Resistance

- RES 4: 119.00 Round number resistance

- RES 3: 118.58 High May 16 and a key resistance

- RES 2: 117.62 High Jun 5 and key resistance

- RES 1: 117.09 High Jun 21

- PRICE: 116.53 @ Close Jun 25

- SUP 1: 115.28/114.35 Low Jun 12 / 11

- SUP 2: 114.02 1.236 proj of the May 16 - 29 - Jun 5 price swing

- SUP 3: 113.60 1.382 proj of the May 16 - 29 - Jun 5 price swing

- SUP 4: 112.77 61.8% of the Oct 19 - Dec 27 2023 rally (cont)

BTP futures have traded in a volatile manner recently. The latest bear reversal from the Jun 5 high, confirmed the end of the corrective phase between May 29 - Jun 5. This resulted in a break of key support at 115.54, Apr 25 low, highlighting a resumption of the downtrend. However, price has rebounded from the Jun 11 low of 114.35. Initial key resistance is 117.62, Jun 5 high. A break would be bullish. First resistance is 117.09, last Friday’s high.

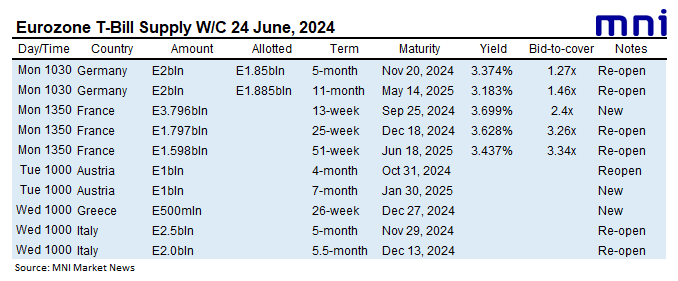

EUROZONE T-BILL ISSUANCE: W/C June 24, 2024

Austria, Greece and Italy are all due to sell bills this week, whilst Germany and France have already issued. We expect issuance to be E18.2bln, down from E18.5bln last week.

- Today, Austria will issue E1bln of the 4-month Oct 31, 2024 ATB and E1bln of the new 7-month Jan 30, 2025 ATB.

- Tomorrow, Greece will issue E500mln of the new 26-week Dec 27, 2024 GTB.

- Also tomorrow, Italy will look to sell E2.5bln of the 5-month Nov 29, 2024 BOT and E2.0bln of the 5.5-month Dec 13, 2024 BOT.

For more on future auctions see the full MNI Eurozone/UK T-bill auction calendar here.