EMISSIONS: EUA DEC25 Implied Volatility Hits All-Time Low

Dec-05 10:50

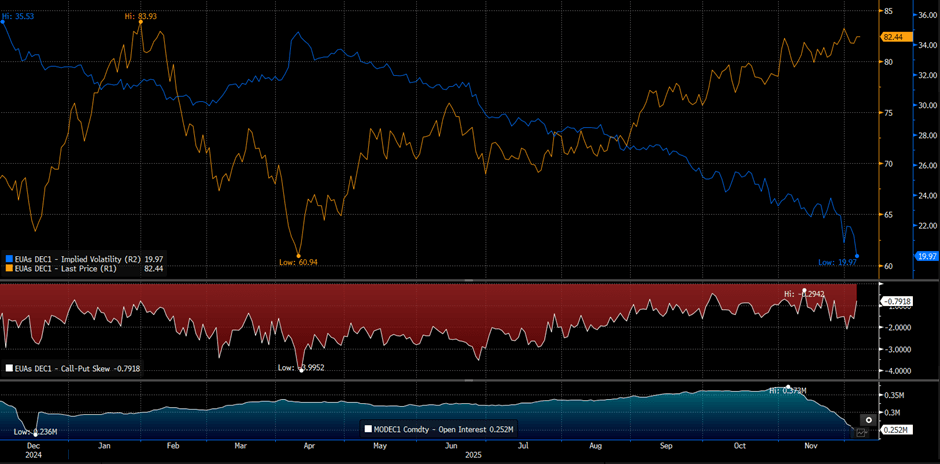

EUA Dec25 options implied volatility fell to an all-time low on 4 Dec, with put open interest rising and calls declining, signalling stable expectations for price swings and caution over downside risks.

- EUAs Dec25 options are set to expire on 10 December.

- Implied volatility dropped to 19.97% on 4 Dec from 22.73% on 26 Nov.

- The 25-delta call-put volatility skew narrowed to -0.79% on 4 Dec from -1.6% on 26 Nov.

- The put/call open interest ratio rose to 0.99 on 4 Dec from 0.96 on 26 Nov .

- Put open interest climbed 2% to 188k contracts from 185k on 26 Nov, while call open interest fell 1% to 190k contracts from 192k on 26 Nov.

- The largest open interest as of 26 Nov remains at the €70/t put strike with 24k contracts, and the €100/t call strike with 26k contracts, unchanged for calls and slightly lower for puts, respectively.

- EUA Dec25 open interest dropped to 252k on 3 Dec, reaching the lowest level since mid-December 2024.

- EUA DEC 25 up 0.05% at 82.47 EUR/t CO2e

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA OPTIONS: Midcurve Call Spread vs Put Spread

Nov-05 10:49

0NU6 96.80/97.10cs vs 0NU6 96.30/96.00ps, bought the cs for -0.25 and flat in 7.5k.

US TSY FUTURES: TY Blocked

Nov-05 10:42

Latest block trade lodged at 10:24:46 London/05:24:46 NY:

- TYZ5 7,460 lots blocked at 112-26, looks like a seller.

- DV01 ~$500K.

EGBS: Bund Futures Continue To Consolidate Above Key Support Zone

Nov-05 10:39

- The early risk-off inspired bid in Bund futures has faded, but RXZ5 remains above the 129.13 support area (aligning with the 50-day EMA and October 13 low). Futures are currently -2 ticks at 129.27, with solid results at today's 15-year Bund auction helping the contract away from session lows of 129.22.

- German yields are up to 1bp lower across the curve.

- Alongside the German supply, Italy held a E5bln buyback transaction.

- 10-year EGB spreads to Bunds are up to 1bp wider on the session, with global equity sentiment still relatively weak.

- Following upward revisions in France and Germany, and stronger-than-expected readings in Italy and Spain, the Eurozone services PMI was revised up to 53.0 (vs 52.6 flash, 51.3 prior). With the manufacturing PMI confirming flash estimates at 50.0 on Monday, this left the composite reading at a 29-month high of 52.5.

- There were marginal upward revisions to the ECB's latest forward-looking wage tracker relative to the September iteration, but the general conclusion that compensation pressures are expected to ease in the coming year remains intact.

- ECB’s Kocher is scheduled to speak on “Negative Rates and the Effective Lower Bound” later today.