EMISSIONS: EU ETS Raises Cost for Intra-EU Shipping Voyages by 45% in 2026

{EEU ETS costs for intra-EU voyages will increase to about $315-$324/t in 2026 from $217–$224/t in 2025, using an assumed EUAs price of €85/tO2e, according to PortNews.

- From 1 January 2026, shipowners must cover 100% of EU ETS costs for covered voyages, up from 70% in 2025 and 40% in 2024.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: EUREX ROLL (Updated)

- Buxl: 54%.

- Bund: 57%.

- Bobl: 77%.

- Schatz: 65%.

- BTP: 63%.

- BTS: 80%.

- OAT: 68%.

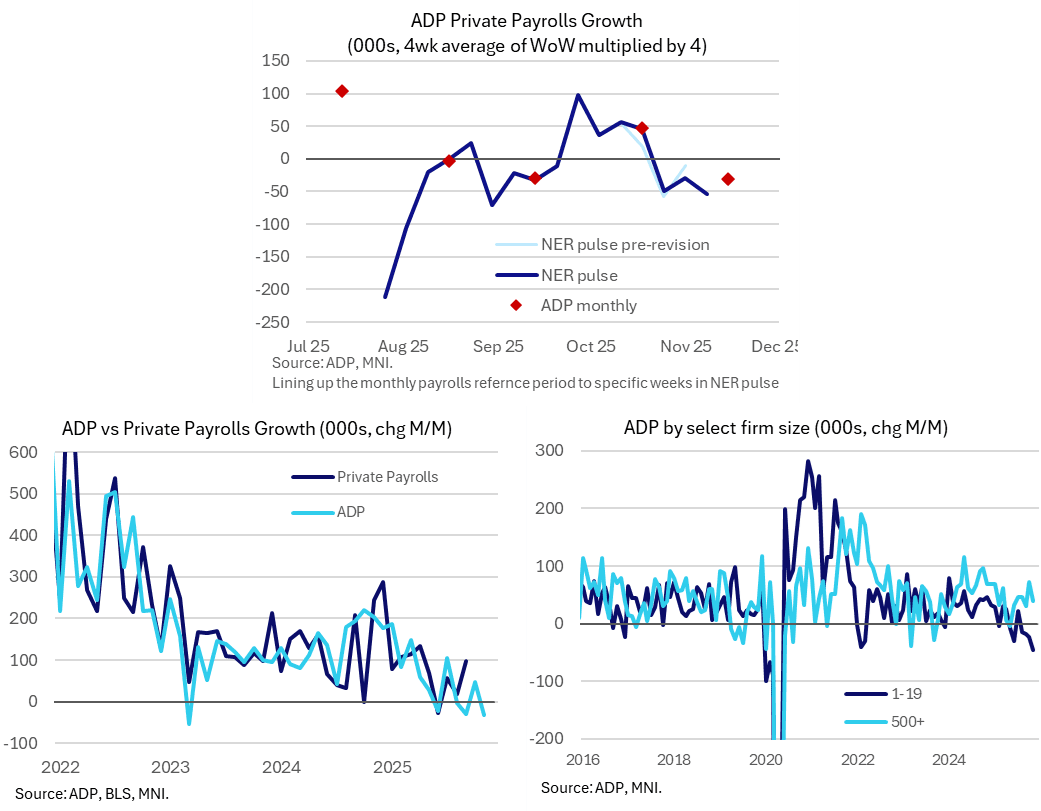

US DATA: No Real Surprises For ADP As Confirms Return Of Declining Employment

The monthly ADP report in November turned out closer to the weakness implied by its own weekly tracker than Bloomberg consensus which had surprisingly eyed a small increase on the month. It confirms a return to a monthly decline in private employment, with a third decline in the past four months.

- ADP employment growth “surprised” lower at -32k (Bloomberg cons 10k) in November whilst the October increase was revised up from 42k to 47k.

- However, as noted in our preview this morning, this had looked an odd consensus figure considering last week’s ADP NER Pulse update saw an average weekly change of -13.5k in the four weeks up to Nov 8, i.e. closer to a -55k decline on a rolling monthly basis.

- In theory, this monthly report should have offered limited new information from that in the weekly series as, broadly mimicking the BLS payrolls report, its reference period is the week including the 12th of the month.

- As we wrote: “The weekly series is prone to revisions although we’d be surprised if they were strong enough to materially alter a weak trend that has seen three weeks averaging -11k (on the same four-week rolling basis, i.e. closer to -45k in monthly terms). “

- Further, the previous current vintage for the weekly tracker had pointed to a ~46k increase back in October so today’s modest upward revision also chimes there.

- Back to today’s monthly report, smaller firms clearly felt pressure in November, with -46k for those with 1-19 employees and -74k for those with 20-49. The offsetting 90k increase elsewhere was led by a 39k increase for those with 500+ employees after a strong 73k increase for the latter in October.

- From today's press release (link): "Job creation has been flat during the second half of 2025 and pay growth has been on a downward trend. November hiring was particularly weak in manufacturing, professional and business services, information, and construction.

- * Hiring has been choppy of late as employers weather cautious consumers and an uncertain macroeconomic environment. And while November's slowdown was broad-based, it was led by a pullback among small businesses."

- The broader momentum in the series should be viewed as an important indicator for jobs growth, with the three-month average slowing through the year to date (200k in Dec 2024, 139k in Mar, 22k in Jun, 24k in Sep and -4k most recently in Oct).

STIR: No Real Movement In Fed Pricing Following ADP, Terminal Hovers Around 3%

Modest dovish adjustment in the U.S. short end in the wake of the softer-than-expected ADP employment reading and slight softening in the wage growth metrics that come within the data (some counter from a marginal upside revision to the prior reading).

- Fed Funds showing 23.5bp of easing for this month, 32bp through January, 39.5bp through March, 47.5bp through April and 62.5bp through June, little changed vs. pre-data levels.

- SOFR futures now 0.25-4.0bp higher on the day vs. 0.25-3.5bp firmer into the release. Implied terminal rate pricing briefly moved to 3.005% vs. 3.025% ahead of the release, operating around the middle of the approximate 2.80-3.20% multi-month range.